Health Insurance and the Affliction of Choice. Saurabh Bhargava, Carnegie Mellon University

|

|

|

- Aron Stokes

- 8 years ago

- Views:

Transcription

1 Health Insurance and the Affliction of Choice Saurabh Bhargava, Carnegie Mellon University Brookings Institute Conference on Behavioral Economics September 2015

2 Recent Explosion in Health Plan Choice Typical ACA Marketplace enrollee faces 47 plan options Typical Medicare Part D enrollee faces 30 plan options

3 Economic Rationale for Expanding Choice? Exchanges offer Americans competition, choice, and clout. Insurance companies will compete for business on a transparent, level playing field, driving down costs, and Exchanges will give individuals a choice of plans to fit their needs. - Kathleen Sebelius, former HHS Secretary Economic rationale for expanded choice presumes individuals make sensible health plan decisions

4 New Evidence on Quality of Health Plan Choice Bhargava, Saurabh, George Loewenstein, and Justin Sydnor. Do Individuals Make Sensible Health Plan Decisions? NBER Working Paper No , Major US Firm - Fortune 50 company ($100B+ revenue) - 50,000+ benefit eligible employees - Self-insured health coverage since 2008 Data on Employee Choice and Spending for 2010 to key features of firm setting offer litmus test for assessing employee ability to make sensible choices

5 1 Firm Let Individuals Build their Own Plan BYO PLAN MENU (single-coverage employees) Deductible Choice: - $350 - $500 - $750 - $1,000 Coinsurance: - 90% - 80% Out-of-Pocket Maximum - $1,500 - $2,500 - $3,000 Office Visit Copayment - $15 - $25

6 2 Employees Chose from Standardized Menus

7 Employee Medical Spending Fraction with those Total Health Bills 3 Nearly Every Low-Deductible Plan was Dominated Total Health Bills 0 For any level of health expense nearly every plan w/ $1k deductible was cheaper than otherwise equivalent low deductible plans

8 So Do Employees Make Sensible Plan Decisions? 55% of employees chose financially dominated health plans (61% on pre-tax basis) Example: Employees who chose $500 deductible over the $1,000 deductible spent $630 in premiums to avoid expected $230 in costs (max of $500) Economic consequences of are significant excess cost equivalent to 42% of premiums Almost 50% of employees Low income employees most likely to select plans with poor economic value

9 Why Did Employees Make Such Decisions? We conducted a series of experiments in which ~4,000 thousand US adult subjects were asked to make hypothetical plan choices from simplified menus Complexity of Choice Interface Low Search Motivation / Trust Low Health Plan Literacy EXPERIMENT 1 EXPERIMENT 2 EXPERIMENT 3 Search and menu complexity modestly important but most still chose dominated plans when choosing from menu w/ 4 plans varying only in deductible and price Subjects suffered from very low health insurance literacy most could not evaluate basic differences in economic value of plans

Employee Sample N =")

10 But Employees Do Not Choose Randomly Simple Choice Menu (Experiment) Employee Sample N = 2,317

Employee")

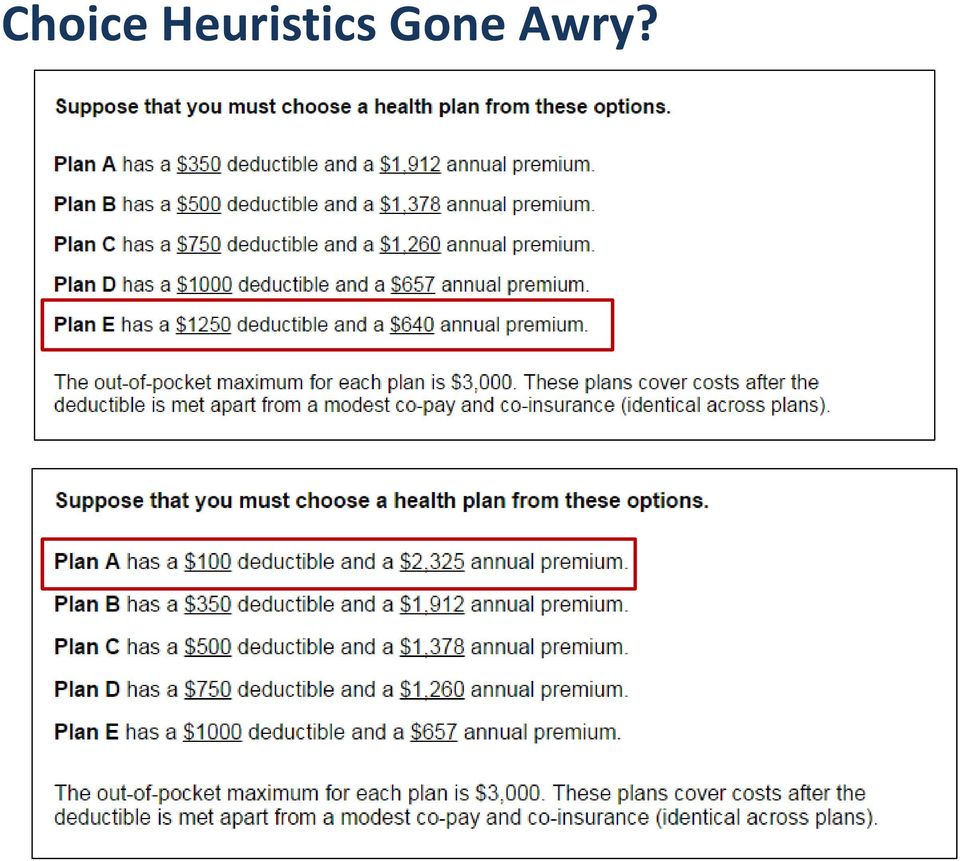

11 Choice Heuristics Gone Awry?

12 Deductible Choice Sensitive to Irrelevant Context Choices appear consistent with heuristic choice strategy where individuals select plans based on perceived health and risk-tolerance but not comparison of plan values (ongoing work with Loewenstein and Sydnor)

13 Do ACA Exchange Enrollees Make Sensible Choices? Bhargava, Saurabh, and George Loewenstein, and Shlomo Benartzi. The Health Exchanges and the Behavioral Economics of Plan Choice Under Review. Exchange adopted Metal Labels to help guide plan choice

14 Tier choice is highly financially consequential but Metal Labels not likely to lead to better choices

15 (Behavioral) Policy Tools for a Complex World Bhargava, Saurabh, and George Loewenstein. Behavioral Economics and Public Policy 102: Beyond Nudging American Economic Review, Papers & Proceedings, Vol. 105, No. 5, pp , Health Plan choices are growing in complexity like other financial choices May be limits to informational disclosures, marketing interventions, and education Perhaps we should move beyond traditional nudges and marketing: - Customized actuarially-based recommendations - Restrict choice menus to those appropriate for each individual - Simplify the actual incentives that underlie insurance Fundamental simplification not only likely to lead to better choice but better utilization and greater provider competition

16 Thank you

NBER WORKING PAPER SERIES DO INDIVIDUALS MAKE SENSIBLE HEALTH INSURANCE DECISIONS? EVIDENCE FROM A MENU WITH DOMINATED OPTIONS

NBER WORKING PAPER SERIES DO INDIVIDUALS MAKE SENSIBLE HEALTH INSURANCE DECISIONS? EVIDENCE FROM A MENU WITH DOMINATED OPTIONS Saurabh Bhargava George Loewenstein Justin Sydnor Working Paper 21160 http://www.nber.org/papers/w21160

NBER WORKING PAPER SERIES DO INDIVIDUALS MAKE SENSIBLE HEALTH INSURANCE DECISIONS? EVIDENCE FROM A MENU WITH DOMINATED OPTIONS Saurabh Bhargava George Loewenstein Justin Sydnor Working Paper 21160 http://www.nber.org/papers/w21160

Do Individuals Make Sensible (Health) Insurance Decisions? Evidence from a Menu with Dominated Options

Insurance Decisions? Evidence from a Menu with Dominated Options") Do Individuals Make Sensible (Health) Insurance Decisions? Evidence from a Menu with Dominated Options Saurabh Bhargava *, George Loewenstein *, and Justin Sydnor + Carnegie Mellon University * University

Do Individuals Make Sensible (Health) Insurance Decisions? Evidence from a Menu with Dominated Options Saurabh Bhargava *, George Loewenstein *, and Justin Sydnor + Carnegie Mellon University * University

INDIVIDUAL HEALTH INSURANCE GUIDE. Introduction. What is the Health Insurance Marketplace?

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

Empowering the Consumer: The Ultimate Health Care Stakeholder

Empowering the Consumer: The Ultimate Health Care Stakeholder Rebecca Burkholder Alliance for Health Reform Briefing July 24, 2015 REBECCA BURKHOLDER @ncl_tweets 1 Estimated Source of Insurance Coverage,

Empowering the Consumer: The Ultimate Health Care Stakeholder Rebecca Burkholder Alliance for Health Reform Briefing July 24, 2015 REBECCA BURKHOLDER @ncl_tweets 1 Estimated Source of Insurance Coverage,

Medicare Supplement Standardized Plans

Medicare Supplement Standardized Plans There are many kinds of Medicare Supplement Plan Different plans are designated with a letter Available plans include A, B, C, D, F, G, K, L, M, & N Not all plans

Medicare Supplement Standardized Plans There are many kinds of Medicare Supplement Plan Different plans are designated with a letter Available plans include A, B, C, D, F, G, K, L, M, & N Not all plans

Reporting Requirements for Employers and Health Plans

Brought to you by Cross Employee Benefits Reporting Requirements for Employers and Health Plans The Affordable Care Act (ACA) created a number of federal reporting requirements for employers and health

Brought to you by Cross Employee Benefits Reporting Requirements for Employers and Health Plans The Affordable Care Act (ACA) created a number of federal reporting requirements for employers and health

Insights AdvocateCare Health Insurance Exchanges

Insights AdvocateCare Physician Edition April 16, 2013 Executive Summary (HIX, also called Health Insurance Marketplace) a key provision of The Patient Protection and Affordable Care Act (ACA, Affordable

Insights AdvocateCare Physician Edition April 16, 2013 Executive Summary (HIX, also called Health Insurance Marketplace) a key provision of The Patient Protection and Affordable Care Act (ACA, Affordable

Make sure you re covered for your biologic medicine!

It s open enrollment time Make sure you re covered for your biologic medicine! Joint Decisions is brought to you by Janssen Biotech, Inc., in partnership with CreakyJoints CreakyJoints Bringing arthritis

It s open enrollment time Make sure you re covered for your biologic medicine! Joint Decisions is brought to you by Janssen Biotech, Inc., in partnership with CreakyJoints CreakyJoints Bringing arthritis

Medicare Supplemental Insurance - Medigap Plans

Medicare Supplemental Insurance (Medigap) All Medigap s A through N The available supplemental insurance plans that are offered are lettered plans A-N. Each plan offers a different benefits package and

Medicare Supplemental Insurance (Medigap) All Medigap s A through N The available supplemental insurance plans that are offered are lettered plans A-N. Each plan offers a different benefits package and

WASHINGTON QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS

WASHINGTON QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS December 2013 Support for this resource provided through a grant from the Robert Wood Johnson Foundation s State Health Reform Assistance

WASHINGTON QUALIFIED HEALTH PLAN SELECTION: CONSIDERATIONS FOR CONSUMERS December 2013 Support for this resource provided through a grant from the Robert Wood Johnson Foundation s State Health Reform Assistance

Survey of Non-Group Health Insurance Enrollees

Survey of Non-Group Health Insurance Enrollees A First Look At People Buying Their Own Health Insurance Following Implementation Of The Affordable Care Act Executive Summary... 1 About The Groups Described

Survey of Non-Group Health Insurance Enrollees A First Look At People Buying Their Own Health Insurance Following Implementation Of The Affordable Care Act Executive Summary... 1 About The Groups Described

CMS NEWS. October, 25, 2012 (202) 690-6145

690-6145") DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Room 352-G 200 Independence Avenue, SW Washington, DC 20201 CMS NEWS FOR IMMEDIATE RELEASE Contact: CMS Media Relations October,

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services Room 352-G 200 Independence Avenue, SW Washington, DC 20201 CMS NEWS FOR IMMEDIATE RELEASE Contact: CMS Media Relations October,

Guide to the Summary and Benefits of Coverage

Guide to the Summary and Benefits of Coverage The Affordable Care Act (ACA) makes health insurance available to nearly all Americans. Each state has a health insurance marketplace, also known as a health

Guide to the Summary and Benefits of Coverage The Affordable Care Act (ACA) makes health insurance available to nearly all Americans. Each state has a health insurance marketplace, also known as a health

CENTERS FOR MEDICARE & MEDICAID SERVICES. Cost

CENTERS FOR MEDICARE & MEDICAID SERVICES Things to Think about when You Compare Medicare Drug Coverage You have two options to get Medicare coverage for your prescription drugs. If you have Original Medicare,

CENTERS FOR MEDICARE & MEDICAID SERVICES Things to Think about when You Compare Medicare Drug Coverage You have two options to get Medicare coverage for your prescription drugs. If you have Original Medicare,

Important Effective Dates for Employers and Health Plans

Brought to you by Krempa Associates, Inc. Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Brought to you by Krempa Associates, Inc. Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Important Effective Dates for Employers and Health Plans

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

HEALTH CARE REFORM: Grandfathered Health Plans

HEALTH CARE REFORM: Grandfathered Health Plans Guidance concerning grandfathered health plan status was issued on June 17, 2010, by the Departments of Labor, Treasury and Health and Human Services with

HEALTH CARE REFORM: Grandfathered Health Plans Guidance concerning grandfathered health plan status was issued on June 17, 2010, by the Departments of Labor, Treasury and Health and Human Services with

Important Effective Dates for Employers and Health Plans

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Cost-sharing Charges in Marketplace Health Insurance Plans - Part II

September 2013 Cost-sharing Charges in Marketplace Health Insurance Plans - Part II Starting in January 2014, new health insurance marketplaces (also called exchanges) will provide a way for people to

September 2013 Cost-sharing Charges in Marketplace Health Insurance Plans - Part II Starting in January 2014, new health insurance marketplaces (also called exchanges) will provide a way for people to

$243.41 $34.69 16.62% 29497DE0090001 Aetna Bronze $15 Copay PPO Bronze 26 $ 212.88

Marketplace plans that were available in Coverage years and/or 2015. 29497DE0090001 Aetna Bronze $15 Copay PPO Bronze 0-20 $ 132.01 $153.95 $21.94 16.62% 29497DE0090001 Aetna Bronze $15 Copay PPO Bronze

Marketplace plans that were available in Coverage years and/or 2015. 29497DE0090001 Aetna Bronze $15 Copay PPO Bronze 0-20 $ 132.01 $153.95 $21.94 16.62% 29497DE0090001 Aetna Bronze $15 Copay PPO Bronze

Massachusetts Health Connector logo. The Health Connector: Massachusetts New and Improved Health Insurance Marketplace

Massachusetts Health Connector logo The Health Connector: Massachusetts New and Improved Health Insurance Marketplace Massachusetts: The model for national health care reform 1 Massachusetts led the nation

Massachusetts Health Connector logo The Health Connector: Massachusetts New and Improved Health Insurance Marketplace Massachusetts: The model for national health care reform 1 Massachusetts led the nation

Cancer Patients Access to Care Post- ACA. Jennifer Singleterry, MA Senior Analyst, Policy Analysis and Legislative Support

Cancer Patients Access to Care Post- ACA Jennifer Singleterry, MA Senior Analyst, Policy Analysis and Legislative Support Disclosure Information Jennifer Singleterry AACR Annual Meeting, April 2016 I have

Cancer Patients Access to Care Post- ACA Jennifer Singleterry, MA Senior Analyst, Policy Analysis and Legislative Support Disclosure Information Jennifer Singleterry AACR Annual Meeting, April 2016 I have

New HHS Rules for 2016 Tighten "Minimum Value" Standard

New HHS Rules for 2016 Tighten "Minimum Value" Standard An apparently unintended loophole in the Affordable Care Act (ACA) has been closed. Under previous rules, large employers (as defined under the act)

New HHS Rules for 2016 Tighten "Minimum Value" Standard An apparently unintended loophole in the Affordable Care Act (ACA) has been closed. Under previous rules, large employers (as defined under the act)

Increasing participation in the Medicare savings programs and the low-income drug subsidy. Joan Sokolovsky and Hannah Neprash November 8, 2007

Increasing participation in the Medicare savings programs and the low-income drug subsidy Joan Sokolovsky and Hannah Neprash November 8, 2007 Key findings Medicare beneficiaries typically have lower incomes

Increasing participation in the Medicare savings programs and the low-income drug subsidy Joan Sokolovsky and Hannah Neprash November 8, 2007 Key findings Medicare beneficiaries typically have lower incomes

The Affordable Care Act and the Health Insurance Marketplace

The Affordable Care Act and the Health Insurance Marketplace Are You Ready? The Affordable Care Act is here! In March 2010, President Obama signed into law the Affordable Care Act (ACA), putting comprehensive

The Affordable Care Act and the Health Insurance Marketplace Are You Ready? The Affordable Care Act is here! In March 2010, President Obama signed into law the Affordable Care Act (ACA), putting comprehensive

illinois health insurance marketplace

illinois health insurance marketplace healthcare reform is coming. find answers here. healthcarereform.illinois.gov The Affordable Care Act. What it means for you. In March of 2010, the Affordable Care

illinois health insurance marketplace healthcare reform is coming. find answers here. healthcarereform.illinois.gov The Affordable Care Act. What it means for you. In March of 2010, the Affordable Care

The Health Benefit Exchange and the Commercial Insurance Market

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

Health Savings Accounts & High Deductible Health Plans

Health Savings Accounts & High Deductible Health Plans Definitions Consumer Driven Health Plan ( CDHP ) A health insurance plan designed to give you more control over your health care spending. CDHPs incorporate

Health Savings Accounts & High Deductible Health Plans Definitions Consumer Driven Health Plan ( CDHP ) A health insurance plan designed to give you more control over your health care spending. CDHPs incorporate

PRIVATE HEALTH INSURANCE. Early Evidence Finds Premium Tax Credit Likely Contributed to Expanded Coverage, but Some Lack Access to Affordable Plans

United States Government Accountability Office Report to Congressional Committees March 2015 PRIVATE HEALTH INSURANCE Early Evidence Finds Premium Tax Credit Likely Contributed to Expanded Coverage, but

United States Government Accountability Office Report to Congressional Committees March 2015 PRIVATE HEALTH INSURANCE Early Evidence Finds Premium Tax Credit Likely Contributed to Expanded Coverage, but

List of Insurance Terms and Definitions for Uniform Translation

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

Term actuarial value Affordable Care Act allowed charge Definition The percentage of total average costs for covered benefits that a plan will cover. For example, if a plan has an actuarial value of 70%,

Health Insurance Overview

Spotsylvania County Open Enrollment August 10 to 28, 2015 Plan Year: October 1, 2015 to September 30, 2016 Health Insurance Overview All Full Time employees are eligible to participate in the County Health

Spotsylvania County Open Enrollment August 10 to 28, 2015 Plan Year: October 1, 2015 to September 30, 2016 Health Insurance Overview All Full Time employees are eligible to participate in the County Health

REGULATORY UPDATE Vol. 1 No. 18

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

REGULATORY UPDATE Vol. 1 No. 18 FAQs on Exchanges August 7, 2013 IN THIS ISSUE FAQs on Exchanges Employer Mandate Delay Transitional Guidance Issued Individual Mandate Final Rules Issued Possible Exchange

Enrollment in a similar plan

Automatic Plan Renewals If you bought a health plan through the Marketplace in 2014, you ll probably be automatically enrolled for 2015. If you don t take any action, your coverage will start January 1,

Automatic Plan Renewals If you bought a health plan through the Marketplace in 2014, you ll probably be automatically enrolled for 2015. If you don t take any action, your coverage will start January 1,

Not All Private Exchanges are Created Equal

Not All Private Exchanges are Created Equal Know the Advantages, Know the Stats, Know the Features E mployers are increasingly embracing private insurance exchanges. Why? Find out about the advantages

Not All Private Exchanges are Created Equal Know the Advantages, Know the Stats, Know the Features E mployers are increasingly embracing private insurance exchanges. Why? Find out about the advantages

Pre-Existing Condition Insurance Plan Program

Pre-Existing Condition Insurance Plan Program Office of Insurance Programs Center for Consumer Information and Insurance Oversight Centers for Medicare & Medicaid Services Center for Consumer Information

Pre-Existing Condition Insurance Plan Program Office of Insurance Programs Center for Consumer Information and Insurance Oversight Centers for Medicare & Medicaid Services Center for Consumer Information

Chao & Company, Ltd. 8460 Tyco Road, Suite E, Vienna, Virginia 22182 Telephone (703) 847-4380, Facsimile (703) 847-4384 www.chaoco.

847-4380, Facsimile (703) 847-4384 www.chaoco.") The Affordable Care Act 1302(d)(1) defines the levels of health plan coverage for the purpose of meeting the following main objectives: To establish the minimum level of coverage an applicable individual

The Affordable Care Act 1302(d)(1) defines the levels of health plan coverage for the purpose of meeting the following main objectives: To establish the minimum level of coverage an applicable individual

NEW HEALTH MARKETPLACE

NEW HEALTH INSURANCE MARKETPLACE DISCLAIMER The information in this presentation is based on information provided www.healthcare.gov. It is not provided as advice for your personal situation. Georgia Perimeter

NEW HEALTH INSURANCE MARKETPLACE DISCLAIMER The information in this presentation is based on information provided www.healthcare.gov. It is not provided as advice for your personal situation. Georgia Perimeter

Reforming Medicare s benefit design. Julie Lee, Scott Harrison, and Joan Sokolovsky March 8, 2012

Reforming Medicare s benefit design Julie Lee, Scott Harrison, and Joan Sokolovsky March 8, 2012 Outline of today s presentation Policy objectives Key design issues Illustrative benefit package With and

Reforming Medicare s benefit design Julie Lee, Scott Harrison, and Joan Sokolovsky March 8, 2012 Outline of today s presentation Policy objectives Key design issues Illustrative benefit package With and

Health Insurance Marketplace. vhealth insurance exchanges. What to expect in 2014. What to expect in 2014

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

vhealth insurance exchanges Health Insurance Marketplace What to expect in 2014 What to expect in 2014 The basics of exchanges As part of the Affordable Care Act (ACA or health care reform law), starting

Your Guide to Getting Health Insurance

Your Guide to Getting Health Insurance Getting Health Insurance: KEY QUESTIONS The following is a list of key questions and things to think about when selecting health insurance to best meet your needs

Your Guide to Getting Health Insurance Getting Health Insurance: KEY QUESTIONS The following is a list of key questions and things to think about when selecting health insurance to best meet your needs

Health Insurance Exchanges: Tools for Success

Health Insurance Exchanges: Tools for Success Health insurance exchanges present a significant opportunity to coordinate and simplify access to affordable health insurance. By 2020, more than 27 million

Health Insurance Exchanges: Tools for Success Health insurance exchanges present a significant opportunity to coordinate and simplify access to affordable health insurance. By 2020, more than 27 million

4/8/2013. Health Care Reform and the. NYS Exchange. Dr. Arthur Vercillo, MD Regional President April 8, 2013. Health Care Reform and the NYS Exchange

Health Care Reform and the NYS Exchange Presentation to the Health Planning Council Advisory Board April 8, 2013, Ithaca NY By Dr. Arthur Vercillo, MD Additional resources on next to last slide. Health

Health Care Reform and the NYS Exchange Presentation to the Health Planning Council Advisory Board April 8, 2013, Ithaca NY By Dr. Arthur Vercillo, MD Additional resources on next to last slide. Health

The New Health Law & Small Businesses

The New Health Law & Small Businesses October 2013 1 Goals of the New Health Law Affordable Care Act (ACA) Protect consumers against unfair insurance industry practices Give consumers more insurance options

The New Health Law & Small Businesses October 2013 1 Goals of the New Health Law Affordable Care Act (ACA) Protect consumers against unfair insurance industry practices Give consumers more insurance options

Insurance Exchanges: New Market Opportunities & Threats to Access. February 2014 avalerehealth.net

Insurance Exchanges: New Market Opportunities & Threats to Access February 2014 avalerehealth.net Despite Slow Initial Enrollment, Exchange Participation Is Accelerating Most Sign-Ups Expected Close to

Insurance Exchanges: New Market Opportunities & Threats to Access February 2014 avalerehealth.net Despite Slow Initial Enrollment, Exchange Participation Is Accelerating Most Sign-Ups Expected Close to

Hospitals and the Affordable Care Act (ACA)

") Hospitals and the Affordable Care Act (ACA) General Housekeeping If you experience any technical difficulties during the webinar, please contact GoToMeeting.com Corporate Account Customer Support at: 1-888-259-8414

Hospitals and the Affordable Care Act (ACA) General Housekeeping If you experience any technical difficulties during the webinar, please contact GoToMeeting.com Corporate Account Customer Support at: 1-888-259-8414

Bronze, Silver, Gold, or Platinum: How to Choose the Right Level of Coverage in Covered California

Fact Sheet NOVEMBER 2014 Bronze, Silver, Gold, or Platinum: How to Choose the Right Level of Coverage in Covered California Summary The Affordable Care Act (ACA) requires that Covered California offer

Fact Sheet NOVEMBER 2014 Bronze, Silver, Gold, or Platinum: How to Choose the Right Level of Coverage in Covered California Summary The Affordable Care Act (ACA) requires that Covered California offer

Issue Brief: The Health Benefit Exchange and the Small Employer Market

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Massachusetts Health Connector logo. What Does National Health Care Reform Mean for You?

Massachusetts Health Connector logo What Does National Health Care Reform Mean for You? 1 National health care reform offers more opportunities for individuals, families, and small businesses to save on

Massachusetts Health Connector logo What Does National Health Care Reform Mean for You? 1 National health care reform offers more opportunities for individuals, families, and small businesses to save on

Health Insurance / Learning Targets

Health Insurance / Learning Targets Compare the basic principles of at least four different health insurance plans Define key terms pertaining to health insurance Health Insurance I have a hospital bill

Health Insurance / Learning Targets Compare the basic principles of at least four different health insurance plans Define key terms pertaining to health insurance Health Insurance I have a hospital bill

Why the Affordable Care Act Matters for Women: Health Insurance 101

Why the Affordable Care Act Matters for Women: Health Insurance 101 APRIL 2014 Women are the health care decision makers in our country they make approximately 80 percent of the health care decisions in

Why the Affordable Care Act Matters for Women: Health Insurance 101 APRIL 2014 Women are the health care decision makers in our country they make approximately 80 percent of the health care decisions in

As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal government.

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA)

") Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA) Brought to you by Aon Presented by: Ryan Comstock & Shawna Brown This information is provided for informational purposes only and is

Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA) Brought to you by Aon Presented by: Ryan Comstock & Shawna Brown This information is provided for informational purposes only and is

How ACA is Changing Employer Health Benefits and the Marketplace Presented by:

North Carolina State Health Plan How ACA is Changing Employer Health Benefits and the Marketplace Presented by: J. Richard Johnson Senior Vice President, Public Sector Health Practice Leader rjohnson@segalco.com

North Carolina State Health Plan How ACA is Changing Employer Health Benefits and the Marketplace Presented by: J. Richard Johnson Senior Vice President, Public Sector Health Practice Leader rjohnson@segalco.com

Affordable Care Act HEALTHCARE.GOV. Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health

HEALTHCARE.GOV Affordable Care Act Marketplace Implementation Briefing Virginia Organizing Marketplace Public Forum August 20, 2013 Joanne Corte Grossi, MIPP Regional Director U.S. Department of Health

Submitted online in connection with: Health Care Workshop, Project No. P131207

Federal Trade Commission Washington, DC 20580 Submitted online in connection with: Health Care Workshop, Project No. P131207 Re: Examining Health Care Competition On behalf of our nearly 5,000 member hospitals,

Federal Trade Commission Washington, DC 20580 Submitted online in connection with: Health Care Workshop, Project No. P131207 Re: Examining Health Care Competition On behalf of our nearly 5,000 member hospitals,

Choosing the Best Plan for You: A Tool for Purchasing Coverage in the Health Insurance Exchange

Choosing the Best Plan for You: A Tool for Purchasing Coverage in the Health Insurance Exchange The Affordable Care Act (ACA) makes health insurance available to nearly all Americans and the law requires

Choosing the Best Plan for You: A Tool for Purchasing Coverage in the Health Insurance Exchange The Affordable Care Act (ACA) makes health insurance available to nearly all Americans and the law requires

How To Compare Health Insurance Plans

The three most important questions you need to ask Health care can be very expensive. Having a baby costs about $30,000, and so does the average three-day hospital stay. Health insurance is a way to reduce

The three most important questions you need to ask Health care can be very expensive. Having a baby costs about $30,000, and so does the average three-day hospital stay. Health insurance is a way to reduce

Scott Lyon, Senior Vice President Small Business Association of Michigan

Scott Lyon, Senior Vice President Small Business Association of Michigan Patient Protection and Affordable Care Act H.R. 3590 Health Care & Education Affordability Reconciliation Act H.R. 4872 20,000 30,000

Scott Lyon, Senior Vice President Small Business Association of Michigan Patient Protection and Affordable Care Act H.R. 3590 Health Care & Education Affordability Reconciliation Act H.R. 4872 20,000 30,000

ISSUE BRIEF. A Little Knowledge Is a Risky Thing: Wide Gap in What People Think They Know About Health Insurance and What They Actually Know

October 214 Amended A Little Knowledge Is a Risky Thing: Wide Gap in What People Think They Know About Health and What They Actually Know BY KATHRYN A. PAEZ AND CORETTA J. MALLERY Under the 2 Affordable

October 214 Amended A Little Knowledge Is a Risky Thing: Wide Gap in What People Think They Know About Health and What They Actually Know BY KATHRYN A. PAEZ AND CORETTA J. MALLERY Under the 2 Affordable

This glossary provides simple and straightforward definitions of key terms that are part of the health reform law.

This glossary provides simple and straightforward definitions of key terms that are part of the health reform law. A Affordable Care Act Also known as the ACA. A law that creates new options for people

This glossary provides simple and straightforward definitions of key terms that are part of the health reform law. A Affordable Care Act Also known as the ACA. A law that creates new options for people

April 2, 2012. Dear Mr. Bertko,

April 2, 2012 Mr. John Bertko, FSA, MAAA Director, Office of Special Initiatives and Pricing Center for Consumer Information and Insurance Oversight Centers for Medicare and Medicaid Services U.S. Department

April 2, 2012 Mr. John Bertko, FSA, MAAA Director, Office of Special Initiatives and Pricing Center for Consumer Information and Insurance Oversight Centers for Medicare and Medicaid Services U.S. Department

Mississippi Health Insurance Exchange Advisory Board. Final Recommendations Employer Participation

Mississippi Health Insurance Exchange Advisory Board Final Recommendations Employer Participation Background The Mississippi Health Insurance Exchange Advisory Board ( Advisory Board ) was formed in order

Mississippi Health Insurance Exchange Advisory Board Final Recommendations Employer Participation Background The Mississippi Health Insurance Exchange Advisory Board ( Advisory Board ) was formed in order

Patient Protection and Affordable Care Act of 2009: Immediate Health Insurance Market Reforms

Patient Protection and Affordable Care Act of 2009: Immediate Health Insurance Market Reforms Provision Notes Standards Development Applicability Effective Date PPACA Statutory Annual and Lifetime Limits

Patient Protection and Affordable Care Act of 2009: Immediate Health Insurance Market Reforms Provision Notes Standards Development Applicability Effective Date PPACA Statutory Annual and Lifetime Limits

National Health Reform and Your Business

National Health Reform and Your Business What Massachusetts Employers Need to Know About the Affordable Care Act and the Massachusetts Health Connector 2 National Health Reform and Your Business National

National Health Reform and Your Business What Massachusetts Employers Need to Know About the Affordable Care Act and the Massachusetts Health Connector 2 National Health Reform and Your Business National

MEDICARE SUPPLEMENT INSURANCE

MEDICARE SUPPLEMENT INSURANCE PROTECTIONfor Today s Senior Galveston, Texas P.O. Box 10627 Springfield, MO 65808 888.290.1085 Visit our web site at www.slaico.com ST-3707 American National Life Insurance

MEDICARE SUPPLEMENT INSURANCE PROTECTIONfor Today s Senior Galveston, Texas P.O. Box 10627 Springfield, MO 65808 888.290.1085 Visit our web site at www.slaico.com ST-3707 American National Life Insurance

What is a Medicare Advantage Plan?

CENTERS FOR MEDICARE & MEDICAID SERVICES What is a Medicare Advantage Plan? A Medicare Advantage Plan (like an HMO or PPO) is a way to get your Medicare benefits. Unlike Original Medicare, in which the

CENTERS FOR MEDICARE & MEDICAID SERVICES What is a Medicare Advantage Plan? A Medicare Advantage Plan (like an HMO or PPO) is a way to get your Medicare benefits. Unlike Original Medicare, in which the

Dental Loss Ratios. Factors to Consider in Establishing a Minimum Loss Ratio for Dental Insurance in California. January 16, 2014.

Dental Loss Ratios Factors to Consider in Establishing a Minimum Loss Ratio for Dental Insurance in California January 16, 2014 Prepared by The Blue Sky Consulting Group Contents ACKNOWLEDGEMENTS... 3

Dental Loss Ratios Factors to Consider in Establishing a Minimum Loss Ratio for Dental Insurance in California January 16, 2014 Prepared by The Blue Sky Consulting Group Contents ACKNOWLEDGEMENTS... 3

Exemptions for Plan Years Beginning on or after 9/23/2010

Health Care Reform: Grandfathered Plan Regulations Certain group health plans providing coverage on March 23, 2010 (the date health care reform was enacted) are "grandfathered plans," exempt from some,

Health Care Reform: Grandfathered Plan Regulations Certain group health plans providing coverage on March 23, 2010 (the date health care reform was enacted) are "grandfathered plans," exempt from some,

Understanding Private Health Insurance Plan Choices and Provider Networks

Understanding Private Health Insurance Plan Choices and Provider Networks Definitions Deductible Out-of-Pocket-Maximum Embedded Deductible Aggregate Deductible Networks PPO EPO HMO POS - HDHP HSA Catastrophic

Understanding Private Health Insurance Plan Choices and Provider Networks Definitions Deductible Out-of-Pocket-Maximum Embedded Deductible Aggregate Deductible Networks PPO EPO HMO POS - HDHP HSA Catastrophic

SENATE FILE NO. SF0026. Employee insurance participation-feasibility study. Sponsored by: Joint Labor, Health and Social Services Interim Committee

00 STATE OF WYOMING 0LSO-0 SENATE FILE NO. SF00 Employee insurance participation-feasibility study. Sponsored by: Joint Labor, Health and Social Services Interim Committee A BILL for AN ACT relating to

00 STATE OF WYOMING 0LSO-0 SENATE FILE NO. SF00 Employee insurance participation-feasibility study. Sponsored by: Joint Labor, Health and Social Services Interim Committee A BILL for AN ACT relating to

Making SHOP an Attractive Option for Small Employers: Tax and Other Strategies AMY MONAHAN & DANIEL SCHWARCZ UNIVERSITY OF MINNESOTA LAW SCHOOL

Making SHOP an Attractive Option for Small Employers: Tax and Other Strategies AMY MONAHAN & DANIEL SCHWARCZ UNIVERSITY OF MINNESOTA LAW SCHOOL Pre-ACA Tax Advantages Through various mechanisms, employers

Making SHOP an Attractive Option for Small Employers: Tax and Other Strategies AMY MONAHAN & DANIEL SCHWARCZ UNIVERSITY OF MINNESOTA LAW SCHOOL Pre-ACA Tax Advantages Through various mechanisms, employers

Open Enrollment 2015 November 12 November 26

Open Enrollment 2015 November 12 November 26 November 4 & 6, 2014 1 Brief Review of Affordable Care Act (ACA) What You Need to Know What you Need to do by November 26 What s New or Changing in 2015 Do

Open Enrollment 2015 November 12 November 26 November 4 & 6, 2014 1 Brief Review of Affordable Care Act (ACA) What You Need to Know What you Need to do by November 26 What s New or Changing in 2015 Do

Health Care Reform Checklist: Provisions, Obstacles and Solutions

Health Care Reform Checklist: Provisions, Obstacles and Solutions HEALTH CARE REFORM PROVISION: COVERAGE FOR CHILDREN UNTIL AGE 26 Summary of Benefit: Benefits are the same as those for other dependent

Health Care Reform Checklist: Provisions, Obstacles and Solutions HEALTH CARE REFORM PROVISION: COVERAGE FOR CHILDREN UNTIL AGE 26 Summary of Benefit: Benefits are the same as those for other dependent

Delaware Rates for Aetna Life Insurance Company Marketplace QHPs - Individual Marketplace Plan Year 2016

Delaware s for Aetna Life Insurance Company Marketplace QHPs - Individual Marketplace Plan Year 2016 that were available in Coverage years and/or. Tobacco Change ($) 29497DE0090001 Aetna Bronze $20 Copay

Delaware s for Aetna Life Insurance Company Marketplace QHPs - Individual Marketplace Plan Year 2016 that were available in Coverage years and/or. Tobacco Change ($) 29497DE0090001 Aetna Bronze $20 Copay

Disclaimer: This ACA is not the health reform bill UE would pass. We have been consistent in our support for Single Payer ( Medicare For All ) going

going") Disclaimer: This ACA is not the health reform bill UE would pass. We have been consistent in our support for Single Payer ( Medicare For All ) going back to the 1940s. However, the ACA is the law of the

Disclaimer: This ACA is not the health reform bill UE would pass. We have been consistent in our support for Single Payer ( Medicare For All ) going back to the 1940s. However, the ACA is the law of the

A Consumer s Guide to the Affordable Care Act

A Consumer s Guide to the Affordable Care Act The Affordable Care Act was designed to help make health care affordable for everyone. This guide will help you understand how the ACA affects individuals

A Consumer s Guide to the Affordable Care Act The Affordable Care Act was designed to help make health care affordable for everyone. This guide will help you understand how the ACA affects individuals

Session 30 PD, New research in Behavioral Economics in Health Care. Moderator/Presenter: Christopher James Coulter, FSA, MAAA, CERA

Session 30 PD, New research in Behavioral Economics in Health Care Moderator/Presenter: Christopher James Coulter, FSA, MAAA, CERA Presenters: Keith Ericson, Ph.D. Ben Handel, Ph.D. New Research in Behavioral

Session 30 PD, New research in Behavioral Economics in Health Care Moderator/Presenter: Christopher James Coulter, FSA, MAAA, CERA Presenters: Keith Ericson, Ph.D. Ben Handel, Ph.D. New Research in Behavioral

Old Law, New Impact: The Mental Health Benefit Parity Requirement

Old Law, New Impact: The Mental Health Benefit Parity Requirement The Mental Health Parity and Addiction Equity Act (MHPAEA) has been on the books for years. Yet some employers are about to feel the law's

Old Law, New Impact: The Mental Health Benefit Parity Requirement The Mental Health Parity and Addiction Equity Act (MHPAEA) has been on the books for years. Yet some employers are about to feel the law's

Exchange 101. August 2013

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

The Vermont Health Benefit Exchange: An Update

The Vermont Health Benefit Exchange: An Update Today s Discussion Health Reform Goals & Timeline Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like? Plan Design Enrollment

The Vermont Health Benefit Exchange: An Update Today s Discussion Health Reform Goals & Timeline Overview of Health Care Reform What is the Exchange? What Does the Exchange Look Like? Plan Design Enrollment

IRS Proposes Rules on Effect of Wellness Incentives on Play or Pay Obligations

IRS Proposes Rules on Effect of Wellness Incentives on Play or Pay Obligations A newly proposed IRS regulation provides additional guidance on how employers subject to the health reform law s play or pay

IRS Proposes Rules on Effect of Wellness Incentives on Play or Pay Obligations A newly proposed IRS regulation provides additional guidance on how employers subject to the health reform law s play or pay

Indiana University Peer Institution Benefits Comparison July 2009 Health Care Plans

Indiana Peer Institution Benefits Comparison July 2009 Summary of comparison with Big 10 universities and/or large employers: Most IU peers also provide healthcare benefits to part time employees (IU provides

Indiana Peer Institution Benefits Comparison July 2009 Summary of comparison with Big 10 universities and/or large employers: Most IU peers also provide healthcare benefits to part time employees (IU provides

THE AFFORDABLE CARE ACT ( ACT ), NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS

, NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS") Community THE AFFORDABLE CARE ACT ( ACT ), NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS Prepared for the 2014 Massachusetts Municipal Association Annual Meeting On March

Community THE AFFORDABLE CARE ACT ( ACT ), NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS Prepared for the 2014 Massachusetts Municipal Association Annual Meeting On March

Affordable Care Act 101: Understanding Federal Healthcare Reform

Affordable Care Act 101: Understanding Federal Healthcare Reform As of July 16, 2013 For more Information, please contact the Office of Countywide Healthcare Planning by e-mail: healthcareplanning@miamidade.gov

Affordable Care Act 101: Understanding Federal Healthcare Reform As of July 16, 2013 For more Information, please contact the Office of Countywide Healthcare Planning by e-mail: healthcareplanning@miamidade.gov

Medicare Prescription Drug Benefit

Medicare Prescription Drug Benefit Karen Tritz Overview Overview of new Medicare Prescription Drug Benefit The Timing and Process Implications for Working People with Disabilities Overview of Medicare

Medicare Prescription Drug Benefit Karen Tritz Overview Overview of new Medicare Prescription Drug Benefit The Timing and Process Implications for Working People with Disabilities Overview of Medicare

The New ACA Health Insurance Exchanges

The New ACA Health Insurance Exchanges Benefit Designs Relating to Prescription Medicines and Other Health Care Items and Services HEALTH Overview of Presentation: Summary of National Data o o Executive

The New ACA Health Insurance Exchanges Benefit Designs Relating to Prescription Medicines and Other Health Care Items and Services HEALTH Overview of Presentation: Summary of National Data o o Executive

Colorado Choice Health Plans

Quality Overview Colorado Choice Health Plans Accreditation Exchange Product Accrediting Organization: Accreditation Status: URAC Health Plan Accreditation (Marketplace HMO) Provisional Accreditation Commercial

Quality Overview Colorado Choice Health Plans Accreditation Exchange Product Accrediting Organization: Accreditation Status: URAC Health Plan Accreditation (Marketplace HMO) Provisional Accreditation Commercial

Affordable Care Act (ACA) Frequently Asked Questions

Frequently Asked Questions") Grandfathered policies Q1: What is grandfathered health plan coverage? A: The interim final rule on grandfathering under ACA generally defines grandfathered health plan coverage as coverage provided by

Grandfathered policies Q1: What is grandfathered health plan coverage? A: The interim final rule on grandfathering under ACA generally defines grandfathered health plan coverage as coverage provided by

Michigan Medicare Medicaid Assistance Program (MMAP)

") Michigan Medicare Medicaid Assistance Program (MMAP) Parts A& B Medicare Part A (hospital insurance) Solvent until 2030 4 years beyond last year s projection Suggests cost-savings measures are working

Michigan Medicare Medicaid Assistance Program (MMAP) Parts A& B Medicare Part A (hospital insurance) Solvent until 2030 4 years beyond last year s projection Suggests cost-savings measures are working

A contract that requires your health insurer to pay some or all of your health care costs in exchange for a premium.

HEALTH INSURANCE A contract that requires your health insurer to pay some or all of your health care costs in exchange for a premium. HI, I m Kate! I Got Health Insurance! Card Member ID: 0000000000 Group

HEALTH INSURANCE A contract that requires your health insurer to pay some or all of your health care costs in exchange for a premium. HI, I m Kate! I Got Health Insurance! Card Member ID: 0000000000 Group

As Reported by the Senate Insurance and Financial Institutions Committee. 130th General Assembly Regular Session Am. S. B. No. 99 2013-2014 A B I L L

As Reported by the Senate Insurance and Financial Institutions Committee 130th General Assembly Regular Session Am. S. B. No. 99 2013-2014 Senators Oelslager, Tavares Cosponsors: Senators Brown, Cafaro,

As Reported by the Senate Insurance and Financial Institutions Committee 130th General Assembly Regular Session Am. S. B. No. 99 2013-2014 Senators Oelslager, Tavares Cosponsors: Senators Brown, Cafaro,

Covered California: California s New Health Insurance Marketplace

Covered California: California s New Health Insurance Marketplace Amber Kemp, MBA Vice President, Health Care Coverage California Hospital Association Overview California s Uninsured Medi-Cal Expansion

Covered California: California s New Health Insurance Marketplace Amber Kemp, MBA Vice President, Health Care Coverage California Hospital Association Overview California s Uninsured Medi-Cal Expansion

What Healthcare Providers Need to Know about the Affordable Care Act (ACA)

") What Healthcare Providers Need to Know about the Affordable Care Act (ACA) General Housekeeping If you experience any technical difficulties during the webinar, please contact GoToMeeting.com Corporate

What Healthcare Providers Need to Know about the Affordable Care Act (ACA) General Housekeeping If you experience any technical difficulties during the webinar, please contact GoToMeeting.com Corporate

Restructuring Medicare Cost Sharing: Options and Implications

Restructuring Medicare Cost Sharing: Options and Implications Alliance for Health Reform Washington, D.C. Juliette Cubanski, Ph.D. Associate Director, Program on Medicare Policy Kaiser Family Foundation

Restructuring Medicare Cost Sharing: Options and Implications Alliance for Health Reform Washington, D.C. Juliette Cubanski, Ph.D. Associate Director, Program on Medicare Policy Kaiser Family Foundation

How To Calculate Health Insurance Premiums In The American Health Insurance Exchange

Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (ACA) Bernadette Fernandez Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy December 30, 2011

Health Insurance Premium Credits in the Patient Protection and Affordable Care Act (ACA) Bernadette Fernandez Specialist in Health Care Financing Thomas Gabe Specialist in Social Policy December 30, 2011

What Advisors Need to Know about Health- Care Planning

What Advisors Need to Know about Health- Care Planning June 18, 2013 by Dinesh Sharma Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor

What Advisors Need to Know about Health- Care Planning June 18, 2013 by Dinesh Sharma Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor

Common Complex Scenarios. Consumers Who Receive an Offer of Employer-Sponsored Coverage

Common Complex Scenarios Consumers Who Receive an Offer Center for Consumer Information and Insurance Oversight February 13, 2015 1 Samson, 55 years old, Married, Father of One Child Samson and his wife

Common Complex Scenarios Consumers Who Receive an Offer Center for Consumer Information and Insurance Oversight February 13, 2015 1 Samson, 55 years old, Married, Father of One Child Samson and his wife