Fiduciaries Managing Costs

|

|

|

- Helena McCarthy

- 8 years ago

- Views:

Transcription

1 AFP National Conference San Antonio, Texas DC Plan Fee Transparency: Fiduciaries Managing Costs November 9, 2010 Presented by: Linda Ruiz-Zaiko ik Randy Murphy Financial, Inc. Manager, Global Equity Plans salesforce.com, inc.

2 DC Plan Fee Transparency: Fiduciaries Managing Costs November 9, 2010 Presented by: Randy Murphy Manager, Global Equity Plans Salesforce.com

3 Salesforce.com CRM (NYSE) Worldwide leader in on-demand d customer relationship management (CRM) services and enterprise cloud computing Founded in 1999 by former Oracle executive, Marc Benioff 82,400+ Customers, 800+ Applications, 15 Languages Revenues: US$ 1.5 Billion (FYE 4/30/2010)

4 Salesforce.com s Mission: Cloud Computing Driver, Catalyst & Evangelist Mainframe Client/Server Cloud Computing 1960 s Platforms 1980 s Platforms Today

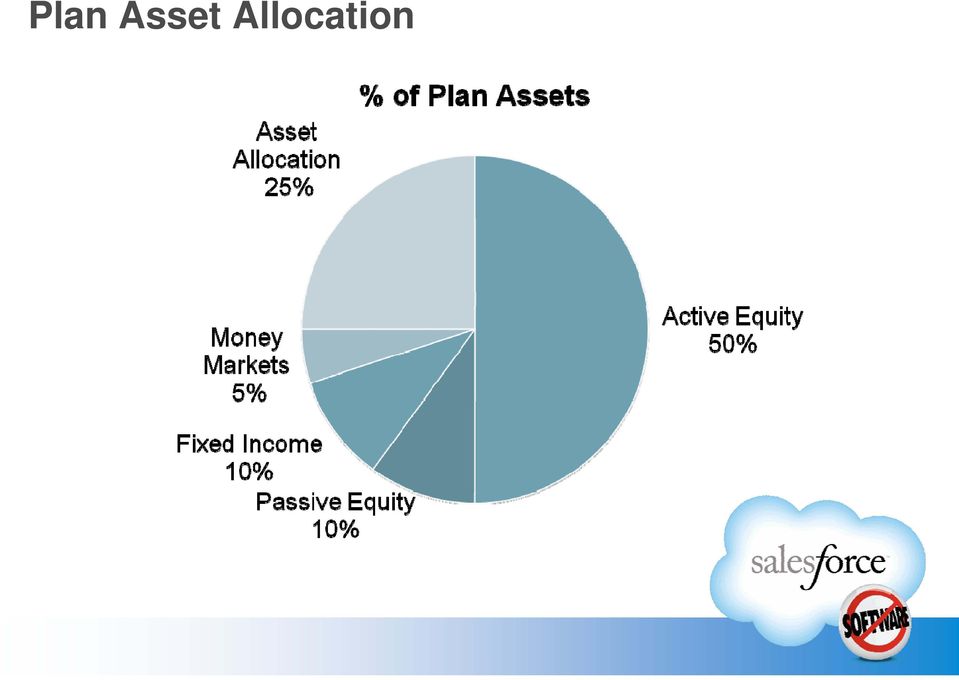

5 The Salesforce.com 401(k) Savings Plan Over 3,000 participants Bundled Provider for Recordkeeping, Funds, Education is Independent Investment Consultant Fiduciary 404 (c) compliant QDIA Target-Date Funds Auto-enrollment t (with opt-out) t) 14 Core Fund Options - Active and Index Funds Multiple Fund Families, highly rated funds Roth 401(k) using same core funds Regular participant education program

t) 14 Core Fund Options - Active and Index Funds Multiple Fund")

6 Plan Asset Allocation

7 Plan, Fund and Fee Monitoring Quarterly review with 401(k) Committee, minutes Investment Policy Statement, due diligence, watchlist Use third party investment consultant, fiduciary to plan Because Provider s investment consultant is not fiduciary Benchmark expenses quarterly Per Fund - total t fees, % and $ Revenue Share by Fund, % and $ Per-Participant P i t $ Cost Measure as % of Total Assets and Absolute Dollars Renegotiated t fees multiple l times as balances grew Reduced per-participant cost Changed to lower-cost share classes

8 DC Plan Fee Transparency Why Do We Care? DC plan sponsors have a fiduciary duty under ERISA To ensure that Plan fees are reasonable Neglecting fees may be deemed a fiduciary breach Explosion in class action lawsuits against plan sponsors Allege that plans sponsor breached their fiduciary duties under ERISA Used plan assets via revenue-share or indirect compensation to pay excessive fees Used retail funds when lower fee (institutional) funds were available New IRS 5500 Schedule C requires providers fee breakdown for 2009 Congress has competing Fee Disclosure Acts for participant disclosures DOL regulations under ERISA Section 408(b)(2) effective July, 2011 All providers must disclose direct and indirect compensation Recent fee survey shows expense ratios rose in 2009

funds were available New IRS 5500 Schedule C requires providers fee breakdown for 2009 Congress has competing Fee Disclosure Acts for participant disclosures DOL regulations")

9 ERISA - Fee Transparency Why do we Care? 3 sets of regulation concerning reasonable fees: Establishment of Trust rules under ERISA Section 403 Prudent Man standard of care under ERISA Section 404 Prohibited Transaction exemption under ERISA Section 408(b)(2) Severe penalties under ERISA if plan sponsor breaches its fiduciary duties ERISA Section 409 Fiduciary is personally liable for plan losses from a breach or use of plan assets to pay unreasonable fees ERISA Section 502(1) 20% civil penalty on amounts recovered from a DOL settlement IRS Code 4975 Excise tax against provider receiving unreasonable compensation (prohibited transactions) ERISA Section 502(a) Empowers participants to sue for fiduciary breach

20% civil penalty on amounts recovered from a DOL settlement IRS Code 4975 Excise tax")

10 DOL Disclosure Regulations under ERISA Section 408(b)(2 ) Effective July 16, 2011 disclosure rules target revenue sharing All service providers, affiliates and sub-contractors (>$1,000) Must provide written description of services and compensation Revenue share is permissible if the compensation for relevant services rendered is reasonable Plan sponsor must assess appropriateness and reasonableness of fees Plan sponsor could be in fiduciary breach if total fees are unreasonable Providers are not required to identify a specific conflicts of interest including referral relationships Referral relationships that do not entail $ compensation Are not required to be disclosed Plan sponsors must figure it out

11 Best Practices Plan sponsors should have detailed written service agreements Create a Fee Policy Statement (supplements the IPS) Documents a due diligence process to monitor provider costs Provider qualifications, service standards, reasonableness Conduct a plan Fee Analysis periodically Use Benchmarking Studies to determine reasonableness Renegotiate fees or more services using reliable competitive information Establish an ERISA budget account to recapture fees Conduct a provider RFP if services are inadequate

12 Plan Service Providers Key Players in Bundled and Unbundled Plans Recordkeeping Third party administration Investment management Trustee services Education and communication Legal counsel Auditor Investment consultant Financial i advisor or broker Managed accounts Self-directed brokerage On-line advice Participant transactions

13 Types of Fees Direct fees Billed expenses paid by plan sponsor or plan assets Invoiced, visible and known Indirect (hidden) fees Embedded fees difficult to track Revenue sharing arrangements among service providers Often asset-based As assets grow fees can become excessive Deducted from participant accounts or plan assets Netted against investment returns

14 Revenue Sharing Revenue share is derived from: 12(b)-1 fees Investment management fees Administrative services charges Different share classes Proprietary funds Sub-transfer agent fees Wrap fees Finder s fees Overrides, volume, asset incentives Asset charges or wrap fees Group annuity contract charges Sales charges Redemption fees Surrender charges

15 Typical Revenue Sharing Direct Expenses Plan Sponsor pays expenses Indirect Expenses Recordkeeper/ Administrator i t Investment fund revenue share pays expenses* Participants pay investment expenses, net returns Participants pay expenses *When revenue share exceeds plan recordkeeping/administrative fees, excess revenue share can be applied to plan expenses or rebated to participants.

16 Fees to Be Deducted from 401(k) Accounts Plan expenses are paid by the plan sponsor and/or from plan assets Costs can be divided into three categories: One-time or initial plan fees Recurring or ongoing fees Termination fees Recurring or ongoing fees are calculated: Participant-based Transaction-based Asset-based as assets grow, fees can become excessive

17 DC Plan Cost Disclosure Worksheet Source: Profit Sharing/ 401(k) Council of America (PSCA)

")

18 DC Plan Cost Disclosure Worksheet Source: Profit Sharing/ 401(k) Council of America (PSCA)

")

19 DC Plan Cost Disclosure Worksheet Source: Profit Sharing/ 401(k) Council of America (PSCA)

")

20 Reasonableness of Fees Reasonable investment fees Retail, institutional, and share class are critical Collective trust index funds tend to have higher fees Annual fund operating expense vs. peer group Fund asset manager quality Net performance vs. benchmark and peers Comparative peer pricing from fund databases Fiduciary best practice Maintain a written record to document a prudent review of funds and fees

21 Tibbe v. Edison International Share Class is Critical Class Action Suit - Edison International (SCE) Plan assets were $3.1 billion in 2005 July 14, 2010 Court decides against Southern California Edison Court declares using retail vs. institutional share class funds is a fiduciary i breach Plan sponsor took advice of its plan investment consultant Selected 3 retail fund shares instead of their less-costly institutional share classes Investment in retail share classes cost participants p excessive fees Plan sponsor should have asked fund managers for institutional class and to waive minimums which the managers age had done for other plans The consultant did not ask yet the plan sponsor is at fault

22 Benchmarking Study Identify the total costs of the current plan services Benchmarking study compares the plan s fees with comparable plans Easiest and lowest cost way to document reasonableness Provides comprehensive relevant comparisons Plan s fees, design, support and services to a benchmark group of similar plans Provides basis to renegotiate services and fees if appropriate Benchmarking Study provides documentation of a thorough and objective fiduciary process. RFP to new providers Can be appropriate to obtain new bids and services if plan has not been upgraded in several years Typically RFP is more expensive than benchmarking Should result in substantial additional savings, upgraded services, better fund platform

23 Administration Recordkeeping Fees Current Plan Plan Sponsor Eligible Employees 11,001 Plan Participants 9,903 Provider Administration/Recordkeeping Fees Description Current Provider Industry Average Provider A Provider B Provider C Annual Base Fee Billed Expenses Indirect Fees Per Eligible Fee Per Participant Fee

24 Average Plan Expense Ratios Average Expense Ratios Description Current Provider Average Provider A Provider B Provider C Average Equity Expense Ratio Average Bond Expense Ratio Average Money Market / Stable Value EpenseRatio Expense Average Additional Asset Management Rate

25 Compensation for Service Provider Compensation for Service Provider - Revenue Share Description Current Provider Industry Standard Provider A Provider B Provider C Amount % Amount % Amount % Amount % Amount % Investment Manager Trustee/Custodian Advisor Recordkeeper Adminis trator Legal - Plan Amendments Accounting Participant Communications Total Annual Compensation

26 Benchmarking Summary Retain independent, third party to benchmark costs Verify Fees, expenses, revenue sharing, amounts, parties involved Use institutional share class rather than retail funds Use expense reimbursement accounts to recapture excess fees Renegotiate asset-based fees as plan grows Renegotiate fund share class Benchmark services and fees Develop a benchmarking peer group Renegotiate for additional services Use industry surveys to benchmark costs

27 Plan Benchmarking Recordkeeper Fees Plan Fees in Dollars Advisor Fees Plan Fees in Dollars Fund Management Fees Plan Fees in Dollars Investment fees $ 157,664 Managed Account Fees $ 124,687 Other Fees $ 137,650 ERISA Spending Account Credit $ (75,000) Total Fees $ 207,351 Investment fees $ 75,945 Commissions $ - Finder s Fees $ 795 Other Fees $ 2,500 Total Fees $ 79,240 Investment fees $ 175,945

28 Plan Benchmarking Breakdown Fee Type $ Plan Fees % Plan Fees Investment Fees $ 268,493 27% Commissions - 0% Finder s Fees $ 795 0% Managed Account Fees $ 49,374 13% Other Fees $ 58,150 15% ERISA Spending Account Credit $ (25,000) - Grand Total $ 351, % Breakdown By Service Provider Plan Fee in Dollars Plan Fee in Percent Recordkeeper $ 95,001 27% Advisor/Consultant $ 79,240 23% Investment Managers $ 130,564 37% Managed Accounts Provider $ 24,687 7% Other Service Providers $ 22,320 6% Grand Total $ 351, % 28

29 Plan Benchmarking Expense Ratios for the Funds vs. Benchmark Universe 8 funds are Lowest Expense 4 funds are Below Median 3 funds are Above Median 5 funds are Highest Expense Total Fund Expense vs. Benchmark Universe

30 Document Fee Conclusions Document the reasons that plan fees are reasonable for the services rendered Complexity of plan design Accuracy of processing Customized services Responsiveness to inquiries Prompt problem resolution High number of transactions Documentation shows that plan sponsor considered plan fees and quality of services Establish an ERISA fee recapture account if fees are high Excess revenue sharing received by the provider is deposited into an account Fees used under the plan sponsor s instructions to pay ERISA eligible plan expenses or return to participants

31 Best Practices Create a Fee Policy Statement (supplements the IPS) Documents a due diligence process to monitor provider costs Provider qualifications, service standards, reasonableness Conduct a plan Fee Analysis periodically and document results Use Benchmarking Studies to determine reasonableness Renegotiate fees or more services using reliable competitive information Establish an ERISA budget account to recapture fees Document the benchmarking results Conduct a provider RFP if plan has outgrown provider s services

32 Financial, Inc. Retirement Plan Services Bid Financial, i Inc. is a fee-based, independent d investment t consulting firm launched in It is a registered investment advisor under the Investment Advisor Act of 1940 and advises defined contribution plans (401(k), 401(a), 403(b) and 457 plans). As a co-fiduciary to defined contribution plans, provides a full range of services including investment policy statements, ongoing plan and investment monitoring, 401(k) provider search/evaluation, fee negotiations, implementation, plan benchmarking, performance monitoring and fiduciary reviews. consultants help employers enhance retirement plan features while reducing plan costs, improving investment options, and reducing fiduciary liability. Each consultant has over 25 years of financial experience advising institutional investors, corporations, foundations and endowments. The dedicated team of professionals has practical experience at major global institutions in addition to holding MBAs and the Chartered Financial Analyst (CFA) designation. These credentials and practitioner experience empower them to create pragmatic solutions to a diverse range of consulting engagements

Using ERISA Accounts to Help Manage Fee-Related Fiduciary Responsibilities

Defined Contribution Plans Fiduciary Focus Series Using ERISA Accounts to Help Manage Fee-Related Fiduciary Responsibilities Contents 1 Employer Fee Responsibilities 2 Revenue Sharing 3 DOL s View of ERISA

Defined Contribution Plans Fiduciary Focus Series Using ERISA Accounts to Help Manage Fee-Related Fiduciary Responsibilities Contents 1 Employer Fee Responsibilities 2 Revenue Sharing 3 DOL s View of ERISA

401k Regulation and the New Fiduciary Responsibility of Sponsors

T. Rowe Price 401(k) Fees and Fiduciary Responsibility What Plan Sponsors Need to Know Retirement Insights Executive Summary In recent years, market events have made many 401(k) participants more sensitive

T. Rowe Price 401(k) Fees and Fiduciary Responsibility What Plan Sponsors Need to Know Retirement Insights Executive Summary In recent years, market events have made many 401(k) participants more sensitive

Not FDIC Insured May Lose Value Not Bank Guaranteed RETIREMENT FIDUCIARY FOCUS

USING ERISA ACCOUNTS TO HELP MANAGE FEE- RELATED FIDUCIARY RESPONSIBILITIES Not FDIC Insured May Lose Value Not Bank Guaranteed RETIREMENT FIDUCIARY FOCUS TABLE OF CONTENTS 1 Employer Fee Responsibilities

USING ERISA ACCOUNTS TO HELP MANAGE FEE- RELATED FIDUCIARY RESPONSIBILITIES Not FDIC Insured May Lose Value Not Bank Guaranteed RETIREMENT FIDUCIARY FOCUS TABLE OF CONTENTS 1 Employer Fee Responsibilities

Managing Your Future

Managing Your Future A Guide to Managing Your Firm s Retirement Plan Alex Hargrave Senior Vice President RBC Dain Rauscher (415) 445-8400 alex.hargrave@rbcdain.com Mike Lucey Managing Partner Gordon &

Managing Your Future A Guide to Managing Your Firm s Retirement Plan Alex Hargrave Senior Vice President RBC Dain Rauscher (415) 445-8400 alex.hargrave@rbcdain.com Mike Lucey Managing Partner Gordon &

Topics Covered. Two Ways To Be A Fiduciary 5/6/2015

ERISA Fiduciary Duty For Human Resources Professionals: Managing Risk and Implementing Cynthia A. Moore Jordan Schreier Dickinson Wright PLLC Topics Covered Who is a Fiduciary? What are Fiduciary Duties?

ERISA Fiduciary Duty For Human Resources Professionals: Managing Risk and Implementing Cynthia A. Moore Jordan Schreier Dickinson Wright PLLC Topics Covered Who is a Fiduciary? What are Fiduciary Duties?

New Regulations Under ERISA Refine and Develop Fiduciary Duties Regarding the Investment of Plan Assets

New Regulations Under ERISA Refine and Develop Fiduciary Duties Regarding the Investment of Plan Assets Maine Employee Benefits Council December 4, 2008 Eric D. Altholz Verrill Dana, LLP Background There

New Regulations Under ERISA Refine and Develop Fiduciary Duties Regarding the Investment of Plan Assets Maine Employee Benefits Council December 4, 2008 Eric D. Altholz Verrill Dana, LLP Background There

Legal Obligations of Employers for 401(k) Plans

Plans") Legal Obligations of Employers for 401(k) Plans 1. Background A. After extensive investigation of 401(k) retirement plans throughout the country, the Department of Labor (DOL) has determined the following:

Legal Obligations of Employers for 401(k) Plans 1. Background A. After extensive investigation of 401(k) retirement plans throughout the country, the Department of Labor (DOL) has determined the following:

Understanding the Report of Indirect Compensation

Understanding the Report of Indirect Compensation Frequently Asked Questions On an annual basis, T. Rowe Price Retirement Plan Services, Inc. (RPS), distributes the Report of Indirect Compensation to assist

Understanding the Report of Indirect Compensation Frequently Asked Questions On an annual basis, T. Rowe Price Retirement Plan Services, Inc. (RPS), distributes the Report of Indirect Compensation to assist

Service Provider Fee Disclosure Rules Now Final: Next Steps for Retirement Plan Fiduciaries. March 2012

Service Provider Fee Disclosure Rules Now Final: Next Steps for Retirement Plan Fiduciaries March 2012 Table of Contents Service Provider Fee Disclosure Final Rules 2 Background 2 Significant Clarifications

Service Provider Fee Disclosure Rules Now Final: Next Steps for Retirement Plan Fiduciaries March 2012 Table of Contents Service Provider Fee Disclosure Final Rules 2 Background 2 Significant Clarifications

Understanding Plan Fees and Expenses

Understanding Plan Fees and Expenses Susan M. Wright, CPA, APM Executive Director, Consulting Topics of Discussion Fiduciary Responsibilities Settlor vs. Non-settlor Expenses Revenue Holding Accounts Questions

Understanding Plan Fees and Expenses Susan M. Wright, CPA, APM Executive Director, Consulting Topics of Discussion Fiduciary Responsibilities Settlor vs. Non-settlor Expenses Revenue Holding Accounts Questions

Understanding Your Fiduciary Role

Understanding Your Fiduciary Role Legal Aspects of Fiduciary Duties Under ERISA for Tax-Exempt Plan Sponsors Mark A. Daniele, Esq. McCarter & English, LLP January 26, 2012 I. ERISA ERISA imposes various

Understanding Your Fiduciary Role Legal Aspects of Fiduciary Duties Under ERISA for Tax-Exempt Plan Sponsors Mark A. Daniele, Esq. McCarter & English, LLP January 26, 2012 I. ERISA ERISA imposes various

Investment Policy Statements. for DC Plans

Investment Policy Statements Presented by: for DC Plans Linda Ruiz-Zaiko, President Bridgebay Financial, Inc. ruiz-zaiko@bridgebay.com www.bridgebay.com Marlow Kee, CPA Director of Finance PATH www.path.org

Investment Policy Statements Presented by: for DC Plans Linda Ruiz-Zaiko, President Bridgebay Financial, Inc. ruiz-zaiko@bridgebay.com www.bridgebay.com Marlow Kee, CPA Director of Finance PATH www.path.org

Fiduciary Risk Management for Plan Sponsors and Advisers

june 2012 perspectives Fiduciary Risk Management for Plan Sponsors and Advisers The recent recession and market volatility have changed the playing field for investors and for the financial institutions

june 2012 perspectives Fiduciary Risk Management for Plan Sponsors and Advisers The recent recession and market volatility have changed the playing field for investors and for the financial institutions

Plan Sponsor s Guide to. Retirement Plan Fees. R e t i r e m e n t p l a n s

Plan Sponsor s Guide to Retirement Plan Fees R e t i r e m e n t p l a n s 2007 StanCorp Equities, Inc. StanCorp Equities, Inc., member NASD/SIPC, distributes group variable annuity and group annuity contracts

Plan Sponsor s Guide to Retirement Plan Fees R e t i r e m e n t p l a n s 2007 StanCorp Equities, Inc. StanCorp Equities, Inc., member NASD/SIPC, distributes group variable annuity and group annuity contracts

ADVISER FEE DISCLOSURE KIT

ADVISR F DISCLOSUR KIT INTRODUCTION November 2010 DoL regulations require that advisers to 401(k) plans make fee disclosures to plan fiduciaries by July 16, 2011. These disclosures must meet the RISA 408(b)(2)

ADVISR F DISCLOSUR KIT INTRODUCTION November 2010 DoL regulations require that advisers to 401(k) plans make fee disclosures to plan fiduciaries by July 16, 2011. These disclosures must meet the RISA 408(b)(2)

401(k) Fiduciary Briefing

Fiduciary Briefing") 401(k) Fiduciary Briefing 7 Steps to Help Plan Sponsors Mitigate Risk Presented by: John A. Frisch, CPA/PFS, CFP, AIF, PPC TM President, & Managing Partner, Qualified Plans Common 401(k) Plan Objectives

401(k) Fiduciary Briefing 7 Steps to Help Plan Sponsors Mitigate Risk Presented by: John A. Frisch, CPA/PFS, CFP, AIF, PPC TM President, & Managing Partner, Qualified Plans Common 401(k) Plan Objectives

Fees, Expenses and Revenue Sharing: Regulation, Litigation, Legislation and Best Practices

Fees, Expenses and Revenue Sharing: Regulation, Litigation, Legislation and Best Practices presented by FREDRED REISH, ESQ ESQ. REISH & REICHER May 6, 2010 Plan Expenses and Compensation The trend is towards

Fees, Expenses and Revenue Sharing: Regulation, Litigation, Legislation and Best Practices presented by FREDRED REISH, ESQ ESQ. REISH & REICHER May 6, 2010 Plan Expenses and Compensation The trend is towards

A GUIDE TO RETIREMENT PLAN FEES & EXPENSES

A GUIDE TO RETIREMENT PLAN FEES & EXPENSES WHITE PAPER DECEMBER 2013 Brian A. Montanez, AIF, CPC PRINCIPAL, MULTNOMAH GROUP Ronald J. Triche, Esq., APM* ASSISTANT GENERAL COUNSEL & DIRECTOR OF GOVERNMENT

A GUIDE TO RETIREMENT PLAN FEES & EXPENSES WHITE PAPER DECEMBER 2013 Brian A. Montanez, AIF, CPC PRINCIPAL, MULTNOMAH GROUP Ronald J. Triche, Esq., APM* ASSISTANT GENERAL COUNSEL & DIRECTOR OF GOVERNMENT

Fiduciary Duties and Responsibilities

Be a Prudent Fiduciary How to Select, Monitor and Assure That Your Providers Properly Exercise their Responsibilities and Assume Appropriate ERISA and Contractual Liability John H. McKendry, Jr. WHO IS

Be a Prudent Fiduciary How to Select, Monitor and Assure That Your Providers Properly Exercise their Responsibilities and Assume Appropriate ERISA and Contractual Liability John H. McKendry, Jr. WHO IS

3(21) and (38) Fiduciary Outsourcing. Blake Willis, July Business Services Rick Keast, Redhawk Wealth Advisors

and (38) Fiduciary Outsourcing. Blake Willis, July Business Services Rick Keast, Redhawk Wealth Advisors") 3(21) and (38) Fiduciary Outsourcing Blake Willis, July Business Services Rick Keast, Redhawk Wealth Advisors 3(21) and 3(38) Fiduciary Outsourcing Presented by: Rick Keast Senior Vice President Business

3(21) and (38) Fiduciary Outsourcing Blake Willis, July Business Services Rick Keast, Redhawk Wealth Advisors 3(21) and 3(38) Fiduciary Outsourcing Presented by: Rick Keast Senior Vice President Business

Disclosure Brochure for Retirement Plan Fiduciaries

Disclosure Brochure for Retirement Plan Fiduciaries Important information regarding services and compensation for retirement plan assets invested in UBS Select and other assets held away from UBS Retirement

Disclosure Brochure for Retirement Plan Fiduciaries Important information regarding services and compensation for retirement plan assets invested in UBS Select and other assets held away from UBS Retirement

Vendor to Plan Fiduciary Investment and Fee/Compensation Disclosure

ADP RETIREMENT SERVICES Vendor to Plan Fiduciary Investment and Fee/Compensation Disclosure HR. Payroll. Benefits. Vendor to Plan Fiduciary Investment and Fee/Compensation Disclosure New vendor to plan

ADP RETIREMENT SERVICES Vendor to Plan Fiduciary Investment and Fee/Compensation Disclosure HR. Payroll. Benefits. Vendor to Plan Fiduciary Investment and Fee/Compensation Disclosure New vendor to plan

ERISA 408(b)(2) Retirement Plan Service Provider Disclosure Information

(2) Retirement Plan Service Provider Disclosure Information") ERISA 408(b)(2) Retirement Plan Service Provider Disclosure Information This information is being provided to you as the Plan Sponsor or other responsible fiduciary of a retirement plan ("Plan") subject

ERISA 408(b)(2) Retirement Plan Service Provider Disclosure Information This information is being provided to you as the Plan Sponsor or other responsible fiduciary of a retirement plan ("Plan") subject

Models of Advisor Fiduciary Responsibility: What Advisors Need to Know

Models of Advisor Fiduciary Responsibility: What Advisors Need to Know Ashish Shrestha Regional Director This information is provided for registered investment advisors and institutional investors and

Models of Advisor Fiduciary Responsibility: What Advisors Need to Know Ashish Shrestha Regional Director This information is provided for registered investment advisors and institutional investors and

Collective. Prepared by the Coalition of Collective. Investment Trusts

Collective Investment Trusts Prepared by the Coalition of Collective Investment Trusts Table of Contents Overview... 2 Collective Investment Trusts Defined... 3 Two Broad Types of Collective Trusts...

Collective Investment Trusts Prepared by the Coalition of Collective Investment Trusts Table of Contents Overview... 2 Collective Investment Trusts Defined... 3 Two Broad Types of Collective Trusts...

Lincoln Alliance Program Fee disclosures

Lincoln Alliance Program Fee disclosures Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates. Affiliates are separately responsible for their own financial

Lincoln Alliance Program Fee disclosures Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates. Affiliates are separately responsible for their own financial

Fiduciary Liability. Liability Case Studies & Strategies for 401(k) Plan Fiduciaries. 401(k) FIDUCIARY TOOLKIT. Prepared by The Wagner Law Group

Plan Fiduciaries. 401(k) FIDUCIARY TOOLKIT. Prepared by The Wagner Law Group") 401(k) FIDUCIARY TOOLKIT Sponsored by ishares Prepared by The Wagner Law Group Fiduciary Liability Liability Case Studies & Strategies for 401(k) Plan Fiduciaries IMPORTANT INFORMATION The Wagner Law Group

401(k) FIDUCIARY TOOLKIT Sponsored by ishares Prepared by The Wagner Law Group Fiduciary Liability Liability Case Studies & Strategies for 401(k) Plan Fiduciaries IMPORTANT INFORMATION The Wagner Law Group

Service Provider Disclosure

Service Provider 408(b)(2) Service Provider Disclosure What Plan Sponsors Need to Know By John Carnevale, JD, President & CEO, Sentinel Benefits & Financial Group Joshua Meltzer, CFP, ChFC, QPFC, CPC,

Service Provider 408(b)(2) Service Provider Disclosure What Plan Sponsors Need to Know By John Carnevale, JD, President & CEO, Sentinel Benefits & Financial Group Joshua Meltzer, CFP, ChFC, QPFC, CPC,

SAMPLE INSURANCE BROKER COMPENSATION DISCLOSURE

SAMPLE INSURANCE BROKER COMPENSATION DISCLOSURE (For Use by Insurance Brokers in Providing Disclosures To Retirement Plan Clients of Indirect Compensation Expected To Be Received From John Hancock Life

SAMPLE INSURANCE BROKER COMPENSATION DISCLOSURE (For Use by Insurance Brokers in Providing Disclosures To Retirement Plan Clients of Indirect Compensation Expected To Be Received From John Hancock Life

RETIREMENT INSIGHTS. Understanding your fiduciary role. A plan sponsor fiduciary guide

RETIREMENT INSIGHTS Understanding your fiduciary role A plan sponsor fiduciary guide ABOUT Perhaps no one topic in the employee benefits arena has drawn more attention and scrutiny over the last several

RETIREMENT INSIGHTS Understanding your fiduciary role A plan sponsor fiduciary guide ABOUT Perhaps no one topic in the employee benefits arena has drawn more attention and scrutiny over the last several

PLAN FEES: FEESResource Guide. what you need to know in today s environment. COMPONENTS of retirement plan expenses

RETIREMENT PLAN FEESResource Guide 2nd Edition PLAN FEES: what you need to know in today s environment COMPONENTS of retirement plan expenses How Dollars Flow between investment managers, plan providers,

RETIREMENT PLAN FEESResource Guide 2nd Edition PLAN FEES: what you need to know in today s environment COMPONENTS of retirement plan expenses How Dollars Flow between investment managers, plan providers,

Understanding Retirement Plan Fees and Expenses

Understanding Retirement Plan Fees and Expenses To view this and other EBSA publications, visit the agency s Web site at: www.dol.gov/ebsa. To order publications, contact us electronically at: www.askebsa.dol.gov.

Understanding Retirement Plan Fees and Expenses To view this and other EBSA publications, visit the agency s Web site at: www.dol.gov/ebsa. To order publications, contact us electronically at: www.askebsa.dol.gov.

Responsibilities of Qualified Plan Fiduciaries and Staying Out of Trouble: Prohibited Transactions

chapter 9 and Staying Out of Trouble: Prohibited Transactions 2014 by Richard A. Naegele (Updated: 10/17/2014) chapter 9 and Staying Out of Trouble: Prohibited Transactions Table of Contents Part I:...

chapter 9 and Staying Out of Trouble: Prohibited Transactions 2014 by Richard A. Naegele (Updated: 10/17/2014) chapter 9 and Staying Out of Trouble: Prohibited Transactions Table of Contents Part I:...

NAIFA Fact Sheet: DOL Expands Fiduciary Definition

NAIFA Fact Sheet: DOL Expands Fiduciary Definition The Department of Labor (DOL) has released its long anticipated Proposed Regulation to Address Conflicts of Interest, and is accepting public comments

NAIFA Fact Sheet: DOL Expands Fiduciary Definition The Department of Labor (DOL) has released its long anticipated Proposed Regulation to Address Conflicts of Interest, and is accepting public comments

FIDUCIARY LIABILITY INSURANCE, BONDING, AND SERVICE AGREEMENTS FOR SPONSORS

FIDUCIARY LIABILITY INSURANCE, BONDING, AND SERVICE AGREEMENTS FOR SPONSORS 2007 by: Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston, MA 02110

FIDUCIARY LIABILITY INSURANCE, BONDING, AND SERVICE AGREEMENTS FOR SPONSORS 2007 by: Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston, MA 02110

IPS RIA, LLC CRD No. 172840

IPS RIA, LLC CRD No. 172840 ADVISORY CLIENT BROCHURE 10000 N. Central Expressway Suite 1100 Dallas, Texas 75231 O: 214.443.2400 F: 214-443.2424 FORM ADV PART 2A BROCHURE 1/26/2015 This brochure provides

IPS RIA, LLC CRD No. 172840 ADVISORY CLIENT BROCHURE 10000 N. Central Expressway Suite 1100 Dallas, Texas 75231 O: 214.443.2400 F: 214-443.2424 FORM ADV PART 2A BROCHURE 1/26/2015 This brochure provides

How To Determine Reasonableness Of A 401(A) Plan Fee

Plan Fee") January 2012 Assessing reasonableness of 403(b) retirement plan fees: Best practices for defining Who, What, How and Why Making sense of retirement plan fees and determining if they are reasonable will

January 2012 Assessing reasonableness of 403(b) retirement plan fees: Best practices for defining Who, What, How and Why Making sense of retirement plan fees and determining if they are reasonable will

Retirement Plan Business Development - Proposal and Preparation

Retirement Plan Business Development Guide Prospecting ideas and talking points Brochure is limited to use with partners working with Standard Retirement Services and StanCorp Equities, subsidiaries of

Retirement Plan Business Development Guide Prospecting ideas and talking points Brochure is limited to use with partners working with Standard Retirement Services and StanCorp Equities, subsidiaries of

Custom Wealth Manager Wrap Fee Program Brochure

Custom Wealth Manager Wrap Fee Program Brochure March 30, 2016 Lincoln Financial Securities Corporation 1300 South Clinton St., Suite 150 Fort Wayne, IN 46802 (800) 258-3648 www.lfsecurities.com This wrap

Custom Wealth Manager Wrap Fee Program Brochure March 30, 2016 Lincoln Financial Securities Corporation 1300 South Clinton St., Suite 150 Fort Wayne, IN 46802 (800) 258-3648 www.lfsecurities.com This wrap

403(b) Retirement Plans New Rules, New Responsibilities

Retirement Plans New Rules, New Responsibilities") 403(b) Retirement Plans New Rules, New Responsibilities Kerry Bandow, CFA Sean Corry, CLU Webinar, Monday, Oct 4, 2010 Kerry Bandow, CFA Speakers Regional Pension Manager at The Standard Bellevue, WA Kerry.Bandow@standard.com

403(b) Retirement Plans New Rules, New Responsibilities Kerry Bandow, CFA Sean Corry, CLU Webinar, Monday, Oct 4, 2010 Kerry Bandow, CFA Speakers Regional Pension Manager at The Standard Bellevue, WA Kerry.Bandow@standard.com

Fiduciary toolkit for financial professionals

Fiduciary toolkit for financial professionals For financial advisor use only. Not for distribution to retail investors. Vanguard is your partner to help guide you and your clients in addressing fiduciary

Fiduciary toolkit for financial professionals For financial advisor use only. Not for distribution to retail investors. Vanguard is your partner to help guide you and your clients in addressing fiduciary

Managing fiduciary responsibility for plan sponsors

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

Managing fiduciary responsibility for plan sponsors Invesco PlanForward Foundations SM Putting fiduciary responsibility in action Contents 1 Defining fiduciary responsibility 4 Maximizing fiduciary protection

Form ADV Part 2A Brochure March 30, 2015

Item 1 Cover Page Form ADV Part 2A Brochure March 30, 2015 OneAmerica Securities, Inc. 433 North Capital Avenue Indianapolis, Indiana, 46204 Telephone: 877-285-3863, option 6# Website: www.oneamerica.com

Item 1 Cover Page Form ADV Part 2A Brochure March 30, 2015 OneAmerica Securities, Inc. 433 North Capital Avenue Indianapolis, Indiana, 46204 Telephone: 877-285-3863, option 6# Website: www.oneamerica.com

Understanding Fiduciary Responsibility in 401(k) Plans

Plans") RESOURCE EDGE TM Understanding Fiduciary Responsibility in 401(k) Plans A Guide for Financial Professionals INVESTMENT INSIGHTS PRACTICE BUILDING SOLUTIONS RETIREMENT RESOURCES The following information

RESOURCE EDGE TM Understanding Fiduciary Responsibility in 401(k) Plans A Guide for Financial Professionals INVESTMENT INSIGHTS PRACTICE BUILDING SOLUTIONS RETIREMENT RESOURCES The following information

UBS Financial Services Inc. DC Advisory Consulting Services Agreement

. DC Advisory Consulting Services Agreement This agreement ( Agreement ) describes the consulting services provided in the DC Advisory program ( DC Advisory ), an investment advisory service of. (the Firm,

. DC Advisory Consulting Services Agreement This agreement ( Agreement ) describes the consulting services provided in the DC Advisory program ( DC Advisory ), an investment advisory service of. (the Firm,

NC Supplemental Retirement Plans Investment Consultant Review North Carolina Retirement Systems Division

NC Supplemental Retirement Plans Investment Consultant Review North Carolina Retirement Systems Division Investment Consultant Review 2 Investment Consultant Review I. Investment Consultant RFP II. Current

NC Supplemental Retirement Plans Investment Consultant Review North Carolina Retirement Systems Division Investment Consultant Review 2 Investment Consultant Review I. Investment Consultant RFP II. Current

65% Effective 68% Effective 79% Effective

Plan Health Pro Average Company Average Company 401k Plan Joe Advisor Smith Consulting jadvisor@smithconsulting.com ph 555-555-5555 cell 555-555-5555 Diagnostic Assessment Report Scoring Summary Plan Health

Plan Health Pro Average Company Average Company 401k Plan Joe Advisor Smith Consulting jadvisor@smithconsulting.com ph 555-555-5555 cell 555-555-5555 Diagnostic Assessment Report Scoring Summary Plan Health

401(k) FEES LITIGATION AND BEST PRACTICES; DISCLOSURE TO PLAN PARTICIPANTS. September 2007

FEES LITIGATION AND BEST PRACTICES; DISCLOSURE TO PLAN PARTICIPANTS. September 2007") 401(k) FEES LITIGATION AND BEST PRACTICES; DISCLOSURE TO PLAN PARTICIPANTS September 2007 by: Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston,

401(k) FEES LITIGATION AND BEST PRACTICES; DISCLOSURE TO PLAN PARTICIPANTS September 2007 by: Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston,

UNITED STATES DISTRICT COURT DISTRICT OF MINNESOTA

UNITED STATES DISTRICT COURT DISTRICT OF MINNESOTA Roger Krueger, et al., Plaintiffs, v. Ameriprise Financial, Inc., et al., Defendants. Case No. 11-cv-2781 Judge Susan Richard Nelson NOTICE OF CLASS ACTION

UNITED STATES DISTRICT COURT DISTRICT OF MINNESOTA Roger Krueger, et al., Plaintiffs, v. Ameriprise Financial, Inc., et al., Defendants. Case No. 11-cv-2781 Judge Susan Richard Nelson NOTICE OF CLASS ACTION

Retirement Plan Investment Monitoring and Best Practices for Plan Sponsors

Retirement Plan Investment Monitoring and Best Practices for Plan Sponsors Tyrone Golatt Senior Regional Vice President Geoff Finkel Associate Account Executive 1 This material is not intended to give

Retirement Plan Investment Monitoring and Best Practices for Plan Sponsors Tyrone Golatt Senior Regional Vice President Geoff Finkel Associate Account Executive 1 This material is not intended to give

The Importance of Understanding and Monitoring Retirement Plan Fees and Expenses

Volume 2011 August 2 The Importance of Understanding and Monitoring Retirement Plan Fees and Expenses Profit sharing plans, 401(k) plans, and other types of defined contribution plans have become the predominant

Volume 2011 August 2 The Importance of Understanding and Monitoring Retirement Plan Fees and Expenses Profit sharing plans, 401(k) plans, and other types of defined contribution plans have become the predominant

Retirement Plan RFPs. John H. McKendry, Jr. & Heidi A. Lyon. Warner Norcross & Judd LLP 2011

Retirement Plan RFPs John H. McKendry, Jr. & Heidi A. Lyon Warner Norcross & Judd LLP 2011 OVERVIEW Legal Background Methods for Selecting Providers RFP Process 22 Steps and Considerations Provider Models

Retirement Plan RFPs John H. McKendry, Jr. & Heidi A. Lyon Warner Norcross & Judd LLP 2011 OVERVIEW Legal Background Methods for Selecting Providers RFP Process 22 Steps and Considerations Provider Models

INVESTMENT ADVISORY AGREEMENT

INVESTMENT ADVISORY AGREEMENT Ceera Investments, LLC ( Adviser ), a registered investment adviser under the Investment Adviser s Act of 1940 (the "Adviser s Act") agrees to act as an investment adviser

INVESTMENT ADVISORY AGREEMENT Ceera Investments, LLC ( Adviser ), a registered investment adviser under the Investment Adviser s Act of 1940 (the "Adviser s Act") agrees to act as an investment adviser

Determining reasonableness of retirement plan fees

Determining reasonableness of retirement plan fees Vanguard commentary September 2011 Fees paid for retirement plan investments and services have always been an important consideration for ERISA fiduciaries.

Determining reasonableness of retirement plan fees Vanguard commentary September 2011 Fees paid for retirement plan investments and services have always been an important consideration for ERISA fiduciaries.

Doing Your Homework: Understanding 401(k) Fees and Making Every Basis Point Count. by Pamela Hess and Valerie M. Kupferschmidt

Fees and Making Every Basis Point Count. by Pamela Hess and Valerie M. Kupferschmidt") Retirement Security Doing Your Homework: Understanding 401(k) Fees and Making Every Basis Point Count by Pamela Hess and Valerie M. Kupferschmidt Even though most plan sponsors realize they need to do

Retirement Security Doing Your Homework: Understanding 401(k) Fees and Making Every Basis Point Count by Pamela Hess and Valerie M. Kupferschmidt Even though most plan sponsors realize they need to do

15 Essential Steps. Fiduciary. Standard of Care. for the Financial Advisor s

15 Essential Steps for the Financial Advisor s Fiduciary Standard of Care In partnership with: Roger L. Levy, LLM, AIFA, of Cambridge Fiduciary Services, LLC i Introduction Your fiduciary duty, simplified.

15 Essential Steps for the Financial Advisor s Fiduciary Standard of Care In partnership with: Roger L. Levy, LLM, AIFA, of Cambridge Fiduciary Services, LLC i Introduction Your fiduciary duty, simplified.

MARK D. MENSACK, LLC. INDEPENDENT FIDUCIARYCONSULTING

MARK D. MENSACK, LLC. INDEPENDENT FIDUCIARYCONSULTING Introduction to Fiduciary Responsibility Fiduciary Responsibility: Why is it Hot?? Ever since the Enron and WorldCom debacles, Fiduciary Responsibility

MARK D. MENSACK, LLC. INDEPENDENT FIDUCIARYCONSULTING Introduction to Fiduciary Responsibility Fiduciary Responsibility: Why is it Hot?? Ever since the Enron and WorldCom debacles, Fiduciary Responsibility

DOL s Fiduciary Rule Increases Advisor Responsibility

New Frontiers For Advisors Who Lead the Way First Quarter 2016 DOL s Fiduciary Rule Increases Advisor Responsibility Industry interest has increased around the Department of Labor s (DOL) rule expanding

New Frontiers For Advisors Who Lead the Way First Quarter 2016 DOL s Fiduciary Rule Increases Advisor Responsibility Industry interest has increased around the Department of Labor s (DOL) rule expanding

Plan Administrator Guide

Plan Administrator Guide Your qualified retirement plan combines current employer tax savings with retirement security for participants. Congress specifically provided for this favorable treatment in the

Plan Administrator Guide Your qualified retirement plan combines current employer tax savings with retirement security for participants. Congress specifically provided for this favorable treatment in the

ABC PLAN 401(k) PLAN FEE DISCLOSURE FORM For Services Provided by XYZ Company 1

PLAN FEE DISCLOSURE FORM For Services Provided by XYZ Company 1") 1 Overview The Employee Retirement Income Security Act of 1974, as amended (ERISA) requires employee benefit plan fiduciaries to act solely in the interests of, and for the exclusive benefit of, plan participants

1 Overview The Employee Retirement Income Security Act of 1974, as amended (ERISA) requires employee benefit plan fiduciaries to act solely in the interests of, and for the exclusive benefit of, plan participants

Johanson Financial Advisors, Inc. 2105 South Bascom Avenue, Suite 255 Campbell, CA 95008. Firm Contact: Lynda Tu Chief Compliance Officer

Part 2A of Form ADV: Firm Brochure Item 1: Cover Page June 2015 Johanson Financial Advisors, Inc. 2105 South Bascom Avenue, Suite 255 Campbell, CA 95008 Firm Contact: Lynda Tu Chief Compliance Officer

Part 2A of Form ADV: Firm Brochure Item 1: Cover Page June 2015 Johanson Financial Advisors, Inc. 2105 South Bascom Avenue, Suite 255 Campbell, CA 95008 Firm Contact: Lynda Tu Chief Compliance Officer

Fiduciary Guide. Helping to protect your plan. MetLife Resources

Fiduciary Guide Helping to protect your plan. MetLife Resources Table of Contents Introduction..........................................................................1 MetLife s Commitment.................................................................

Fiduciary Guide Helping to protect your plan. MetLife Resources Table of Contents Introduction..........................................................................1 MetLife s Commitment.................................................................

Bullet Proof. A Fiduciary s Guide to Oversight

Bullet Proof Your Retirement Plan: A Fiduciary s Guide to Oversight Financial Executives International Northeastern Wisconsin Chapter Professional Development Session January 20, 2011 Francis Investment

Bullet Proof Your Retirement Plan: A Fiduciary s Guide to Oversight Financial Executives International Northeastern Wisconsin Chapter Professional Development Session January 20, 2011 Francis Investment

401(k) Plan Administration: Fiduciary Responsibility and The Impact of Changes to Your Plan

Plan Administration: Fiduciary Responsibility and The Impact of Changes to Your Plan") 401(k) Plan Administration: Fiduciary Responsibility and The Impact of Changes to Your Plan Presented by: Kirsten L. Vignec Shareholder Hill Ward Henderson Introduction Our discussion today focuses on

401(k) Plan Administration: Fiduciary Responsibility and The Impact of Changes to Your Plan Presented by: Kirsten L. Vignec Shareholder Hill Ward Henderson Introduction Our discussion today focuses on

INTERNATIONAL ACTUARIAL ASSOCIATION COLLOQUIUM OSLO, NORWAY TUESDAY, JUNE 9, 2015

INTERNATIONAL ACTUARIAL ASSOCIATION COLLOQUIUM OSLO, NORWAY TUESDAY, JUNE 9, 2015 PLAN FEES AND CHARGES: CURRENT ISSUES IN THE U.S. AND MANAGING TRANSPARENCY RISKS TO AVOID HIDDEN FEE LITIGATION JEFFREY

INTERNATIONAL ACTUARIAL ASSOCIATION COLLOQUIUM OSLO, NORWAY TUESDAY, JUNE 9, 2015 PLAN FEES AND CHARGES: CURRENT ISSUES IN THE U.S. AND MANAGING TRANSPARENCY RISKS TO AVOID HIDDEN FEE LITIGATION JEFFREY

New Fee Disclosure Regulation Magnifies Fiduciary Risks for 401(k) Plan Sponsors

Plan Sponsors") Fiduciary Insights New Fee Disclosure Regulation Magnifies Fiduciary Risks for 401(k) Plan Sponsors COST ASSIGNMENT DECISIONS EXPENSE CONTROLS CONFLICTS OF INTEREST INVESTMENT SELECTION CONSTRAINTS FEE

Fiduciary Insights New Fee Disclosure Regulation Magnifies Fiduciary Risks for 401(k) Plan Sponsors COST ASSIGNMENT DECISIONS EXPENSE CONTROLS CONFLICTS OF INTEREST INVESTMENT SELECTION CONSTRAINTS FEE

Form ADV Part 2A Disclosure Brochure

Form ADV Part 2A Disclosure Brochure Cover Page Name of Registered Investment Advisor Asset Planning Corporation Address 234 S. Peters Road, Suite 102 Knoxville, TN 37923 Phone Number (888) 690-1231 Website

Form ADV Part 2A Disclosure Brochure Cover Page Name of Registered Investment Advisor Asset Planning Corporation Address 234 S. Peters Road, Suite 102 Knoxville, TN 37923 Phone Number (888) 690-1231 Website

The Department of Labor ( DOL ) recently issued proposed regulations

recently issued proposed regulations") Proposed Labor Regulations Would Require Greater Disclosures of Fees, Compensation, and Conflicts of Interest for Employee Benefit Plan Services Providers PETER M. VARNEY AND PATRICK C. DICARLO The authors

Proposed Labor Regulations Would Require Greater Disclosures of Fees, Compensation, and Conflicts of Interest for Employee Benefit Plan Services Providers PETER M. VARNEY AND PATRICK C. DICARLO The authors

Retirement Plan Fee Disclosure:

Retirement Plan Fee Disclosure: Preparing for Participant Questions The time clock for fee disclosure is ticking. Starting in 2012, the U.S. Department of Labor (DOL) is requiring retirement plan administrators

Retirement Plan Fee Disclosure: Preparing for Participant Questions The time clock for fee disclosure is ticking. Starting in 2012, the U.S. Department of Labor (DOL) is requiring retirement plan administrators

Jarus Wealth Advisors LLC

Jarus Wealth Advisors LLC Firm Brochure - Form ADV Part 2A This brochure provides information about the qualifications and business practices of Jarus Wealth Advisors LLC. If you have any questions about

Jarus Wealth Advisors LLC Firm Brochure - Form ADV Part 2A This brochure provides information about the qualifications and business practices of Jarus Wealth Advisors LLC. If you have any questions about

Rockhaven Capital Management, LLC 132 Rock Haven Lane Pittsburgh, PA 15228 412-260- 7917 www.rockhavencapital.com 09/30/12

Item 1 Cover Page Rockhaven Capital Management, LLC 132 Rock Haven Lane Pittsburgh, PA 15228 412-260- 7917 www.rockhavencapital.com 09/30/12 This Brochure provides information about the qualifications

Item 1 Cover Page Rockhaven Capital Management, LLC 132 Rock Haven Lane Pittsburgh, PA 15228 412-260- 7917 www.rockhavencapital.com 09/30/12 This Brochure provides information about the qualifications

Inside the Structure of Defined Contribution/401(k) Plan Fees, 2013: A study assessing the mechanics of the all-in fee

Plan Fees, 2013: A study assessing the mechanics of the all-in fee") Conducted by Deloitte Consulting LLP for the Investment Company Institute August 2014 Inside the Structure of Defined Contribution/401(k) Plan Fees, 2013: A study assessing the mechanics of the all-in

Conducted by Deloitte Consulting LLP for the Investment Company Institute August 2014 Inside the Structure of Defined Contribution/401(k) Plan Fees, 2013: A study assessing the mechanics of the all-in

RETIREMENT PLAN CONSULTING SERVICES PROGRAM

UBS Financial Services Inc. SEC File Number 801-7163 1000 Harbor Boulevard March 31, 2015 Weehawken, NJ 07086 (201)352-3000 http://financialservicesinc.ubs.com RETIREMENT PLAN CONSULTING SERVICES PROGRAM

UBS Financial Services Inc. SEC File Number 801-7163 1000 Harbor Boulevard March 31, 2015 Weehawken, NJ 07086 (201)352-3000 http://financialservicesinc.ubs.com RETIREMENT PLAN CONSULTING SERVICES PROGRAM

Since September 11, 2006, at least ten ERISAbased

ERISA-Based Class Actions Attack Fees Charged to 401(k) Plans: But Are They Really Just Excessive Fee Cases? By Paul Ondrasik, Melanie Nussdorf, and Eric Serron Since September 11, 2006, at least ten ERISAbased

ERISA-Based Class Actions Attack Fees Charged to 401(k) Plans: But Are They Really Just Excessive Fee Cases? By Paul Ondrasik, Melanie Nussdorf, and Eric Serron Since September 11, 2006, at least ten ERISAbased

DISCRETIONARY INVESTMENT ADVISORY AGREEMENT

DISCRETIONARY INVESTMENT ADVISORY AGREEMENT This Discretionary Investment Advisory Agreement (this Agreement ) is between (the "Client") and LEONARD L. GOLDBERG d/b/a GOLDBERG CAPITAL MANAGEMENT, a sole

DISCRETIONARY INVESTMENT ADVISORY AGREEMENT This Discretionary Investment Advisory Agreement (this Agreement ) is between (the "Client") and LEONARD L. GOLDBERG d/b/a GOLDBERG CAPITAL MANAGEMENT, a sole

Executive Summary Definition of the Term Fiduciary U.S. Department of Labor Conflict of Interest Rule 1. April 15, 2016

Executive Summary Definition of the Term Fiduciary U.S. Department of Labor Conflict of Interest Rule 1 April 15, 2016 I. Introduction. Background. The U.S. Department of Labor (the Department or DOL )

Executive Summary Definition of the Term Fiduciary U.S. Department of Labor Conflict of Interest Rule 1 April 15, 2016 I. Introduction. Background. The U.S. Department of Labor (the Department or DOL )

Best Practices for Investment Committee Members

Best Practices for Investment Committee Members Brightscape Erisamyliability.com Eric Weiss, CFP, AIF This paper identifies best practices for 401(k) investment committee members in order to reduce potential

Best Practices for Investment Committee Members Brightscape Erisamyliability.com Eric Weiss, CFP, AIF This paper identifies best practices for 401(k) investment committee members in order to reduce potential

Clear Perspectives Financial Planning, LLC Firm Brochure

Clear Perspectives Financial Planning, LLC Firm Brochure This brochure provides information about the qualifications and business practices of Clear Perspectives Financial Planning, LLC. If you have any

Clear Perspectives Financial Planning, LLC Firm Brochure This brochure provides information about the qualifications and business practices of Clear Perspectives Financial Planning, LLC. If you have any

Account Fees: Fee. Physical Certificate Fee Check Delivery. Fees. Outgoing fed wire fee

ERISA Section 408(b)(2) Disclosure Document Brokerage Services Introduction: This disclosure document (this Disclosure Document ) provides an overview of the fees and other compensation charged for or

ERISA Section 408(b)(2) Disclosure Document Brokerage Services Introduction: This disclosure document (this Disclosure Document ) provides an overview of the fees and other compensation charged for or

Fee disclosure Q&A: Answering plan sponsor questions about Department of Labor regulations

Fee disclosure Q&A: Answering plan sponsor questions about Department of Labor regulations Spring 2012 U.S. Department of Labor (DOL) regulations outlining obligations of plan sponsors and service providers

Fee disclosure Q&A: Answering plan sponsor questions about Department of Labor regulations Spring 2012 U.S. Department of Labor (DOL) regulations outlining obligations of plan sponsors and service providers

The Re-Emergence of Collective Investment Trust Funds

Manning & Napier Advisors, LLC The Re-Emergence of Collective Investment Trust Funds June 2011 Manning & Napier Advisors, LLC provides investment advisory services to Exeter Trust Company ( ETC ), Trustee

Manning & Napier Advisors, LLC The Re-Emergence of Collective Investment Trust Funds June 2011 Manning & Napier Advisors, LLC provides investment advisory services to Exeter Trust Company ( ETC ), Trustee

Prudent Investing and ERISA: Fees and the Fiduciary Duty of Care

y Prudent Investing and ERISA: Fees and the Fiduciary Duty of Care by Melanie L. Fein Fein Law Office Washington, DC MAY 2015 1 June 2, 2015 Prudent Investing and ERISA: Fees and the Fiduciary Duty of

y Prudent Investing and ERISA: Fees and the Fiduciary Duty of Care by Melanie L. Fein Fein Law Office Washington, DC MAY 2015 1 June 2, 2015 Prudent Investing and ERISA: Fees and the Fiduciary Duty of

Firm Brochure (Form ADV Part 2A) 12610 N. Community Road, Suite 204 Charlotte, NC 28277 704-540-2500. www.independentadvisoralliance.

12610 N. Community Road, Suite 204 Charlotte, NC 28277 704-540-2500. www.independentadvisoralliance.") Firm Brochure (Form ADV Part 2A) 12610 N. Community Road, Suite 204 Charlotte, NC 28277 704-540-2500 www.independentadvisoralliance.com October 21, 2015 This brochure provides information about the qualifications

Firm Brochure (Form ADV Part 2A) 12610 N. Community Road, Suite 204 Charlotte, NC 28277 704-540-2500 www.independentadvisoralliance.com October 21, 2015 This brochure provides information about the qualifications

Fiduciary Recordkeeping Playbook: A Plan Sponsor s Guide to 401(k) Plans. Plan Administrators, Inc.

Plans. Plan Administrators, Inc.") Fiduciary Recordkeeping Playbook: A Plan Sponsor s Guide to 401(k) Plans Plan Administrators, Inc. Table of Contents Putting Together a 401(k) Game Plan...3 Rules for 401(k) Fiduciaries...4 Your Fiduciary

Fiduciary Recordkeeping Playbook: A Plan Sponsor s Guide to 401(k) Plans Plan Administrators, Inc. Table of Contents Putting Together a 401(k) Game Plan...3 Rules for 401(k) Fiduciaries...4 Your Fiduciary

Ameriprise Strategic Portfolio Service Advantage Client Agreement

Provide this form to the client. Do NOT send it to the Corporate Office. Ameriprise Strategic Portfolio Service Advantage Client Agreement 1. Overview of Ameriprise Managed Accounts Ameriprise Financial

Provide this form to the client. Do NOT send it to the Corporate Office. Ameriprise Strategic Portfolio Service Advantage Client Agreement 1. Overview of Ameriprise Managed Accounts Ameriprise Financial

Broker-Dealer and Registered Investment Advisor Fee Disclosure of the Transamerica Financial Group Division of TFA

Broker-Dealer and Registered Investment Advisor Fee Disclosure of the Transamerica Financial Group Division of TFA This disclosure summarizes fees and other compensation received by Transamerica Financial

Broker-Dealer and Registered Investment Advisor Fee Disclosure of the Transamerica Financial Group Division of TFA This disclosure summarizes fees and other compensation received by Transamerica Financial

Choosing a 401k plan Advisor?

Choosing a 401k plan Advisor? Why is choosing a 401k service provider and/or a 401k plan Advisor a major decision? Because unlike most day to day work-related decisions these are fiduciary decisions. A

Choosing a 401k plan Advisor? Why is choosing a 401k service provider and/or a 401k plan Advisor a major decision? Because unlike most day to day work-related decisions these are fiduciary decisions. A

F I R M B R O C H U R E

Part 2A of Form ADV: F I R M B R O C H U R E Dated: 03/24/2015 Contact Information: Bob Pfeifer, Chief Compliance Officer Post Office Box 2509 San Antonio, TX 78299 2509 Phone Number: (210) 220 5070 Fax

Part 2A of Form ADV: F I R M B R O C H U R E Dated: 03/24/2015 Contact Information: Bob Pfeifer, Chief Compliance Officer Post Office Box 2509 San Antonio, TX 78299 2509 Phone Number: (210) 220 5070 Fax

ERISA 408(b)(2) Disclosure Statement

(2) Disclosure Statement") This Fee Disclosure Guide 1 contains a description of services provided to plans and/or its participants as well as sources of compensation received by us or our affiliates which details are set forth

This Fee Disclosure Guide 1 contains a description of services provided to plans and/or its participants as well as sources of compensation received by us or our affiliates which details are set forth

Cambridge Investment Research Advisors, Inc. 1776 Pleasant Plain Road Fairfield, IA 52556 800-777-6080 www.cir2.com. Date of Brochure: September, 2013

Item 1 - Cover Page 1776 Pleasant Plain Road Fairfield, IA 52556 800-777-6080 www.cir2.com Date of Brochure: September, 2013 This brochure provides information about the qualifications and business practices

Item 1 - Cover Page 1776 Pleasant Plain Road Fairfield, IA 52556 800-777-6080 www.cir2.com Date of Brochure: September, 2013 This brochure provides information about the qualifications and business practices

ERISA Compliance for Investment Advisers: A Q&A Guide To DOL s 408(b)(2) Disclosure Regulation

(2) Disclosure Regulation") Vol. 20, No. 7 July 2013 ERISA Compliance for Investment Advisers: A Q&A Guide To DOL s 408(b)(2) Disclosure Regulation By Michael L. Hadley and Joshua R. Landsman O n February 2, 2012, the Department

Vol. 20, No. 7 July 2013 ERISA Compliance for Investment Advisers: A Q&A Guide To DOL s 408(b)(2) Disclosure Regulation By Michael L. Hadley and Joshua R. Landsman O n February 2, 2012, the Department

401K Plan Fee Regulations: From Paper to Practice

401K Plan Fee Regulations: From Paper to Practice FEATURED FACULTY: Matthew I. Whitehorn, Esq., Partner, Dilworth Paxson LLP 215-575-7166 mwhitehorn@dilworthlaw.com Elizabeth J. Goldstein, Esq., Partner,

401K Plan Fee Regulations: From Paper to Practice FEATURED FACULTY: Matthew I. Whitehorn, Esq., Partner, Dilworth Paxson LLP 215-575-7166 mwhitehorn@dilworthlaw.com Elizabeth J. Goldstein, Esq., Partner,

A Prudent Response to New 401(k) Developments

Developments") A Prudent Response to New 401(k) Developments By Fred Reish Partner, Drinker Biddle & Reath LLP PlanAdvisorTools.com A Prudent Response to New 401(k) Developments by Fred Reish Partner, Drinker Biddle

A Prudent Response to New 401(k) Developments By Fred Reish Partner, Drinker Biddle & Reath LLP PlanAdvisorTools.com A Prudent Response to New 401(k) Developments by Fred Reish Partner, Drinker Biddle

Key Points IBDs, RIAs and Advisors Need to Know

Review of the Department of Labor s (DOL) Final Definition of Fiduciary Key Points IBDs, RIAs and Advisors Need to Know Contents Three Key Points... 1 The Basic Framework of the Final Rule... 3 DOL s Final

Review of the Department of Labor s (DOL) Final Definition of Fiduciary Key Points IBDs, RIAs and Advisors Need to Know Contents Three Key Points... 1 The Basic Framework of the Final Rule... 3 DOL s Final

Retirement Plan Business Development Guide

Retirement Plan Business Development Guide Prospecting Ideas And Talking Points This brochure is limited to use with partners working with Standard Retirement Services and StanCorp Equities, Inc., subsidiaries

Retirement Plan Business Development Guide Prospecting Ideas And Talking Points This brochure is limited to use with partners working with Standard Retirement Services and StanCorp Equities, Inc., subsidiaries

VERDE WEALTH GROUP, LLC

VERDE WEALTH GROUP, LLC 2323 S. Shepherd Dr. Suite 845 Houston, TX 77019 www.verdewealthgroup.com This brochure provides information about the qualifications and business practices of Verde Wealth Group,

VERDE WEALTH GROUP, LLC 2323 S. Shepherd Dr. Suite 845 Houston, TX 77019 www.verdewealthgroup.com This brochure provides information about the qualifications and business practices of Verde Wealth Group,

Best practices for confident plan compliance

Best practices for confident plan compliance Ongoing efforts to expand retirement plan participation, promote transparency and enhance benefit security have increased responsibilities for plan sponsors.

Best practices for confident plan compliance Ongoing efforts to expand retirement plan participation, promote transparency and enhance benefit security have increased responsibilities for plan sponsors.

What is a IFA Retirement Plan?

Retirement Plan Solution 401k Guided Simple Transparent Guided Simple Transparent IFA Retirement Plan Solution Bringing best practices to small and mid-sized company retirement plans. Our focus is on protecting

Retirement Plan Solution 401k Guided Simple Transparent Guided Simple Transparent IFA Retirement Plan Solution Bringing best practices to small and mid-sized company retirement plans. Our focus is on protecting

Log. Present by RPAG Member:

Log Present by RPAG Member: Robert Greulich Managing Member The Pinnacle Planning Group, LLC (630)684-8562 Robert.Greulich@ThePinnaclePlanningGroup.com @ 2013 Retirement Plan Advisory Group. All rights

Log Present by RPAG Member: Robert Greulich Managing Member The Pinnacle Planning Group, LLC (630)684-8562 Robert.Greulich@ThePinnaclePlanningGroup.com @ 2013 Retirement Plan Advisory Group. All rights

Clients of Asset Planning Corporation

DATE: October 2014 TO: FROM: Clients of Asset Planning Corporation Paul K. Fain, III, CFP, President Asset Planning Corporation (APC) is registered with the Securities and Exchange Commission (SEC) as

DATE: October 2014 TO: FROM: Clients of Asset Planning Corporation Paul K. Fain, III, CFP, President Asset Planning Corporation (APC) is registered with the Securities and Exchange Commission (SEC) as