A Guide to Understanding AmerUs Life s EIL Products

|

|

|

- Sheila Newman

- 8 years ago

- Views:

Transcription

1 A Guide to Understanding AmerUs Life s EIL Products

2 REWARD WITHOUT MARKET RISK Introduced in 1995, equity indexed products are relatively new to the financial services world. In their short life span, individuals who own equity indexed products have found that they add value and stability to their portfolios. Purchasing equity indexed products, however, first means understanding what they are, how they are designed to work and for whom they are tailored. AmerUs Life Insurance Company 611 Fifth Avenue Des Moines, IA 50309

3 THE ADVANTAGE OF EQUITY INDEXED LIFE The most significant advantage of Equity Indexed Life Insurance (EIL) is that it combines most of the features, benefits and security of traditional life insurance with the potential to earn interest based on the upward movement of an equity index. Instead of the Company declaring a specific interest rate or dividend as with traditional life insurance, interest earnings are credited based on increases in value of a specific equity index. The Standard & Poor s 500 Composite Stock Price Index* (excluding dividends) is used as the index for AmerUs Life s EIL products. The S&P 500 Index is currently the most commonly used index for EILs. Credited interest is linked to increases in the S&P 500 Index without the downside risks associated with investing directly in the stock market. And, because EILs are permanent life insurance plans, they provide features which give you a sense of stability through: A guaranteed minimum interest rate Tax-deferred interest accumulation Access to cash value through withdrawal and loan provisions In addition, the equity indexed link in EIL products offers important benefits: Equity index-linked returns with the potential to beat inflation Protection in the contract against downside market risk WHO CAN BENEFIT FROM EILS The typical profiles of EIL buyers are individuals who: Want affordable protection with strong cash value accumulation potential. Want built-in product flexibility to better accommodate changing financial circumstances. Want the security and attractive interest potential provided by AmerUs Life equity indexed life insurance products. EIL Buyer Risk Profile Conservative to Aggressive Whole Life Universal Life Fixed Premium Equity Indexed Life Equity Indexed Universal Life Variable Universal Life Equity indexed life insurance is an alternative that fits in between traditional fixed life plans and variable universal life plans. Determining your comfort level for market risk is important when considering which type of life insurance plan is most appropriate for you. * Standard & Poor s, S&P, S&P 500, Standard & Poor s 500 and 500 are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by AmerUs Life Insurance Company. AmerUs Life s EIL products are not sponsored, endorsed, sold or promoted by Standard & Poor s, and Standard & Poor s makes no representation regarding the advisability of purchasing these products. 1

is used as the index for AmerUs Life s EIL products. The S&P 500 Index is currently the most commonly used index for EILs.")

4 The S&P 500 Composite Stock Price Index is often regarded as the standard for broad stock market performance. It is used to measure the average stock price changes of the 500 most widely held companies representing over 100 specific industry groups. The S&P 500 Index represents approximately 70% of the total domestic U.S. equity market s capitalization. Historically, the S&P 500 Index has outperformed fixed interest products such as corporate and government bonds and CDs. The Opportunities of an Equity Index Equity indexed life insurance offers the upside potential of stock market performance and a guard against downside risk with a guaranteed minimum interest rate. The chart below demonstrates how different asset vehicles have performed during a 45-year period. It depicts the growth of one dollar placed in hypothetical assets tied to the S&P 500 Index, Treasury Bonds, Treasury Bills, and the inflation rate over a period from 1958 through S&P 500 Index Treasury Bonds Treasury Bills Inflation $1 linked to the performance of the S&P 500 and two other assets compared to inflation The chart reflects the historical growth of the S&P 500 Index, 10-Year U.S. Treasury Bonds, 30-Day U.S. Treasury Bills and the Consumer Price Index Inflation Rate. The S&P 500 Index does not include dividend earnings. Past performance is no guarantee of future performance or of values of equity indexed life insurance. This chart is not intended to illustrate interest earnings under AmerUs Life s EIL plans. The growth rates shown do not reflect the impact of participation rates and cap rates (as described within this guide) which would affect actual credited interest earnings in any given market environment. CDs offered by banks are insured by a government agency and offer a fixed rate of return. The principal and yield of corporate and government bonds are not insured and will fluctuate with changes of the market price and return of underlying securities. Source: Standard & Poor s, U.S. Bureau of Labor Statistics 2

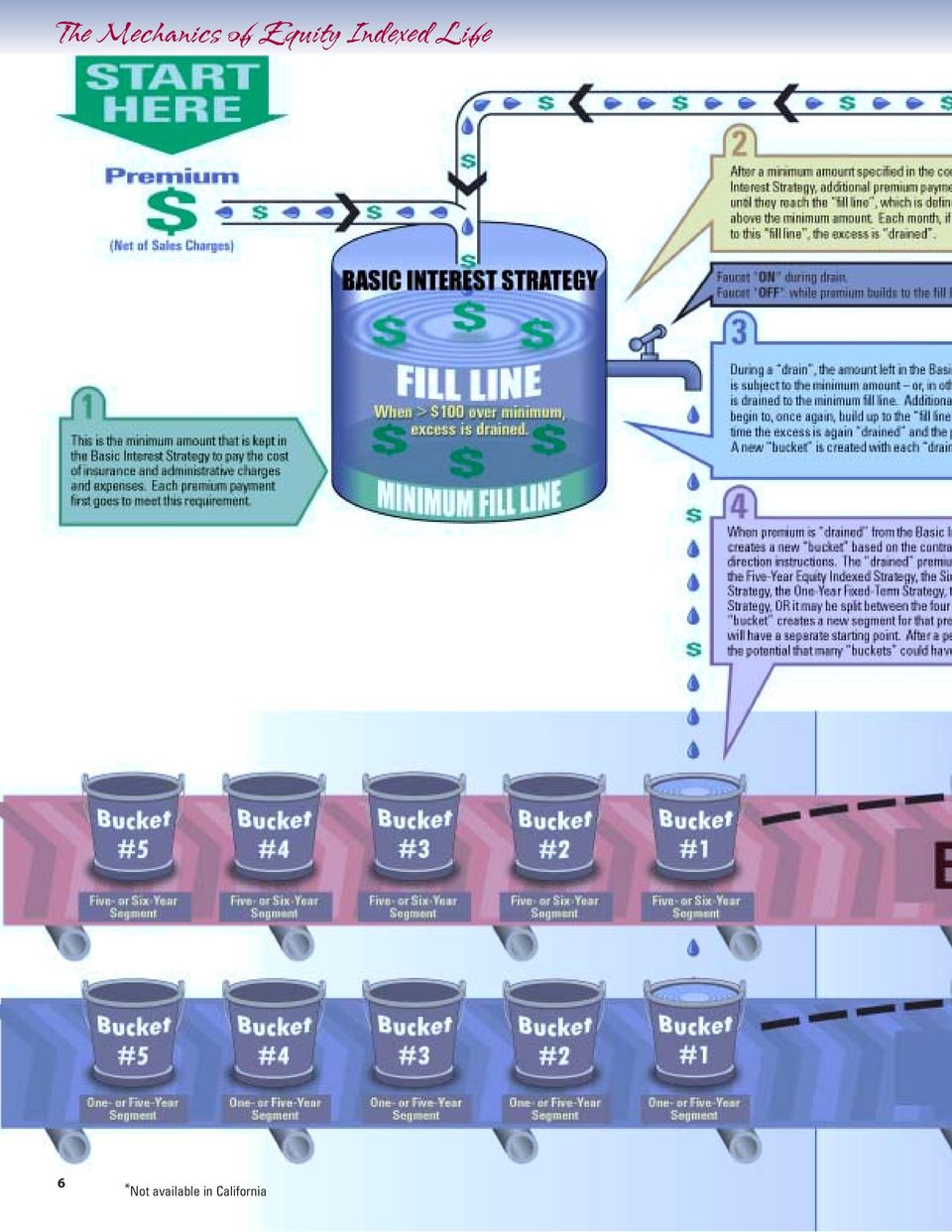

5 With Equity Indexed Life Insurance, you can direct your premium payments to interest crediting strategies that are consistent with your preferences. 1. One-Year Fixed-Term Strategy* 2. Five-Year Fixed-Term Strategy* 3. Five-Year Equity Indexed Strategy 4. Six-Year Equity Indexed Strategy HOW THE STRATEGIES WORK See a more in-depth, visual explanation on page 6. All net premiums paid are initially placed directly into the Basic Interest Strategy. At least once per month, part of the Basic Interest Strategy value may be directed to a new One- Year Fixed-Term Strategy, Five- Year Fixed-Term Strategy, Five- Year Equity Indexed Strategy and/or a new Six-Year Equity- Indexed Strategy, subject to the minimum value required to be kept in the Basic Interest Strategy. $ Each premium direction creates a new segment based on the strategy(ies) chosen. This means, for example, that for any amounts directed to the Five-Year Fixed-Term Strategy, those funds will remain in that segment of the policy for five years. The direction may be changed for new premiums, or it can remain unchanged from prior segments. Furthermore, when each segment reaches its maturity, its value flows back into the Basic Interest Strategy and will be redirected, along with any new premium, based on the client's choices of interest crediting strategies at that time. * May not be available in all states 3

6 UNDERSTANDING THE INTEREST CREDITING STRATEGIES Basic Interest Strategy Net premium is initially paid into the Basic Interest Strategy, from which insurance and administrative charges and policy expenses are paid. This strategy earns interest (as declared by the Company) and, as long as premiums continue, certain amounts will be held in this strategy to cover future insurance and administrative charges. The premiums in the Basic Interest Strategy will earn an interest rate which may fluctuate on a daily basis, but will never be less than the minimum rate guaranteed in the contract. The policyholder elects how the excess Basic Interest Strategy values will be directed to the other available strategies. AmerUs Life will not sweep any amounts less than $100. Regardless of mode, before any premium directions are made into the other strategies, a minimum balance in the Basic Interest Strategy approximately equal to one year s policy charges is required. 1. One-Year Fixed-Term Interest Strategy Each premium directed to this strategy creates a distinct one-year fixed term segment. Over time, policyholders will generally have a number of one-year fixed term segments within their policy. The interest rate for each one-year fixed term segment created is guaranteed for that one-year period. 2. Five-Year Fixed-Term Interest Strategy Each premium directed to this strategy creates a distinct five-year fixed-term segment. Over time, policyholders will generally have a number of five-year fixed term segments within their policy. Other than the minimum contract guarantee, the current interest rate for the Five-Year Fixed-Term Strategy is not guaranteed. AmerUs Life s current practice is to maintain a constant interest rate for each five-year fixed segment. 3. Five-Year Equity Indexed Strategy 4. Six-Year Equity Indexed Strategy In these strategies, interest earnings are linked to growth in the S&P 500 Composite Stock Price Index (excluding dividends) and are subject to a participation rate (guaranteed at 100%) and a maximum earnings rate that can change at the beginning of each segment earnings period. In addition, the Equity Indexed Strategies include the following features: Principal Protection: Premiums directed to an Equity Indexed Strategy are protected from a downturn in the index. Lock-In of Earnings: Each premium directed to the Five-Year Equity Indexed Strategy creates a new five-year segment. Index linked earnings are calculated and credited each 12 months on the funds in a segment. In effect, we lock in any index-linked earnings every 12 months within a segment and protect them from potential future downturns in the equity index. Each premium directed to the Six-Year Equity Indexed Strategy creates a new six-year segment. Index linked earnings are calculated and credited each 24 months on the funds in a segment. A greater earnings potential is available as indexed earnings are locked in every 24 months within a segment and protected from potential future downturns in the equity index.* Interest Rate Guarantee: For the Equity Indexed Strategies, each segment has a minimum guaranteed interest rate. Interest is credited at the end of the segment term under this guarantee if the value of the segment at that time is not at least equal to the premium (less any withdrawals or deductions), compounded annually at the minimum guaranteed interest rate. May not be available in all states * Values withdrawn during an earnings period, including monthly deductions taken from equity indexed segments, will not be credited with index earnings. 4

7 100% PARTICIPATION RATE AmerUs Life EIL policies guarantee that the participation rate will be 100% for the life of the contract. CAP RATES Index Increase (If any) Each earnings period, the segment's equity-linked interest earnings are subject to a cap rate (or an annual account value growth limit), as specified in the contract. The cap is the maximum earnings rate that will be credited to a segment for the earnings period. The cap rate may be reset for each segment at the beginning of an earnings period, and at the discretion of the Company. Individual segments may have different cap rates assigned. Interest Earnings Cannot Exceed Any Cap Participation Rate Interest Rate Credited (subject to the annual cap) Example: If the cap rate is 11%, and the index earnings are 12%, you would receive 11% credited to your plan, not 112%. MONTHLY DEDUCTIONS All monthly deductions are first deducted from the Basic Interest Strategy. However, if sufficient values are not maintained in the Basic Interest Strategy, deductions are then taken from the most recently established segment to the oldest segment of the strategies in this order: One-Year Fixed-Term Strategy, Five-Year Fixed- Term Strategy, Five-Year Equity Indexed Strategy, and then the Six-Year Equity Indexed Strategy. If sufficient policy values are still not available (and any minimum premium requirement has not been met), the policy will lapse. 5

8 6 *Not available in California

9 7

10 The method used to measure index growth is a major driver of product performance because the interest credited is directly tied to the index growth. AmerUs Life uses the Point-to-Point crediting method, whereas several competitors use the Averaging Annual Reset method. With Point-to-Point, you can more easily understand how the credited rate is determined without having to decipher calculations for the average change in the index over time. In addition, Averaging Annual Reset tends to reduce the ultimate credited rate in a steadily increasing index environment. POINT-TO-POINT The Point-to-Point design measures the growth of the index from one segment earnings period to the next segment earnings period. The starting point is reset either annually or bi-annually, depending on the strategy. Earnings, if any, are credited and locked in on an annual or bi-annual basis. Point-To-Point Example Using the Five-Year Equity Indexed Strategy E S&P 500 B F 8Index Value A C Years In this example, the total increase over five years would be figured by taking the sum of all anniversaries which experienced an index increase. Notice that the increases occur on the 1st, 3rd and 4th contract anniversaries (B, D and E). The two years that experienced an index decrease result in no gain and no decrease (C and F) in earnings. D

11 POINT-TO-POINT VS. AVERAGING ANNUAL RESET Understanding participation rates, caps and the index measuring methodology used to determine the credited rate is key when comparing EIL products. The accompanying examples show how two Point-to-Point products and one Averaging Annual Reset product compare in various index growth scenarios. It illustrates that products with lower participation rates and averaging methods will generally need substantially greater index growth to achieve a credited rate equal to a product using a high participation rate and a cap. Index Growth SCENARIO 1 SCENARIO 2 Start of Year Index Value $1, $1, End of Year Index Value $1, $1, Index Monthly Average $1,053.38* $1,105.32* Point-to-Point Index Growth 10.0% 20.0% Averaging Annual Reset Index Growth 5.3%* 10.5%* * Monthly index growth used to produce the credited interest rate for the Averaging Annual Reset product. SCENARIO 1 SCENARIO 2 Starting Starting Point $1, Point $1, Month 1 1, Month , , , , , , , , , , , Average $1, Average $1, Average Average Growth 5.3% Growth 10.5% Scenarios are illustrative only and are not intended to be a predictor of actual results. Participation rates and caps are assumed to be constant for the term shown. 9

12 The key advantage of an equity-linked product is that it provides minimum guarantees to protect against downside risk with the upside growth potential of an equity index. AmerUs Life's EILs guarantee that upon contract termination, all amounts paid (less any withdrawals or deductions), will have earned the minimum interest rate specified in the contract. GUARANTEES AMONG STRATEGIES AmerUs Life's EILs feature five interest crediting strategies. Each strategy, and each segment within that strategy, works independently from other strategies and segments. Basic Interest Strategy - The credited interest rate for this strategy may change periodically with market conditions. This rate will never be less than the minimum stated in the contract. One-Year Fixed-Term Strategy - The credited interest rate for a segment within this strategy is set when the segment is created. This rate will never be less than the minimum stated in the contract. Five-Year Fixed-Term Strategy - The credited interest rate for a segment within this strategy is set when the segment is created. This rate will never be less than the minimum stated in the contract. Five-Year Equity Indexed Strategy - Credited interest earnings for this strategy are linked to the performance of the S&P 500 Index. This means if the S&P 500 Index is flat or declines when measured at the segment anniversary, 0% will be credited to the segment for that year. However, at the end of an Equity Indexed Strategy segment's five-year term (or when the contract terminates if earlier), AmerUs Life will credit any additional interest needed to increase the value of the segment at that time to at least the premium (less any withdrawals or deductions) compounded annually at the minimum interest rate guaranteed in the contract. Six-Year Equity Indexed Strategy - Credited interest earnings for this strategy are linked to the performance of the S&P 500 Index. This means if the S&P 500 Index is flat or declines when measured at the end of the two-year segment earnings period, 0% will be credited to the segment. However, at the end of a segment's six-year term (or when the contract terminates if earlier), AmerUs Life will credit any additional interest needed to increase the value of the segment at that time to at least the premium (less any withdrawals or deductions) compounded annually at the minimum interest rate guaranteed in the contract. Ups and Downs of Linking Current Interest to an Equity Index Potential for lower interest earnings (but not less than guaranteed minimum) if Index decreases Potential for higher interest earnings if Index increases 10

13 One significant advantage of an EIL is the potential to earn more than typical fixed rate life insurance and provide downside protection not found in most variable universal life insurance. VOLATILE INCREASING MARKET CONDITIONS If the S&P 500 Index Does This... 20% 10% The Results* Would Be This... UL** EIL VUL (Using Five-Year EI Strategy) Year 1 6% 10% 10% Index Value 15% 10% -20% Years Year 2 6% 12% 20% Year 3 6% 0% -20% Year 4 6% 12% 15% Year 5 6% 10% 10% Effective Annualized 6% 8.4% 6% Interest Earnings Rate VOLATILE DECREASING MARKET CONDITIONS If the S&P 500 Index Does This... Index Value 2% -10% 1% -6% -3% Years The Results* Would Be This... UL** EIL VUL (Using Five-Year EI Strategy) Year 1 6% 2% 2% Year 2 6% 0% -10% Year 3 6% 1% 1% Year 4 6% 0% -6% Year 5 6% 0% -3% End of Term - 7.2%*** - Adjustment Effective Annualized 6% 2% -3.3% Interest Earnings Rate These hypothetical examples show the potential for increased interest earnings on premium directed to the Five-Year Equity Indexed Strategy with an EIL, but there is also the risk that the rate equivalent to traditional fixed life insurance and variable universal life insurance will not be earned. The real security of an EIL is in the protection from the downside stock market risk. * Expense charges and cost of insurance charges not reflected. Assumes a 2% minimum interest rate and a cap of 12% on equity indexed life that do not change during the five-year period. Assumes no dividends, management expenses or fund fees on variable universal life. ** Assumes 6% credited rate for each contract year. *** At the end of a segment's five-year term, AmerUs Life credits any additional interest needed to increase the value of the segment to the minimum interest rate guaranteed in the contract, which in this example is 2%. There is no negative crediting with an index decrease. Scenarios are illustrative only and are not intended to be a predictor of actual results. 11

14 HOW THE ILLUSTRATED RATE IS DETERMINED FOR AN EIL ILLUSTRATION The total amount of interest credited to a Vision Builder or Liberty Builder policy is the sum of the interest earnings credited to each strategy. In order to represent the combined credited interest earnings in an illustration, a weighted average assumed rate is used. This weighted average assumed rate is derived by averaging the current interest rates of the Basic Interest Strategy, the One-Year Fixed-Term Strategy, and Five-Year Fixed-Term Strategy, along with a reasonable expectation of index growth for the Five-Year and Six-Year Equity Indexed Strategies. The Basic Interest Strategy is always included in an illustration, but it is optional whether some or all of the other four strategies - the One-Year Fixed-Term Strategy, Five-Year Fixed-Term Strategy, Five-Year Equity Indexed Strategy and the Six-Year Equity Indexed Strategy - are chosen to illustrate cash value accumulation inside the policy. The weighted average assumed rate is illustrated as the assumed rate in the Non-Guaranteed Assumed Values section of the policy illustration. The interest crediting rate used for each strategy is found on the second page of the illustration. Interest Rates Basic Interest, One-Year Fixed- Term and Five-Year Fixed-Term Strategies The interest rates illustrated for the Basic Interest Strategy, the One-Year Fixed-Term Strategy and the Five-Year Fixed- Term Strategy are those currently being credited by the Company. These rates may change from time to time as declared by the Company. At no time will they be less than the interest rate guaranteed in the policy. Current interest rates are available on AmerUs Live. Equity Indexed Strategy Illustrated Rate AmerUs Life provides a "guideline" rate to be used in illustrating cash value growth associated with the two Equity Indexed Strategies. This guideline rate is dependent on the cap rate and is derived from applying the cap rate to historical movements in the S&P 500 Index, excluding dividends, based on the policy mechanics. Currently illustrated rates for a declared cap rate are representative of the monthly S&P 500 Index and dividend yield* data since January The Company will update the guideline illustrated rate when: 1) the cap rate changes, and/or 2) emerging S&P 500 Index experience warrants a change. Because the Company is basing the illustrated rate on such a long-term perspective, changes to the guideline rate due to emerging experience are expected to be relatively infrequent (e.g. every two or three years). Remember, the purpose of a policy illustration is to provide a reasonable view of the long-term, potential values in the policy based on its current, non-guaranteed elements as well as minimum guarantees. The illustrated rate is for illustration purposes ONLY. The actual credited rate can be higher or lower, and will be based on the actual S&P 500 Index movement, which cannot be predicted. Unlike the level rate illustrated for each strategy, the actual index-linked illustrated rates are likely to vary over time. The Five-Year Equity Indexed Strategy uses an assumed rate that is credited each year while the Six-Year Equity Indexed Strategy uses an assumed rate that is credited every two years. At the end of each five- or six-year segment within the Equity Indexed Strategies, AmerUs Life guarantees the segment value will be at least equal to the premium paid (less any withdrawals or deductions) compounded annually at the minimum guaranteed interest rate of 2%. HOW THE CONTRACT IS SUPPORTED Vision Builder and Liberty Builder are like any other fixed interest rate universal life contracts in that they are backed by AmerUs Life's general account and no separate account is established. AmerUs Life does not directly invest in the stock market to support the product. As it does with other general account products, AmerUs Life chooses investments that closely mimic its liabilities. With an equity indexed product like Vision Builder or Liberty Builder, this means that AmerUs Life purchases assets to cover both the minimum guarantees of the contract as well as the upside potential brought about by the equity index features. For example, bonds, mortgages, or other fixed income assets may be purchased to support the minimum guarantees, while options or other equity based securities may be purchased to support the upside potential. Cap rates are, in general, based on the costs of these investments. * While the index excludes dividends, actual dividend yields do impact the cost of the investments supporting the product, which helps determine the cap rate. Subject to contract restrictions 12

15 THE UNIQUE APPEAL OF EILS Equity Indexed Life products combine the features of traditional fixed life products with the potential to earn interest based on the upward movement of an equity index. With this unique combination of benefits, EILs have become popular among financial consumers. While equity indexed products credit interest earnings based on the upward movement of an equity index, EILs are not securities. Purchasing an EIL is not the same as making an investment directly in the stock market. EILs are fixed life products that offer a viable alternative to variable universal life. AmerUs Life thanks you for taking the time to learn about EILs, so you can determine whether an equity-linked product is right for you.

16 AmerUs Life Insurance Company 611 Fifth Avenue Des Moines, Iowa, /04

UNDERSTANDING INDEXED LIFE INSURANCE

UNDERSTANDING INDEXED LIFE INSURANCE STABILITY WITH UPSIDE POTENTIAL A life insurance purchase is one of the most important investments an individual can make. It can assure that a family s lifestyle will

UNDERSTANDING INDEXED LIFE INSURANCE STABILITY WITH UPSIDE POTENTIAL A life insurance purchase is one of the most important investments an individual can make. It can assure that a family s lifestyle will

Advantage Builder II ABOUT AVIVA. Consumer product guide

ABOUT AVIVA Aviva Life and Annuity Company is part of Aviva USA, one of the fastest-growing life insurers in the United States, with more than 1,115,000 customers and 32,850 agents and distributors. We

ABOUT AVIVA Aviva Life and Annuity Company is part of Aviva USA, one of the fastest-growing life insurers in the United States, with more than 1,115,000 customers and 32,850 agents and distributors. We

Income Preferred Bonus Fixed Indexed Annuity

Income Preferred Bonus Fixed Indexed Annuity 55542 (03/14) What is a fixed indexed annuity? It is a contract between you and an insurance company. In return for your money, or premium, the insurance company

Income Preferred Bonus Fixed Indexed Annuity 55542 (03/14) What is a fixed indexed annuity? It is a contract between you and an insurance company. In return for your money, or premium, the insurance company

Understanding Indexed Universal Life Insurance

Understanding Indexed Universal Life Insurance Consumer Guide Table of Contents Overview [ 2 ] Indexed Universal Life Insurance [ 2 ] What is Indexed Universal Life Insurance? [ 2 ] How North American

Understanding Indexed Universal Life Insurance Consumer Guide Table of Contents Overview [ 2 ] Indexed Universal Life Insurance [ 2 ] What is Indexed Universal Life Insurance? [ 2 ] How North American

Accumulation Builder II SM IUL. Protecting your family, building your future. A better way of life

Accumulation Builder II SM IUL Protecting your family, building your future. A better way of life When you need protection for your family and a foundation for your future. Protection for Today A permanent

Accumulation Builder II SM IUL Protecting your family, building your future. A better way of life When you need protection for your family and a foundation for your future. Protection for Today A permanent

Diversified Growth SM Variable Universal Life. Protection and accumulation that adjust with your life. A better way of life

Diversified Growth SM Variable Universal Life Protection and accumulation that adjust with your life A better way of life Add to your peace of mind, while adding to your assets You want and need to protect

Diversified Growth SM Variable Universal Life Protection and accumulation that adjust with your life A better way of life Add to your peace of mind, while adding to your assets You want and need to protect

Aviva s No-Lapse Guarantee Portfolio

We are building insurance around you. Aviva s No-Lapse Guarantee Portfolio Advantage Builder Guarantee UL Solution Agent reference guide 17928 For agent use only. Not for use with the general public 5/11

We are building insurance around you. Aviva s No-Lapse Guarantee Portfolio Advantage Builder Guarantee UL Solution Agent reference guide 17928 For agent use only. Not for use with the general public 5/11

UNDERSTANDING FIXED INDEXED ANNUITIES

UNDERSTANDING FIXED INDEXED ANNUITIES INTRODUCING FIXED INDEXED ANNUITIES Fixed Indexed Annuities combine the features of Fixed Annuities including tax-deferred interest accumulation, a minimum guaranteed

UNDERSTANDING FIXED INDEXED ANNUITIES INTRODUCING FIXED INDEXED ANNUITIES Fixed Indexed Annuities combine the features of Fixed Annuities including tax-deferred interest accumulation, a minimum guaranteed

Discover What s Possible

Discover What s Possible Accumulation Builder Choice SM IUL for Business Accumulation Builder Choice SM Indexed Universal Life for Business Owners Building your path to success As a small business owner,

Discover What s Possible Accumulation Builder Choice SM IUL for Business Accumulation Builder Choice SM Indexed Universal Life for Business Owners Building your path to success As a small business owner,

Series. Eagle Select. Fixed Indexed Annuity (ICC13 E-IDXA)* Issued by:

* Issued by:") Fixed Indexed Annuity Eagle Select Series (ICC13 E-IDXA)* Issued by: * Form number and availability may vary by state. Annuity contracts are products of the insurance industry and are not guaranteed by

Fixed Indexed Annuity Eagle Select Series (ICC13 E-IDXA)* Issued by: * Form number and availability may vary by state. Annuity contracts are products of the insurance industry and are not guaranteed by

Indexed Survivor Universal Life

Indexed Survivor Universal Life Protecting your estate... 15888 7/10 Indexed Survivor Universal Life Building wealth has always been about more than living the good life. The estate you ve amassed through

Indexed Survivor Universal Life Protecting your estate... 15888 7/10 Indexed Survivor Universal Life Building wealth has always been about more than living the good life. The estate you ve amassed through

Understanding Fixed Indexed Annuities

Fact Sheet for Consumers: Understanding Fixed Indexed Annuities PRESENTED BY Insured Retirement Institute Fact Sheet for Consumers: Understanding Fixed Indexed Annuities Put simply, a Fixed Indexed Annuity

Fact Sheet for Consumers: Understanding Fixed Indexed Annuities PRESENTED BY Insured Retirement Institute Fact Sheet for Consumers: Understanding Fixed Indexed Annuities Put simply, a Fixed Indexed Annuity

AIUL2013 (04-15) Understanding. Indexed Universal Life

Understanding. Indexed Universal Life") AIUL2013 (04-15) Understanding Indexed Universal Life About Accordia Life Accordia Life is an innovative life insurance company, providing customers and agents proven expertise in indexed universal life

AIUL2013 (04-15) Understanding Indexed Universal Life About Accordia Life Accordia Life is an innovative life insurance company, providing customers and agents proven expertise in indexed universal life

Understanding Indexed Universal Life Insurance

Understanding Indexed Universal Life Insurance Consumer Guide Table of Contents Overview [ 2 ] Indexed Universal Life Insurance [ 2 ] What is Indexed Universal Life Insurance? [ 2 ] How North American

Understanding Indexed Universal Life Insurance Consumer Guide Table of Contents Overview [ 2 ] Indexed Universal Life Insurance [ 2 ] What is Indexed Universal Life Insurance? [ 2 ] How North American

Your Guide to ING Indexed Universal Life CV

Early retirement. Financial security. Expanding your business. Oh, the possibilities. Your Guide to ING Indexed Universal Life CV Issued by Security Life of Denver Insurance Company LIFE Your future. Made

Early retirement. Financial security. Expanding your business. Oh, the possibilities. Your Guide to ING Indexed Universal Life CV Issued by Security Life of Denver Insurance Company LIFE Your future. Made

Value+ Protector Index Universal Life Insurance

Value+ Protector Index Universal Life Insurance Long-term financial protection and value at a market-leading price PROTECTION VALUE STABILITY ACCESS Help provide security for beneficiaries Receive extended

Value+ Protector Index Universal Life Insurance Long-term financial protection and value at a market-leading price PROTECTION VALUE STABILITY ACCESS Help provide security for beneficiaries Receive extended

Understanding and Benefiting from FIXED INDEXED ANNUITIES

Understanding and Benefiting from FIXED INDEXED ANNUITIES 1 What do FIXED INDEXED ANNUITIES offer? Safety of principal and previously-credited interest No risk of loss if held to term Minimum contract

Understanding and Benefiting from FIXED INDEXED ANNUITIES 1 What do FIXED INDEXED ANNUITIES offer? Safety of principal and previously-credited interest No risk of loss if held to term Minimum contract

Aviva MultiChoice SM Xtra S

We are building insurance around you. Aviva MultiChoice SM Xtra S Fixed Indexed Annuity 81143 (Rev. 12/12) What is a fixed indexed annuity? It is a contract between you and an insurance company. In return

We are building insurance around you. Aviva MultiChoice SM Xtra S Fixed Indexed Annuity 81143 (Rev. 12/12) What is a fixed indexed annuity? It is a contract between you and an insurance company. In return

Understanding Indexed Universal Life Insurance

Understanding Indexed Universal Life Insurance Consumer Brochure Table of Contents Overview... [ 2 ] Indexed Universal Life Insurance...[ 2 ] What is Indexed Universal Life Insurance?... [ 2 ] How North

Understanding Indexed Universal Life Insurance Consumer Brochure Table of Contents Overview... [ 2 ] Indexed Universal Life Insurance...[ 2 ] What is Indexed Universal Life Insurance?... [ 2 ] How North

flexible life insurance protection enhanced cash value accumulation potential

AXA Equitable Life Insurance Company Athena Indexed Universal Life SM flexible life insurance protection enhanced cash value accumulation potential your changing protection and financial needs Life never

AXA Equitable Life Insurance Company Athena Indexed Universal Life SM flexible life insurance protection enhanced cash value accumulation potential your changing protection and financial needs Life never

NORTH AMERICAN FORMULA CHOICE FIXED INDEX ANNUITY 11079Z-06 REV 08-10

NORTH AMERICAN FORMULA CHOICE FIXED INDEX ANNUITY 11079Z-06 REV 08-10 NORTH AMERICAN FORMULA CHOICE The Formula Choice is a flexible premium, fixed index annuity that offers you the ability to apply all

NORTH AMERICAN FORMULA CHOICE FIXED INDEX ANNUITY 11079Z-06 REV 08-10 NORTH AMERICAN FORMULA CHOICE The Formula Choice is a flexible premium, fixed index annuity that offers you the ability to apply all

Advantage Builder III Indexed Universal Life

Advantage Builder III Indexed Universal Life A policy just for you 17537 7/10 A policy just for You At Aviva, we understand your life evolves every day that s how life is. And as you and your unique needs

Advantage Builder III Indexed Universal Life A policy just for you 17537 7/10 A policy just for You At Aviva, we understand your life evolves every day that s how life is. And as you and your unique needs

Flexible Premium Universal Life Insurance with an Indexed Feature A Life Insurance Illustration

Initial Base Face Amount = $ Total Initial Annual Premium = $ About the Universal Life Insurance Policy Phoenix Simplicity Index Life is a single life flexible premium universal life insurance policy with

Initial Base Face Amount = $ Total Initial Annual Premium = $ About the Universal Life Insurance Policy Phoenix Simplicity Index Life is a single life flexible premium universal life insurance policy with

A Powerful Combination for Retirement

Power Select Plus Income Index Annuity A Powerful Combination for Retirement Principal Protection. Growth Potential. Lifetime Income. Plus, the Opportunity to Guarantee Rising Income for Up to 10 Contract

Power Select Plus Income Index Annuity A Powerful Combination for Retirement Principal Protection. Growth Potential. Lifetime Income. Plus, the Opportunity to Guarantee Rising Income for Up to 10 Contract

MEMBERS Index Annuity

MEMBERS Index Annuity GUARANTEES, WITH FLEXIBILITY AND UPSIDE POTENTIAL Move confidently into the future 07-0002 REV 09MHC A financial services company serving financial institutions and their clients

MEMBERS Index Annuity GUARANTEES, WITH FLEXIBILITY AND UPSIDE POTENTIAL Move confidently into the future 07-0002 REV 09MHC A financial services company serving financial institutions and their clients

14-YEAR SURRENDER PERIOD Issue Ages 0-65 1

NORTH AMERICAN Charter SM 14 Fixed INDEX ANNUITY 16761Z-04 PRT 08-12 [Any annotations are personal comments for research, informational and education purposes ONLY. Sales Proposals ONLY allow the addition

NORTH AMERICAN Charter SM 14 Fixed INDEX ANNUITY 16761Z-04 PRT 08-12 [Any annotations are personal comments for research, informational and education purposes ONLY. Sales Proposals ONLY allow the addition

NAC RetireChoice SM 10 FIXED INDEX ANNUITY 16107Z REV 07-12

NAC RetireChoice SM 10 FIXED INDEX ANNUITY 16107Z REV 07-12 FLEXIBLE CHOICES THAT FIT Most people dream about having a secure and comfortable retirement. And now because we re living longer, healthier

NAC RetireChoice SM 10 FIXED INDEX ANNUITY 16107Z REV 07-12 FLEXIBLE CHOICES THAT FIT Most people dream about having a secure and comfortable retirement. And now because we re living longer, healthier

Income-Tax Free Benefits for Your Heirs and Lifetime Benefits for You. Lifetime Benefits for You

Indexed Universal Life Insurance 1 Income-Tax Free s for Your Heirs and Lifetime s for You Prepared on August 13, 2013 for by Trusted Advisor Income - 1 Tax Free s for Your Heirs Lifetime s for You Product

Indexed Universal Life Insurance 1 Income-Tax Free s for Your Heirs and Lifetime s for You Prepared on August 13, 2013 for by Trusted Advisor Income - 1 Tax Free s for Your Heirs Lifetime s for You Product

for a secure Retirement Bonus Gold (INDEX-1-07)* *Form number varies by state.

* *Form number varies by state.") for a secure Retirement Bonus Gold (INDEX-1-07)* *Form number varies by state. Where Will Your Retirement Dollars Take You? RETIREMENT PROTECTION ASSURING YOUR LIFESTYLE As Americans, we work hard everyday

for a secure Retirement Bonus Gold (INDEX-1-07)* *Form number varies by state. Where Will Your Retirement Dollars Take You? RETIREMENT PROTECTION ASSURING YOUR LIFESTYLE As Americans, we work hard everyday

How Does Survivorship GIUL Work?

A Protection Plan for Future Generations Information on North American Company s Survivorship GIUL Indexed Universal Life Insurance Product Consumer Brochure NAM-1436 11/12 Table of Contents Overview [

A Protection Plan for Future Generations Information on North American Company s Survivorship GIUL Indexed Universal Life Insurance Product Consumer Brochure NAM-1436 11/12 Table of Contents Overview [

How To Get A Balanced Allocation Annuity

BalancedAllocation LIFETIME INCOME RIDER THE INCOME RIDER AS UNIQUE AS YOU. Why stop when it comes to planning your retirement income? A retirement plan isn t just about that moment when you retire, but

BalancedAllocation LIFETIME INCOME RIDER THE INCOME RIDER AS UNIQUE AS YOU. Why stop when it comes to planning your retirement income? A retirement plan isn t just about that moment when you retire, but

A balanced, versatile approach to long-term wealth accumulation

RiverSource Multi-Index universal life insurance RiverSource Life Insurance Company RiverSource Life Insurance Co. of New York A balanced, versatile approach to long-term wealth accumulation 291731 D (3/16)

RiverSource Multi-Index universal life insurance RiverSource Life Insurance Company RiverSource Life Insurance Co. of New York A balanced, versatile approach to long-term wealth accumulation 291731 D (3/16)

Aim for the Horizon. Security. Growth. Flexibility. Strength. CONSUMER Guide

CONSUMER Guide AG HorizonIndex 9 Annuity AG HorizonIndex 12 Annuity index single-premium deferred annuity with premium bonus, market value adjustment and AG Lifetime Income Builder optional living benefit

CONSUMER Guide AG HorizonIndex 9 Annuity AG HorizonIndex 12 Annuity index single-premium deferred annuity with premium bonus, market value adjustment and AG Lifetime Income Builder optional living benefit

North American Pillar 13930Z REV 08-12

North American Pillar fixed index annuity 13930Z REV 08-12 North American Pillar Are you looking for ways to manage your future retirement income today so that you can enjoy financial freedom later? North

North American Pillar fixed index annuity 13930Z REV 08-12 North American Pillar Are you looking for ways to manage your future retirement income today so that you can enjoy financial freedom later? North

PROTECTION PROTECTION SIUL. The pacesetter in affordable, secure protection. For two. CONSUMER GUIDE IM4156CG

CONSUMER GUIDE PROTECTION PROTECTION SIUL The pacesetter in affordable, secure protection. For two. IM4156CG JOHN HANCOCK LIFE INSURANCE COMPANY (U.S.A.) JOHN HANCOCK LIFE INSURANCE COMPANY OF NEW YORK

CONSUMER GUIDE PROTECTION PROTECTION SIUL The pacesetter in affordable, secure protection. For two. IM4156CG JOHN HANCOCK LIFE INSURANCE COMPANY (U.S.A.) JOHN HANCOCK LIFE INSURANCE COMPANY OF NEW YORK

PruLife Index Advantage UL

CREATED EXCLUSIVELY FOR FINANCIAL PROFESSIONALS FAQS PruLife Index Advantage UL A new product usually gives rise to questions, and PruLife Index Advantage UL (Advantage UL) is no exception. Here are some

CREATED EXCLUSIVELY FOR FINANCIAL PROFESSIONALS FAQS PruLife Index Advantage UL A new product usually gives rise to questions, and PruLife Index Advantage UL (Advantage UL) is no exception. Here are some

Fixed Index Annuities

Fixed Index Annuities I Annuities Sales Tool Series Fixed Index Annuities Innovative Retirement Planning Alternative 143731 11/26/12 For Producer/Agent Information Only. Not to be Reproduced or Shown to

Fixed Index Annuities I Annuities Sales Tool Series Fixed Index Annuities Innovative Retirement Planning Alternative 143731 11/26/12 For Producer/Agent Information Only. Not to be Reproduced or Shown to

A Review of Indexed Universal Life Considerations

Life insurance due care requires an understanding of the factors that impact policy performance and drive product selection. D U E C A R E B U L L E T I N A Review of Indexed Universal Life Considerations

Life insurance due care requires an understanding of the factors that impact policy performance and drive product selection. D U E C A R E B U L L E T I N A Review of Indexed Universal Life Considerations

Pacific Life Insurance Company Indexed Universal Life Insurance: Frequently Asked Questions

Pacific Life Insurance Company Indexed Universal Life Insurance: Frequently Asked Questions THE GROWTH CAP, PARTICIPATION RATE, AND FLOOR RATEE 1. What accounts for the gap in indexed cap rates from one

Pacific Life Insurance Company Indexed Universal Life Insurance: Frequently Asked Questions THE GROWTH CAP, PARTICIPATION RATE, AND FLOOR RATEE 1. What accounts for the gap in indexed cap rates from one

BUYER'S GUIDE TO EQUITY-INDEXED ANNUITIES WHAT ARE THE DIFFERENT KINDS OF ANNUITY CONTRACTS?

BUYER'S GUIDE TO EQUITY-INDEXED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

BUYER'S GUIDE TO EQUITY-INDEXED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

for a secure Retirement Retirement Gold (INDEX-2-09)* *Form number varies by state.

* *Form number varies by state.") for a secure Retirement Retirement Gold (INDEX-2-09)* *Form number varies by state. Where Will Your Retirement Dollars Take You? RETIREMENT PROTECTION ASSURING YOUR LIFESTYLE As Americans, we work hard

for a secure Retirement Retirement Gold (INDEX-2-09)* *Form number varies by state. Where Will Your Retirement Dollars Take You? RETIREMENT PROTECTION ASSURING YOUR LIFESTYLE As Americans, we work hard

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES. The face page of the Fixed Deferred Annuity Buyer s Guide shall read as follows:

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES The face page of the Fixed Deferred Annuity Buyer s Guide shall read as follows: Prepared by the National Association of Insurance Commissioners The National Association

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES The face page of the Fixed Deferred Annuity Buyer s Guide shall read as follows: Prepared by the National Association of Insurance Commissioners The National Association

Nationwide YourLife Indexed UL. Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC

advisor GUIDE Nationwide YourLife Indexed UL Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC Preparing for the future can be stressful for your clients.

advisor GUIDE Nationwide YourLife Indexed UL Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC Preparing for the future can be stressful for your clients.

SecurePlus Provider I N D E X E D U N I V E R S A L L I F E

SecurePlus Provider I N D E X E D U N I V E R S A L L I F E B U Y E R S G U I D E TC27761(0906) Life is a journey. And while there are many unknowns along the way, you can be prepared. Preparations should

SecurePlus Provider I N D E X E D U N I V E R S A L L I F E B U Y E R S G U I D E TC27761(0906) Life is a journey. And while there are many unknowns along the way, you can be prepared. Preparations should

CLIENT BROCHURE Nationwide YourLife Indexed UL. Find balance in life

CLIENT BROCHURE Nationwide YourLife Indexed UL Find balance in life Planning for the future may seem stressful these days especially with so much market uncertainty. But it doesn t have to be that way.

CLIENT BROCHURE Nationwide YourLife Indexed UL Find balance in life Planning for the future may seem stressful these days especially with so much market uncertainty. But it doesn t have to be that way.

The Truth About Fixed Indexed Annuities

The Truth About Fixed Indexed Annuities Index annuities were first introduced in the United States nearly two decades ago. They were initially created as an alternative to mutual funds and variable annuities,

The Truth About Fixed Indexed Annuities Index annuities were first introduced in the United States nearly two decades ago. They were initially created as an alternative to mutual funds and variable annuities,

The Hartford Saver Solution Choice SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT

The Hartford Saver Solution Choice SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION CHOICE SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important

The Hartford Saver Solution Choice SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION CHOICE SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important

ConsecoLifeOptions SM

Upside potential with downside protection. ConsecoLifeOptions SM indexed universal life insurance Freedom Choices Flexibility Conseco Insurance Company A life and health insurance company CL-LO-CB ConsecoLifeOptions

Upside potential with downside protection. ConsecoLifeOptions SM indexed universal life insurance Freedom Choices Flexibility Conseco Insurance Company A life and health insurance company CL-LO-CB ConsecoLifeOptions

The Lafayette Life Insurance Company Agents Products Quiz The Marquis Series of Products and Other Annuities

There are different types of annuity products that can serve different needs. Even within a particular type of annuity product category, for example a fixed indexed annuity, the benefits and features can

There are different types of annuity products that can serve different needs. Even within a particular type of annuity product category, for example a fixed indexed annuity, the benefits and features can

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important information

The Hartford Saver Solution SM A FIXED INDEX ANNUITY DISCLOSURE STATEMENT THE HARTFORD SAVER SOLUTION SM FIXED INDEX ANNUITY DISCLOSURE STATEMENT This Disclosure Statement provides important information

Cost-effective index universal life insurance with upside potential and downside protection

Elite Index II Producer Guide Cost-effective index universal life insurance with upside potential and downside protection Policies issued by American General Life Insurance Company (AGL) Security and choice

Elite Index II Producer Guide Cost-effective index universal life insurance with upside potential and downside protection Policies issued by American General Life Insurance Company (AGL) Security and choice

Fixed Deferred Annuities

Buyer s Guide to: Fixed Deferred Annuities with Appendix for Equity-Indexed Annuities National Association of Insurance Commissioners 2301 McGee St Suite 800 Kansas City, MO 64108-2604 (816) 842-3600 1999,

Buyer s Guide to: Fixed Deferred Annuities with Appendix for Equity-Indexed Annuities National Association of Insurance Commissioners 2301 McGee St Suite 800 Kansas City, MO 64108-2604 (816) 842-3600 1999,

Indexed Universal Life Insurance

Insurance Upside Potential with Downside Protection Securities and Investment Advisory Services offered through M Holdings Securities, Inc., a registered broker dealer and Investment Advisor, member FINRA

Insurance Upside Potential with Downside Protection Securities and Investment Advisory Services offered through M Holdings Securities, Inc., a registered broker dealer and Investment Advisor, member FINRA

Annuities. Products. Safe Money. that Stimulate Financial Growth & Preserve Wealth. Safe Money is for money you cannot afford to lose.

Annuities Safe Money Products that Stimulate Financial Growth & Preserve Wealth Safe Money is for money you cannot afford to lose. Learn why Annuities are considered to be a Safe Money Place and how these

Annuities Safe Money Products that Stimulate Financial Growth & Preserve Wealth Safe Money is for money you cannot afford to lose. Learn why Annuities are considered to be a Safe Money Place and how these

Understanding Fixed Indexed Annuities

Understanding Fixed Indexed Annuities Legacy Producer Training Presentation FOR BROKER USE ONLY. NOT FOR USE WITH CONSUMERS. 1 This training presentation is designed to ensure your understanding of the:

Understanding Fixed Indexed Annuities Legacy Producer Training Presentation FOR BROKER USE ONLY. NOT FOR USE WITH CONSUMERS. 1 This training presentation is designed to ensure your understanding of the:

North America Company s Indexed Universal Life Portfolio

North America Company s Indexed Universal Life Portfolio North American Company s Builder IUL Series plans are indexed universal life insurance products that offer the guarantees and flexibility of universal

North America Company s Indexed Universal Life Portfolio North American Company s Builder IUL Series plans are indexed universal life insurance products that offer the guarantees and flexibility of universal

Understanding Annuities: A Lesson in Indexed Annuities

Understanding Annuities: A Lesson in Indexed Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that

Understanding Annuities: A Lesson in Indexed Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that

Indexed Universal Life Insurance Upside Potential with Downside Protection

Insurance Upside Potential with Downside Protection Securities and Investment Advisory Services offered through M Holdings Securities, Inc., a registered broker dealer and Investment Advisor, member FINRA

Insurance Upside Potential with Downside Protection Securities and Investment Advisory Services offered through M Holdings Securities, Inc., a registered broker dealer and Investment Advisor, member FINRA

Protection That Offers Selection To Fit Your Lifestyle! More Choices More Control!

Protection That Offers Selection To Fit Your Lifestyle! More Choices More Control! Consumer Brochure A Flexible Premium Life Insurance Policy with Equity Index Options Policy Form 01-1143-07 and state

Protection That Offers Selection To Fit Your Lifestyle! More Choices More Control! Consumer Brochure A Flexible Premium Life Insurance Policy with Equity Index Options Policy Form 01-1143-07 and state

Index Growth Annuities

Index Growth Annuities 5 And 7 A Rewarding Combination Of Safety, Tax Deferral And Choice Standard Insurance Company Index Growth Annuities A Deferred Annuity Is An Insurance Contract A deferred annuity

Index Growth Annuities 5 And 7 A Rewarding Combination Of Safety, Tax Deferral And Choice Standard Insurance Company Index Growth Annuities A Deferred Annuity Is An Insurance Contract A deferred annuity

ANNUITY DISCLOSURE MODEL REGULATION. Standards for the Disclosure Document and Buyer s Guide Report to Contract Owners *****

Draft: 7/15/08 Revisions to Appendix A in Model 245 Edits by K Kitt and B. Cude 9/16/09 Comments should be sent by email to Jennifer Cook at jcook@naic.org by October 23, 2009. Table of Contents ANNUITY

Draft: 7/15/08 Revisions to Appendix A in Model 245 Edits by K Kitt and B. Cude 9/16/09 Comments should be sent by email to Jennifer Cook at jcook@naic.org by October 23, 2009. Table of Contents ANNUITY

Survivorship Builder. An indexed survivorship life policy AS2000 (04-15)

") Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Survivorship index universal life insurance

Elite Survivor Index II Producer Guide Survivorship index universal life insurance Policies issued by American General Life Insurance Company (AGL) and The United States Life Insurance Company in the City

Elite Survivor Index II Producer Guide Survivorship index universal life insurance Policies issued by American General Life Insurance Company (AGL) and The United States Life Insurance Company in the City

Overview of Your TIAA-CREF Investment Solutions SM Accounts

Overview of Your TIAA-CREF Investment Solutions SM Accounts TIAA-CREF Investment Solutions SM now offers you nine mutual funds in addition to our fixed and variable annuity accounts. TIAA-CREF Investment

Overview of Your TIAA-CREF Investment Solutions SM Accounts TIAA-CREF Investment Solutions SM now offers you nine mutual funds in addition to our fixed and variable annuity accounts. TIAA-CREF Investment

Issued by Fidelity & Guaranty Life Insurance Company, Baltimore, MD Distributed by Legacy Marketing Group

Issued by Fidelity & Guaranty Life Insurance Company, Baltimore, MD Distributed by Legacy Marketing Group Choices To Plan for the Long Term The financial challenges you face evolve with economic and life

Issued by Fidelity & Guaranty Life Insurance Company, Baltimore, MD Distributed by Legacy Marketing Group Choices To Plan for the Long Term The financial challenges you face evolve with economic and life

Heritage Gold. American Equity. Gold Standard for a Secure Retirement. The one who works for you!

Heritage Gold American Equity Gold Standard for a Secure Retirement The one who works for you! Heritage Gold A Good Plan is Always Better Than a Good Guess The security of your future begins today with

Heritage Gold American Equity Gold Standard for a Secure Retirement The one who works for you! Heritage Gold A Good Plan is Always Better Than a Good Guess The security of your future begins today with

LiveWell Fixed Index Annuity

LiveWell Fixed Index Annuity Issued by Midland National Life Insurance Company Administered by 19231I PRT 03-14 1 May Provide Guaranteed Income for Life. Retain Control of Your Money. Potential for Stock

LiveWell Fixed Index Annuity Issued by Midland National Life Insurance Company Administered by 19231I PRT 03-14 1 May Provide Guaranteed Income for Life. Retain Control of Your Money. Potential for Stock

An Assessment of No Lapse Guarantee Products and Alternatives. Prepared and Researched by

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

The Basics of Annuities: Planning for Income Needs

March 2013 The Basics of Annuities: Planning for Income Needs summary the facts of retirement Earning income once your paychecks stop that is, after your retirement requires preparing for what s to come

March 2013 The Basics of Annuities: Planning for Income Needs summary the facts of retirement Earning income once your paychecks stop that is, after your retirement requires preparing for what s to come

THE SECURITY BENEFIT FOUNDATIONS ANNUITY

THE SECURITY BENEFIT FOUNDATIONS ANNUITY The Security Benefit Foundations Annuity Retirement. It s a big step and one you ve spent your whole career saving for and building on. As you enter retirement,

THE SECURITY BENEFIT FOUNDATIONS ANNUITY The Security Benefit Foundations Annuity Retirement. It s a big step and one you ve spent your whole career saving for and building on. As you enter retirement,

advisory & Brokerage consulting services Make Your Retirement Savings Last a Lifetime

advisory & Brokerage consulting services Make Your Retirement Savings Last a Lifetime Member FINRA/SIPC ADVISORY & Brokerage consulting SERVICES Three Things to Consider When Planning for Retirement Today,

advisory & Brokerage consulting services Make Your Retirement Savings Last a Lifetime Member FINRA/SIPC ADVISORY & Brokerage consulting SERVICES Three Things to Consider When Planning for Retirement Today,

Understanding Annuities

Annuities, 06 5/4/05 12:43 PM Page 1 Important Information about Variable Annuities Variable annuities are offered by prospectus, which you can obtain from your financial professional or the insurance

Annuities, 06 5/4/05 12:43 PM Page 1 Important Information about Variable Annuities Variable annuities are offered by prospectus, which you can obtain from your financial professional or the insurance

Retirement Chapters 10 SM

Delaware Life Retirement Chapters 0 SM Fixed Index Annuity The Retirement Challenge Retirement is a time to do the things that you never have a chance to do when you re working, raising a family, and paying

Delaware Life Retirement Chapters 0 SM Fixed Index Annuity The Retirement Challenge Retirement is a time to do the things that you never have a chance to do when you re working, raising a family, and paying

Lifetime Retirement Planning with Wells Fargo Advisors Income guarantees for your retirement savings

Lifetime Retirement Planning with Wells Fargo Advisors Income guarantees for your retirement savings Get there. Your way. Lifetime Retirement Planning with Wells Fargo Advisors 1 Guaranteed income for

Lifetime Retirement Planning with Wells Fargo Advisors Income guarantees for your retirement savings Get there. Your way. Lifetime Retirement Planning with Wells Fargo Advisors 1 Guaranteed income for

Evaluating the Different Types of Life Insurance Coverage

Evaluating the Different Types of Life Insurance Coverage All life insurance falls into one of two categories of coverage. Each category has certain characteristics that make it more suitable for certain

Evaluating the Different Types of Life Insurance Coverage All life insurance falls into one of two categories of coverage. Each category has certain characteristics that make it more suitable for certain

Define your goals. Understand your objectives.

Define your goals. Understand your objectives. As an investor, you are unique. Your financial goals, current financial situation, investment experience and attitude towards risk all help determine the

Define your goals. Understand your objectives. As an investor, you are unique. Your financial goals, current financial situation, investment experience and attitude towards risk all help determine the

The Basics of Annuities: Income Beyond the Paycheck

The Basics of Annuities: PLANNING FOR INCOME NEEDS TABLE OF CONTENTS Income Beyond the Paycheck...1 The Facts of Retirement...2 What Is an Annuity?...2 What Type of Annuity Is Right for Me?...2 Payment

The Basics of Annuities: PLANNING FOR INCOME NEEDS TABLE OF CONTENTS Income Beyond the Paycheck...1 The Facts of Retirement...2 What Is an Annuity?...2 What Type of Annuity Is Right for Me?...2 Payment

Build your retirement plan to last a lifetime.

Build your retirement plan to last a lifetime. Phoenix Personal Income Annuity A single-premium fixed indexed annuity with lifetime income options IRS Circular 230 Disclosure: Any information contained

Build your retirement plan to last a lifetime. Phoenix Personal Income Annuity A single-premium fixed indexed annuity with lifetime income options IRS Circular 230 Disclosure: Any information contained

Understanding fixed index universal life insurance

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation, and tax advantages in one policy M-3959 Page of 6 Understanding fixed

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation, and tax advantages in one policy M-3959 Page of 6 Understanding fixed

Looking For Protection

Financial Advisor Website and Magazine www.fa-mag.com Looking For Protection Financial Advisor Magazine 2011 Issue FA NEWS MARCH Index annuities promise to deliver a guaranteed return, but their costs

Financial Advisor Website and Magazine www.fa-mag.com Looking For Protection Financial Advisor Magazine 2011 Issue FA NEWS MARCH Index annuities promise to deliver a guaranteed return, but their costs

Secure Income Annuity. Base Product. live CONFIDENTLY

Secure Income Annuity Base Product live CONFIDENTLY Welcome! Security Benefit Secure Income Annuity Most of us look forward to retirement. We want to know that when we retire, especially in the volatile

Secure Income Annuity Base Product live CONFIDENTLY Welcome! Security Benefit Secure Income Annuity Most of us look forward to retirement. We want to know that when we retire, especially in the volatile

Hi, my name is [presenter] with Forethought Life Insurance Company.

![Hi, my name is [presenter] with Forethought Life Insurance Company.](/thumbs/22/1299823.jpg "Hi, my name is [presenter] with Forethought Life Insurance Company.") Hi, my name is [presenter] with Forethought Life Insurance Company. Today we ll be talking about some of the myths and truths regarding fixed index annuities. 1 You may have wondered whether an annuity

Hi, my name is [presenter] with Forethought Life Insurance Company. Today we ll be talking about some of the myths and truths regarding fixed index annuities. 1 You may have wondered whether an annuity

Implications of Withdrawals and Loans from a Life Insurance Policy

Implications of Withdrawals and Loans from a Life Insurance Policy Life insurance is frequently structured to provide income that can be used for various needs, such as supplemental retirement income,

Implications of Withdrawals and Loans from a Life Insurance Policy Life insurance is frequently structured to provide income that can be used for various needs, such as supplemental retirement income,

PruLife Founders Plus UL

PruLife Founders Plus UL PREPARE FOR THE POSSIBILITIES IN LIFE The Prudential Insurance Company of America 0255027 0255027-00001-00 Ed. 12/2013 Exp. 06/12/2015 A FINANCIAL LEADER FOR OVER 135 YEARS Prudential

PruLife Founders Plus UL PREPARE FOR THE POSSIBILITIES IN LIFE The Prudential Insurance Company of America 0255027 0255027-00001-00 Ed. 12/2013 Exp. 06/12/2015 A FINANCIAL LEADER FOR OVER 135 YEARS Prudential

WealthMax Bonus Life. Provide a Financial Legacy Single Premium Index Life Insurance

WealthMax Bonus Life Provide a Financial Legacy Single Premium Index Life Insurance Are tax-deferral and building a financial legacy important to you? Are you concerned about liquidity to cover expenses

WealthMax Bonus Life Provide a Financial Legacy Single Premium Index Life Insurance Are tax-deferral and building a financial legacy important to you? Are you concerned about liquidity to cover expenses

Understanding fixed index universal life insurance

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation potential, and tax advantages in one policy M-3959 Understanding fixed

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation potential, and tax advantages in one policy M-3959 Understanding fixed

Voya SmartDesign Multi-Rate Index Annuity

Voya Insurance and Annuity Company Deferred Modified Guaranteed Annuity Prospectus Voya SmartDesign Multi-Rate Index Annuity May 1, 2015 This prospectus describes Voya SmartDesign Multi-Rate Index Annuity,

Voya Insurance and Annuity Company Deferred Modified Guaranteed Annuity Prospectus Voya SmartDesign Multi-Rate Index Annuity May 1, 2015 This prospectus describes Voya SmartDesign Multi-Rate Index Annuity,

Designed for growth. Destined to provide. ULTRA INDEX SM UNIVERSAL LIFE INSURANCE LBL7376-2

Designed for growth. Destined to provide. PRODUCT OVERVIEW ULTRA INDEX SM UNIVERSAL LIFE INSURANCE Designed for growth. Destined to provide. Taking care of your family means more than protecting them.

Designed for growth. Destined to provide. PRODUCT OVERVIEW ULTRA INDEX SM UNIVERSAL LIFE INSURANCE Designed for growth. Destined to provide. Taking care of your family means more than protecting them.

White Paper Equity Indexed Universal Life Insurance

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Synergy Global Advantage Gold. Fixed Indexed Universal Life Insurance Consumer Brochure. Distributed by:

Synergy Global Advantage Gold Fixed Indexed Universal Life Insurance Consumer Brochure Distributed by: ADV 1188 (12-2011) Fidelity & Guaranty Life Insurance Company Rev. 09-2014 14-680 Synergy Global Advantage

Synergy Global Advantage Gold Fixed Indexed Universal Life Insurance Consumer Brochure Distributed by: ADV 1188 (12-2011) Fidelity & Guaranty Life Insurance Company Rev. 09-2014 14-680 Synergy Global Advantage

The Navigator. Fall 2015 Issue 5. Life Insurance: A Risk Mitigation Tool that Should Not be Considered an Investment

The Navigator A Financial Planning Resource from Pekin Singer Strauss Asset Management Fall 2015 Issue 5 Life insurance can be a highly effective risk management tool that should have a place in most Americans

The Navigator A Financial Planning Resource from Pekin Singer Strauss Asset Management Fall 2015 Issue 5 Life insurance can be a highly effective risk management tool that should have a place in most Americans

Important Information about your Annuity

Robert W. Baird & Co. Incorporated Important Information about your Annuity Annuities are long-term investments that may help you meet or supplement your retirement and other long-term goals. Annuities

Robert W. Baird & Co. Incorporated Important Information about your Annuity Annuities are long-term investments that may help you meet or supplement your retirement and other long-term goals. Annuities

QUICK NOTES SUPPLEMENTAL STUDY GUIDE NEW JERSEY

QUICK NOTES SUPPLEMENTAL STUDY GUIDE NEW JERSEY A REVIEW SUPPLEMENT FOR THE NEW JERSEY LIFE, ACCIDENT & HEALTH STATE LICENSING EXAM (April 2016 Edition) What is Insurance Schools Quick Notes Supplemental

QUICK NOTES SUPPLEMENTAL STUDY GUIDE NEW JERSEY A REVIEW SUPPLEMENT FOR THE NEW JERSEY LIFE, ACCIDENT & HEALTH STATE LICENSING EXAM (April 2016 Edition) What is Insurance Schools Quick Notes Supplemental

Life insurance product portfolio

Aviva Life and Annuity Company Life insurance product portfolio Welcome Home to Aviva Universal Life Insurance that is built around you. 15440 9/10 Life insurance built for the many stages of life Aviva

Aviva Life and Annuity Company Life insurance product portfolio Welcome Home to Aviva Universal Life Insurance that is built around you. 15440 9/10 Life insurance built for the many stages of life Aviva

Make your next move Put tax-advantaged protection and growth potential into your future plan

Wealth Protection Expertise SM Make your next move Put tax-advantaged protection and growth potential into your future plan LIFE SOLUTIONS Not a deposit Not FDIC-insured May go down in value Not insured

Wealth Protection Expertise SM Make your next move Put tax-advantaged protection and growth potential into your future plan LIFE SOLUTIONS Not a deposit Not FDIC-insured May go down in value Not insured

Allianz MasterDex X Annuity. Allianz Life Insurance Company of North America CB52575-NFA-CA-2. Page 1 of 16

Allianz Life Insurance Company of North America CB52575-NFA-CA-2 Page 1 of 16 Discover the MasterDex X Annuity from Allianz. A fixed index annuity from Allianz can be a valuable asset. A prudent plan shouldn

Allianz Life Insurance Company of North America CB52575-NFA-CA-2 Page 1 of 16 Discover the MasterDex X Annuity from Allianz. A fixed index annuity from Allianz can be a valuable asset. A prudent plan shouldn