Sri Lanka Accounting Standard -LKAS 11. Construction Contracts

|

|

|

- Hugh Chapman

- 8 years ago

- Views:

Transcription

1 Sri Lanka Accounting Standard -LKAS 11 Construction Contracts

2 -405-

3 Sri Lanka Accounting Standard -LKAS 11 Construction Contracts Sri Lanka Accounting Standard LKAS 11 Construction Contracts is set out in paragraphs All the paragraphs have equal authority. LKAS 11 should be read in the context of its objective, the Preface to Sri Lanka Accounting Standards and the Conceptual Framework for Financial Reporting. LKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance. Objective* The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with construction contracts. Because of the nature of the activity undertaken in construction contracts, the date at which the contract activity is entered into and the date when the activity is completed usually fall into different accounting periods. Therefore, the primary issue in accounting for construction contracts is the allocation of contract revenue and contract costs to the accounting periods in which construction work is performed. This Standard uses the recognition criteria established in the Framework for the Preparation and Presentation of Financial Statements to determine when contract revenue and contract costs should be recognised as revenue and expenses in the statement of comprehensive income. It also provides practical guidance on the application of these criteria. Scope 1 This Standard shall be applied in accounting for construction contracts in the financial statements of contractors. 2 [Deleted] Definitions 3 The following terms are used in this Standard with the meanings specified: A construction contract is a contract specifically negotiated for the construction of an asset or a combination of assets that are closely -406-

4 interrelated or interdependent in terms of their design, technology and function or their ultimate purpose or use. A fixed price contract is a construction contract in which the contractor agrees to a fixed contract price, or a fixed rate per unit of output, which in some cases is subject to cost escalation clauses. A cost plus contract is a construction contract in which the contractor is reimbursed for allowable or otherwise defined costs, plus a percentage of these costs or a fixed fee. 4 A construction contracts may be negotiated for the construction of a single asset such as a bridge, building, dam, pipeline, road, ship or tunnel. A construction contract may also deal with the construction of a number of assets which are closely interrelated or interdependent in terms of their design, technology and function or their ultimate purpose or use; examples of such contracts include those for the construction of refineries and other complex pieces of plant or equipment. 5 For the purposes of this Standard, construction contracts include: contracts for the rendering of services which are directly related to the construction of the asset, for example, those for the services of project managers and architects; and contracts for the destruction or restoration of assets, and the restoration of the environment following the demolition of assets. 6 Construction contracts are formulated in a number of ways which, for the purposes of this Standard, are classified as fixed price contracts and cost plus contracts. Some construction contracts may contain characteristics of both a fixed price contract and a cost plus contract, for example in the case of a cost plus contract with an agreed maximum price. In such circumstances, a contractor needs to consider all the conditions in paragraphs 23 and 24 in order to determine when to recognise contract revenue and expenses. Combining and segmenting construction contracts 7 The requirements of this Standard are usually applied separately to each construction contract. However, in certain circumstances, it is necessary to apply the Standard to the separately identifiable components of a single contract or to a group of contracts together in order to reflect the substance of a contract or a group of contracts

5 8 When a contract covers a number of assets, the construction of each asset shall be treated as a separate construction contract when: separate proposals have been submitted for each asset; each asset has been subject to separate negotiation and the contractor and customer have been able to accept or reject that part of the contract relating to each asset; and the costs and revenues of each asset can be identified. 9 A group of contracts, whether with a single customer or with several customers, shall be treated as a single construction contract when: the group of contracts is negotiated as a single package; the contracts are so closely interrelated that they are, in effect, part of a single project with an overall profit margin; and the contracts are performed concurrently or in a continuous sequence. 10 A contract may provide for the construction of an additional asset at the option of the customer or may be amended to include the construction of an additional asset. The construction of the additional asset shall be treated as a separate construction contract when: the asset differs significantly in design, technology or function from the asset or assets covered by the original contract; or the price of the asset is negotiated without regard to the original contract price. Contract revenue 11 Contract revenue shall comprise: the initial amount of revenue agreed in the contract; and variations in contract work, claims and incentive payments: -408-

6 (i) (ii) to the extent that it is probable that they will result in revenue; and they are capable of being reliably measured. 12 Contract revenue is measured at the fair value of the consideration received or receivable. The measurement of contract revenue is affected by a variety of uncertainties that depend on the outcome of future events. The estimates often need to be revised as events occur and uncertainties are resolved. Therefore, the amount of contract revenue may increase or decrease from one period to the next. For example: (d) a contractor and a customer may agree variations or claims that increase or decrease contract revenue in a period subsequent to that in which the contract was initially agreed; the amount of revenue agreed in a fixed price contract may increase as a result of cost escalation clauses; the amount of contract revenue may decrease as a result of penalties arising from delays caused by the contractor in the completion of the contract; or when a fixed price contract involves a fixed price per unit of output, contract revenue increases as the number of units is increased. 13 A variation is an instruction by the customer for a change in the scope of the work to be performed under the contract. A variation may lead to an increase or a decrease in contract revenue. Examples of variations are changes in the specifications or design of the asset and changes in the duration of the contract. A variation is included in contract revenue when: it is probable that the customer will approve the variation and the amount of revenue arising from the variation; and the amount of revenue can be reliably measured. 14 A claim is an amount that the contractor seeks to collect from the customer or another party as reimbursement for costs not included in the contract price. A claim may arise from, for example, customer caused delays, errors in specifications or design, and disputed variations in contract work. The measurement of the amounts of revenue arising -409-

7 from claims is subject to a high level of uncertainty and often depends on the outcome of negotiations. Therefore, claims are included in contract revenue only when: negotiations have reached an advanced stage such that it is probable that the customer will accept the claim; and the amount that it is probable will be accepted by the customer can be measured reliably. 15 Incentive payments are additional amounts paid to the contractor if specified performance standards are met or exceeded. For example, a contract may allow for an incentive payment to the contractor for early completion of the contract. Incentive payments are included in contract revenue when: the contract is sufficiently advanced that it is probable that the specified performance standards will be met or exceeded; and the amount of the incentive payment can be measured reliably. Contract costs 16 Contract costs shall comprise: costs that relate directly to the specific contract; costs that are attributable to contract activity in general and can be allocated to the contract; and such other costs as are specifically chargeable to the customer under the terms of the contract. 17 Costs that relate directly to a specific contract include: (d) site labour costs, including site supervision; costs of materials used in construction; depreciation of plant and equipment used on the contract; costs of moving plant, equipment and materials to and from the contract site; -410-

8 (e) (f) (g) (h) costs of hiring plant and equipment; costs of design and technical assistance that is directly related to the contract; the estimated costs of rectification and guarantee work, including expected warranty costs; and claims from third parties. These costs may be reduced by any incidental income that is not included in contract revenue, for example income from the sale of surplus materials and the disposal of plant and equipment at the end of the contract. 18 Costs that may be attributable to contract activity in general and can be allocated to specific contracts include: insurance; costs of design and technical assistance that are not directly related to a specific contract; and construction overheads. Such costs are allocated using methods that are systematic and rational and are applied consistently to all costs having similar characteristics. The allocation is based on the normal level of construction activity. Construction overheads include costs such as the preparation and processing of construction personnel payroll. Costs that may be attributable to contract activity in general and can be allocated to specific contracts also include borrowing costs. 19 Costs that are specifically chargeable to the customer under the terms of the contract may include some general administration costs and development costs for which reimbursement is specified in the terms of the contract. 20 Costs that cannot be attributed to contract activity or cannot be allocated to a contract are excluded from the costs of a construction contract. Such costs include: general administration costs for which reimbursement is not specified in the contract; -411-

9 (d) selling costs; research and development costs for which reimbursement is not specified in the contract; and depreciation of idle plant and equipment that is not used on a particular contract. 21 Contract costs include the costs attributable to a contract for the period from the date of securing the contract to the final completion of the contract. However, costs that relate directly to a contract and are incurred in securing the contract are also included as part of the contract costs if they can be separately identified and measured reliably and it is probable that the contract will be obtained. When costs incurred in securing a contract are recognised as an expense in the period in which they are incurred, they are not included in contract costs when the contract is obtained in a subsequent period. Recognition of contract revenue and expenses 22 When the outcome of a construction contract can be estimated reliably, contract revenue and contract costs associated with the construction contract shall be recognised as revenue and expenses respectively by reference to the stage of completion of the contract activity at the end of the reporting period. An expected loss on the construction contract shall be recognised as an expense immediately in accordance with paragraph In the case of a fixed price contract, the outcome of a construction contract can be estimated reliably when all the following conditions are satisfied: (d) total contract revenue can be measured reliably; it is probable that the economic benefits associated with the contract will flow to the entity; both the contract costs to complete the contract and the stage of contract completion at the end of the reporting period can be measured reliably; and the contract costs attributable to the contract can be clearly identified and measured reliably so that actual contract costs incurred can be compared with prior estimates

10 24 In the case of a cost plus contract, the outcome of a construction contract can be estimated reliably when all the following conditions are satisfied: it is probable that the economic benefits associated with the contract will flow to the entity; and the contract costs attributable to the contract, whether or not specifically reimbursable, can be clearly identified and measured reliably. 25 The recognition of revenue and expenses by reference to the stage of completion of a contract is often referred to as the percentage of completion method. Under this method, contract revenue is matched with the contract costs incurred in reaching the stage of completion, resulting in the reporting of revenue, expenses and profit which can be attributed to the proportion of work completed. This method provides useful information on the extent of contract activity and performance during a period. 26 Under the percentage of completion method, contract revenue is recognised as revenue in profit or loss in the accounting periods in which the work is performed. Contract costs are usually recognised as an expense in profit or loss in the accounting periods in which the work to which they relate is performed. However, any expected excess of total contract costs over total contract revenue for the contract is recognised as an expense immediately in accordance with paragraph A contractor may have incurred contract costs that relate to future activity on the contract. Such contract costs are recognised as an asset provided it is probable that they will be recovered. Such costs represent an amount due from the customer and are often classified as contract work in progress. 28 The outcome of a construction contract can only be estimated reliably when it is probable that the economic benefits associated with the contract will flow to the entity. However, when an uncertainty arises about the collectibility of an amount already included in contract revenue, and already recognised in profit or loss, the uncollectible amount or the amount in respect of which recovery has ceased to be probable is recognised as an expense rather than as an adjustment of the amount of contract revenue

11 29 An entity is generally able to make reliable estimates after it has agreed to a contract which establishes: each party s enforceable rights regarding the asset to be constructed; the consideration to be exchanged; and the manner and terms of settlement. It is also usually necessary for the entity to have an effective internal financial budgeting and reporting system. The entity reviews and, when necessary, revises the estimates of contract revenue and contract costs as the contract progresses. The need for such revisions does not necessarily indicate that the outcome of the contract cannot be estimated reliably. 30 The stage of completion of a contract may be determined in a variety of ways. The entity uses the method that measures reliably the work performed. Depending on the nature of the contract, the methods may include: the proportion that contract costs incurred for work performed to date bear to the estimated total contract costs; surveys of work performed; or completion of a physical proportion of the contract work. Progress payments and advances received from customers often do not reflect the work performed. 31 When the stage of completion is determined by reference to the contract costs incurred to date, only those contract costs that reflect work performed are included in costs incurred to date. Examples of contract costs which are excluded are: contract costs that relate to future activity on the contract, such as costs of materials that have been delivered to a contract site or set aside for use in a contract but not yet installed, used or applied during contract performance, unless the materials have been made especially for the contract; and -414-

12 -415-

13 (e) where the contractor is unable to complete the contract or otherwise meet its obligations under the contract. 35 When the uncertainties that prevented the outcome of the contract being estimated reliably no longer exist, revenue and expenses associated with the construction contract shall be recognised in accordance with paragraph 22 rather than in accordance with paragraph 32. Recognition of expected losses 36 When it is probable that total contract costs will exceed total contract revenue, the expected loss shall be recognised as an expense immediately. 37 The amount of such a loss is determined irrespective of: whether work has commenced on the contract; the stage of completion of contract activity; or the amount of profits expected to arise on other contracts which are not treated as a single construction contract in accordance with paragraph 9. Changes in estimates 38 The percentage of completion method is applied on a cumulative basis in each accounting period to the current estimates of contract revenue and contract costs. Therefore, the effect of a change in the estimate of contract revenue or contract costs, or the effect of a change in the estimate of the outcome of a contract, is accounted for as a change in accounting estimate (see LKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors). The changed estimates are used in the determination of the amount of revenue and expenses recognised in profit or loss in the period in which the change is made and in subsequent periods

14 Disclosure 39 An entity shall disclose: the amount of contract revenue recognised as revenue in the period; the methods used to determine the contract revenue recognised in the period; and the methods used to determine the stage of completion of contracts in progress. 40 An entity shall disclose each of the following for contracts in progress at the end of the reporting period: the aggregate amount of costs incurred and recognised profits (less recognised losses) to date; the amount of advances received; and the amount of retentions. 41 Retentions are amounts of progress billings that are not paid until the satisfaction of conditions specified in the contract for the payment of such amounts or until defects have been rectified. Progress billings are amounts billed for work performed on a contract whether or not they have been paid by the customer. Advances are amounts received by the contractor before the related work is performed. 42 An entity shall present: the gross amount due from customers for contract work as an asset; and the gross amount due to customers for contract work as a liability. 43 The gross amount due from customers for contract work is the net amount of: costs incurred plus recognised profits; less -417-

15 the sum of recognised losses and progress billings for all contracts in progress for which costs incurred plus recognised profits (less recognised losses) exceeds progress billings. 44 The gross amount due to customers for contract work is the net amount of: costs incurred plus recognised profits; less the sum of recognised losses and progress billings for all contracts in progress for which progress billings exceed costs incurred plus recognised profits (less recognised losses). 45 An entity discloses any contingent liabilities and contingent assets in accordance with LKAS 37 Provisions, Contingent Liabilities and Contingent Assets. Contingent liabilities and contingent assets may arise from such items as warranty costs, claims, penalties or possible losses. Effective date 46 This Standard becomes operative for financial statements covering periods beginning on or after 1 January

16 -419-

17 -420-

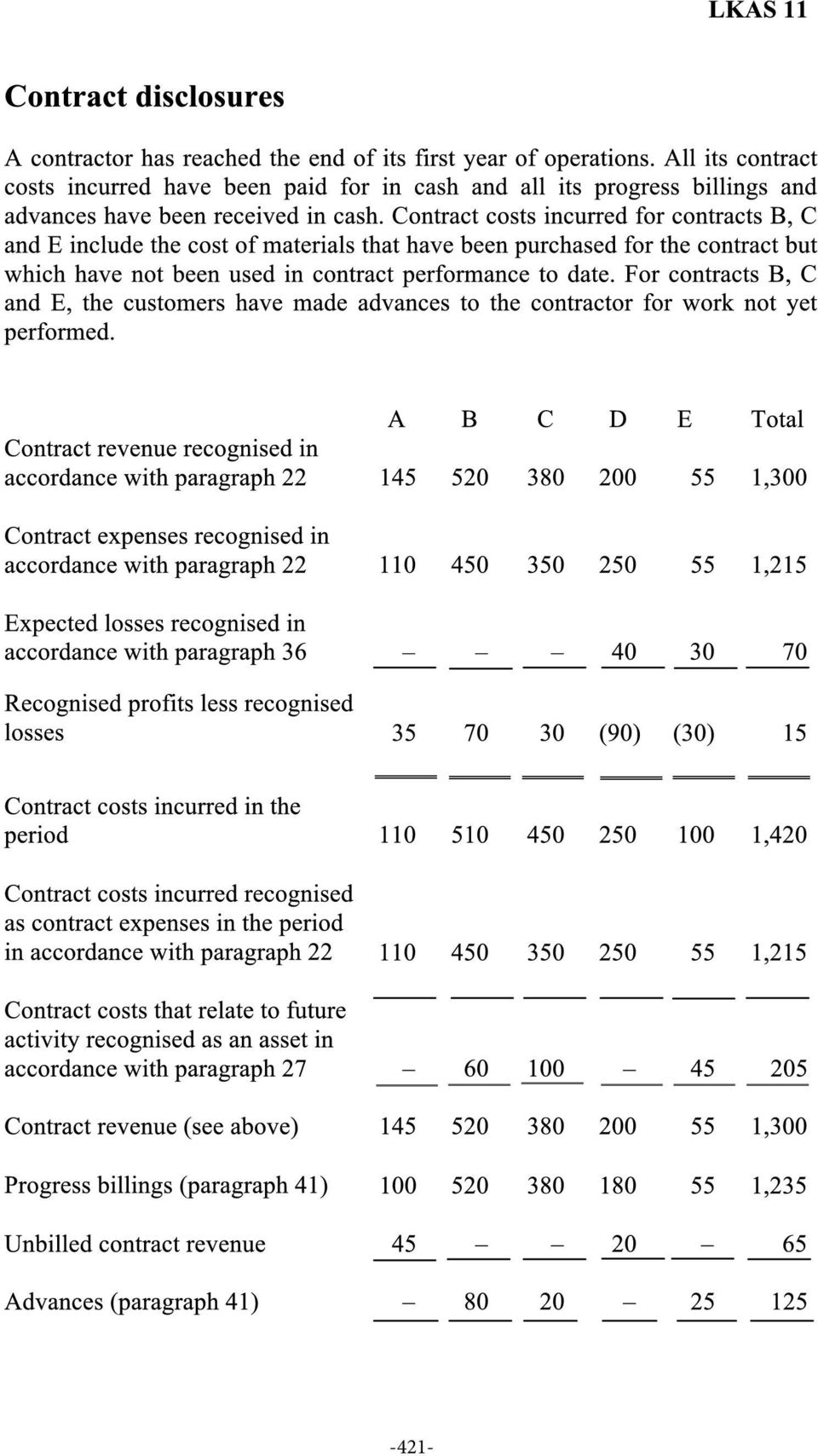

18 -421-

19 -422-

Construction Contracts

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 11 Construction Contracts This version of SB-FRS 11 does not include amendments that are effective for annual periods beginning after 1 January 2015.

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 11 Construction Contracts This version of SB-FRS 11 does not include amendments that are effective for annual periods beginning after 1 January 2015.

International Accounting Standard 11 Construction Contracts

International Accounting Standard 11 Construction Contracts Objective The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with construction contracts.

International Accounting Standard 11 Construction Contracts Objective The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with construction contracts.

NEPAL ACCOUNTING STANDARDS ON CONSTRUCTION CONTRACTS

NAS 13 NEPAL ACCOUNTING STANDARDS ON CONSTRUCTION CONTRACTS CONTENTS Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

NAS 13 NEPAL ACCOUNTING STANDARDS ON CONSTRUCTION CONTRACTS CONTENTS Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

The following Accounting Standards Interpretation (ASI) relates to AS 7. ASI 29 Turnover in case of Contractors

relates to AS 7. ASI 29 Turnover in case of Contractors") 108 Accounting Standard (AS) 7 (revised 2002) Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT

108 Accounting Standard (AS) 7 (revised 2002) Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT

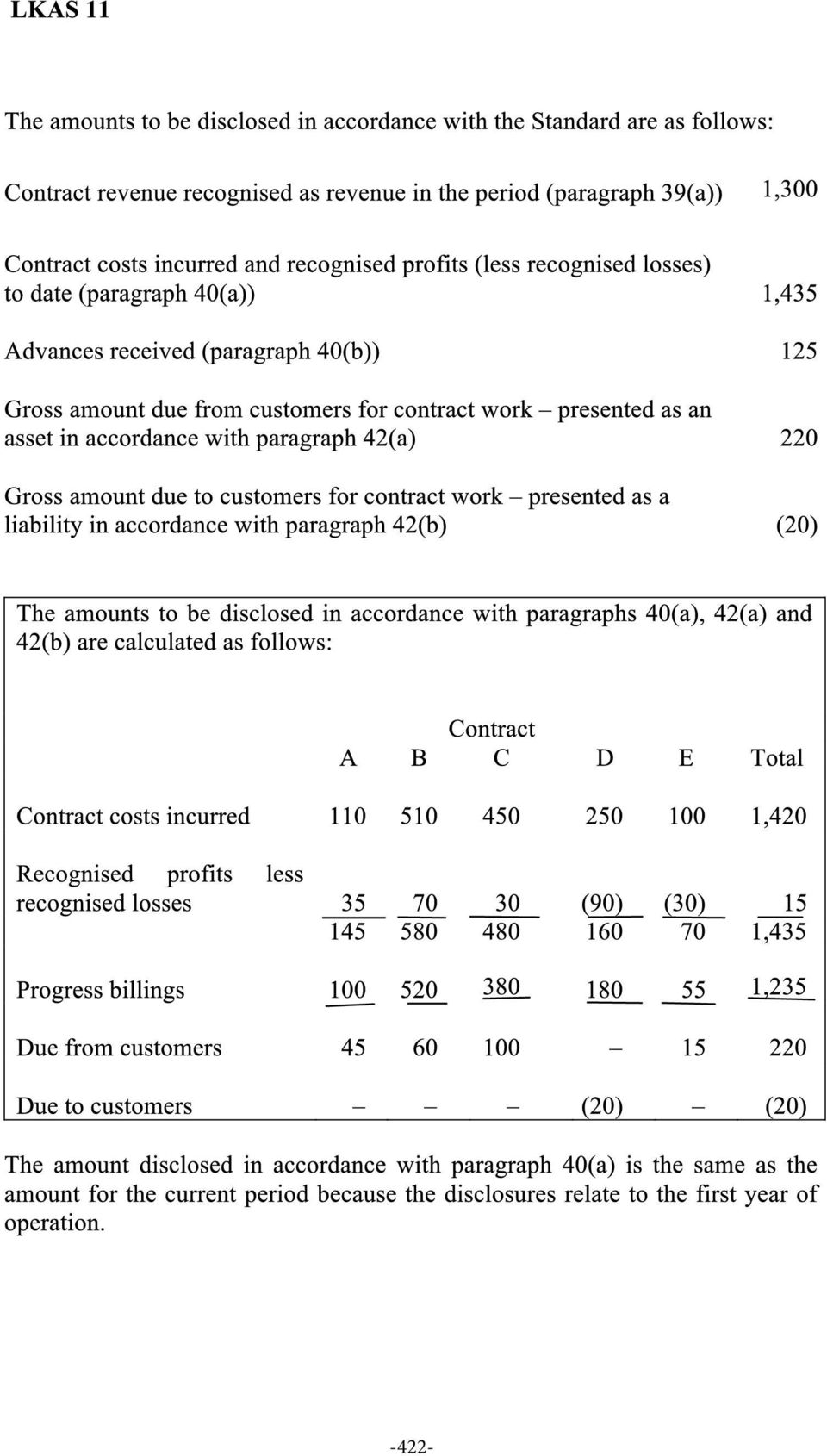

How To Account For Construction Contracts In Hong Kong Kongsong Accounting Standard 11

HKAS 11 Issued October 2004Revised March 2010 Hong Kong Accounting Standard 11 Construction Contracts COPYRIGHT Copyright 2011 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

HKAS 11 Issued October 2004Revised March 2010 Hong Kong Accounting Standard 11 Construction Contracts COPYRIGHT Copyright 2011 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial

Construction Contracts

65 Accounting Standard (AS) 7 Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT COSTS 15-20

65 Accounting Standard (AS) 7 Construction Contracts Contents OBJECTIVE SCOPE Paragraph 1 DEFINITIONS 2-5 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 6-9 CONTRACT REVENUE 10-14 CONTRACT COSTS 15-20

Construction Contracts

Compiled Accounting Standard AASB 111 Construction Contracts This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application

Compiled Accounting Standard AASB 111 Construction Contracts This compiled Standard applies to annual reporting periods beginning on or after 1 January 2009 that end on or after 30 June 2009. Early application

GOVERNMENT OF MALAYSIA

GOVERNMENT OF MALAYSIA Malaysian Public Sector Accounting Standards MPSAS 11 Construction Contracts March 2015 MPSAS 11 Construction Contracts Acknowledgment The Malaysian Public Sector Accounting Standard

GOVERNMENT OF MALAYSIA Malaysian Public Sector Accounting Standards MPSAS 11 Construction Contracts March 2015 MPSAS 11 Construction Contracts Acknowledgment The Malaysian Public Sector Accounting Standard

Applicability / Objective

By Rakesh Agarwal Applicability / Objective APPLICABILITY: applicable to all contracts entered into on or after 1-4-2003 and is mandatory in nature from that date. Based on AS 7 (Construction Contracts)

By Rakesh Agarwal Applicability / Objective APPLICABILITY: applicable to all contracts entered into on or after 1-4-2003 and is mandatory in nature from that date. Based on AS 7 (Construction Contracts)

How To Account For Construction Contracts In Indian Accounting Standard (Indas)

") Contents Indian Accounting Standard (Ind AS) 11 Construction Contracts Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

Contents Indian Accounting Standard (Ind AS) 11 Construction Contracts Paragraphs OBJECTIVE SCOPE 1 2 DEFINITIONS 3 6 COMBINING AND SEGMENTING CONSTRUCTION CONTRACTS 7 10 CONTRACT REVENUE 11 15 CONTRACT

International Financial Reporting. Construction Contracts IAS 11

Construction Contracts IAS 11 2 Construction contract definition Construction Contract is a contract specifically negotiated for the construction of an asset (a building, a bridge) or a combination of

Construction Contracts IAS 11 2 Construction contract definition Construction Contract is a contract specifically negotiated for the construction of an asset (a building, a bridge) or a combination of

19.2 Applicable Terms

19.0 ACCOUNTING FOR CONSTRUCTION CONTRACTS 19.1 Introduction This chapter covers the following: a. Applicable Terms b. Applicable Standard c. Key IPSAS Provisions d. Accounting Documentation e. Accounting

19.0 ACCOUNTING FOR CONSTRUCTION CONTRACTS 19.1 Introduction This chapter covers the following: a. Applicable Terms b. Applicable Standard c. Key IPSAS Provisions d. Accounting Documentation e. Accounting

ACCOUNTING FOR CONSTRUCTION CONTRACT AS7 (Revised-2002) Applied in accounting for construction contracts in the financial statements of contractors.

Applied in accounting for construction contracts in the financial statements of contractors.") ACCOUNTING FOR CONSTRUCTION CONTRACT AS7 (Revised-2002) 1) Applicability of the Standard Applied in accounting for construction contracts in the financial statements of contractors. Where a Construction

ACCOUNTING FOR CONSTRUCTION CONTRACT AS7 (Revised-2002) 1) Applicability of the Standard Applied in accounting for construction contracts in the financial statements of contractors. Where a Construction

1 Supplement: IAS 11 Construction contracts

1 Supplement: IAS 11 Construction contracts Introduction In this section we introduce construction contracts. We will look at the required treatments and disclosures under IAS 11. Make sure that you work

1 Supplement: IAS 11 Construction contracts Introduction In this section we introduce construction contracts. We will look at the required treatments and disclosures under IAS 11. Make sure that you work

International Accounting Standards

International Accounting Standards The Key Issues in IAS 2 and 11 Background In this second of my series on international accounting standards, I have chosen to look at the two standards covering the topic

International Accounting Standards The Key Issues in IAS 2 and 11 Background In this second of my series on international accounting standards, I have chosen to look at the two standards covering the topic

ACCOUNTING FOR CONSTRUCTION IN PROGRESS

ATTACHMENT X GOVERNMENT REGULATION OF THE REPUBLIC OF INDONESIA NUMBER YEAR 00 DATE JUNE 00 GOVERNMENT ACCOUNTING STANDARDS STATEMENT NO.0 ACCOUNTING FOR CONSTRUCTION IN PROGRESS TABLE OF CONTENTS Paragraph

ATTACHMENT X GOVERNMENT REGULATION OF THE REPUBLIC OF INDONESIA NUMBER YEAR 00 DATE JUNE 00 GOVERNMENT ACCOUNTING STANDARDS STATEMENT NO.0 ACCOUNTING FOR CONSTRUCTION IN PROGRESS TABLE OF CONTENTS Paragraph

DRAFT INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS]

![DRAFT INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS]](/thumbs/28/13005002.jpg "DRAFT INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS]") DRAFT INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS] Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes January 2015 Income Computation and Disclosure Standard

DRAFT INCOME COMPUTATION AND DISCLOSURE STANDARDS [ICDS] Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes January 2015 Income Computation and Disclosure Standard

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

![[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]](/thumbs/17/95178.jpg "[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]") [TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) NOTIFICATION

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) (CENTRAL BOARD OF DIRECT TAXES) NOTIFICATION

23 Construction contracts/ Long term WIP IAS 11

23 Construction contracts/ Long term WIP IAS 11 A Key points Construction contract assets are often material amounts in balance sheets. Changes in valuation of work in progress (WIP) have a direct profit

23 Construction contracts/ Long term WIP IAS 11 A Key points Construction contract assets are often material amounts in balance sheets. Changes in valuation of work in progress (WIP) have a direct profit

CONCEPTUAL AND ACCOUNTING ASPECTS RELATING CONSTRUCTION CONTRACTS IN PUBLIC ENTITIES

CONCEPTUAL AND ACCOUNTING ASPECTS RELATING CONSTRUCTION CONTRACTS IN PUBLIC ENTITIES Ţenovici Cristina Otilia Ph D Lecturer Constantin Brâncoveanu University, Piteşti, F.M.M.A.E. Rm. Vâlcea cristina.tenovici@gmail.com

CONCEPTUAL AND ACCOUNTING ASPECTS RELATING CONSTRUCTION CONTRACTS IN PUBLIC ENTITIES Ţenovici Cristina Otilia Ph D Lecturer Constantin Brâncoveanu University, Piteşti, F.M.M.A.E. Rm. Vâlcea cristina.tenovici@gmail.com

Sri Lanka Accounting Standard LKAS 17. Leases

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 3 DEFINITIONS 4 6 CLASSIFICATION OF LEASES 7 19 LEASES IN THE FINANCIAL

Sri Lanka Accounting Standard LKAS 17 Leases CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 17 LEASES paragraphs OBJECTIVE 1 SCOPE 2 3 DEFINITIONS 4 6 CLASSIFICATION OF LEASES 7 19 LEASES IN THE FINANCIAL

International Accounting Standard 17 Leases

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

International Accounting Standard 17 Leases Objective 1 The objective of this Standard is to prescribe, for lessees and lessors, the appropriate accounting policies and disclosure to apply in relation

Sri Lanka Accounting Standard LKAS 28. Investments in Associates

Sri Lanka Accounting Standard LKAS 28 Investments in Associates CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 28 INVESTMENTS IN ASSOCIATES paragraphs SCOPE 1 DEFINITIONS 2 12 Significant influence 6 10 Equity

Sri Lanka Accounting Standard LKAS 28 Investments in Associates CONTENTS SRI LANKA ACCOUNTING STANDARD LKAS 28 INVESTMENTS IN ASSOCIATES paragraphs SCOPE 1 DEFINITIONS 2 12 Significant influence 6 10 Equity

INLAND REVENUE BOARD MALAYSIA CONSTRUCTION CONTRACTS

INLAND REVENUE BOARD MALAYSIA CONSTRUCTION CONTRACTS PUBLIC RULING NO. 2/2009 Translation from the original Bahasa Malaysia text DATE OF ISSUE : 22 MAY 2009 CONSTRUCTION CONTRACTS INLAND REVENUE BOARD

INLAND REVENUE BOARD MALAYSIA CONSTRUCTION CONTRACTS PUBLIC RULING NO. 2/2009 Translation from the original Bahasa Malaysia text DATE OF ISSUE : 22 MAY 2009 CONSTRUCTION CONTRACTS INLAND REVENUE BOARD

DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 111: CONSTRUCTION CONTRACTS

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 111: CONSTRUCTION CONTRACTS Prepared by: Joint Tax Working Group on FRS Date

The Malaysian Institute of Certified Public Accountants DISCUSSION PAPER TAX IMPLICATIONS RELATED TO THE IMPLEMENTATION OF FRS 111: CONSTRUCTION CONTRACTS Prepared by: Joint Tax Working Group on FRS Date

Sri Lanka Accounting Standard LKAS 12. Income Taxes

Sri Lanka Accounting Standard LKAS 12 Income Taxes CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 12 INCOME TAXES OBJECTIVE SCOPE 1 4 DEFINITIONS 5 11 Tax base 7 11 RECOGNITION OF CURRENT TAX LIABILITIES

Sri Lanka Accounting Standard LKAS 12 Income Taxes CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 12 INCOME TAXES OBJECTIVE SCOPE 1 4 DEFINITIONS 5 11 Tax base 7 11 RECOGNITION OF CURRENT TAX LIABILITIES

HKAS 17 Revised July 2012February 2014. Hong Kong Accounting Standard 17. Leases

HKAS 17 Revised July 2012February 2014 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting Standard

HKAS 17 Revised July 2012February 2014 Hong Kong Accounting Standard 17 Leases HKAS 17 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting Standard

Impacts on the construction industry of the new revenue standard

IFRS Impacts on the construction industry of the new revenue standard September 2014 kpmg.com/ifrs Contents The devil is in the detail 1 1 Critical judgements at contract inception 2 1.1 Pre-contract costs

IFRS Impacts on the construction industry of the new revenue standard September 2014 kpmg.com/ifrs Contents The devil is in the detail 1 1 Critical judgements at contract inception 2 1.1 Pre-contract costs

Sri Lanka Accounting Standard LKAS 16. Property, Plant and Equipment

Sri Lanka Accounting Standard LKAS 16 Property, Plant and Equipment CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 16 PROPERTY, PLANT AND EQUIPMENT OBJECTIVE 1 SCOPE 2 DEFINITIONS 6 RECOGNITION

Sri Lanka Accounting Standard LKAS 16 Property, Plant and Equipment CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 16 PROPERTY, PLANT AND EQUIPMENT OBJECTIVE 1 SCOPE 2 DEFINITIONS 6 RECOGNITION

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 11, 2014 What s inside: Overview... 1 Defining the contract...

Revenue from contracts with customers The standard is final A comprehensive look at the new revenue model No. US2014-01 (supplement) June 11, 2014 What s inside: Overview... 1 Defining the contract...

Sri Lanka Accounting Standard-LKAS 27. Consolidated and Separate Financial Statements

Sri Lanka Accounting Standard-LKAS 27 Consolidated and Separate Financial Statements -675- Sri Lanka Accounting Standard-LKAS 27 Consolidated and Separate Financial Statements Sri Lanka Accounting Standard

Sri Lanka Accounting Standard-LKAS 27 Consolidated and Separate Financial Statements -675- Sri Lanka Accounting Standard-LKAS 27 Consolidated and Separate Financial Statements Sri Lanka Accounting Standard

Property, Plant and Equipment

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

Provisions, Contingent Liabilities and Contingent Assets

HKAS 37 Issued November 2004 Revised March 2010 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

HKAS 37 Issued November 2004 Revised March 2010 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement

International Accounting Standard 37 Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17)

") New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments up to October 2010 This Standard was issued by the Financial Reporting

New Zealand Equivalent to International Accounting Standard 17 Leases (NZ IAS 17) Issued November 2004 and incorporates amendments up to October 2010 This Standard was issued by the Financial Reporting

IPSAS 13 LEASES Acknowledgment

IPSAS 13 LEASES Acknowledgment This International Public Sector Accounting Standard is drawn primarily from International Accounting Standard (IAS) 17 (revised 2003), Leases published by the International

IPSAS 13 LEASES Acknowledgment This International Public Sector Accounting Standard is drawn primarily from International Accounting Standard (IAS) 17 (revised 2003), Leases published by the International

IPSAS 13 LEASES Acknowledgment

IPSAS 13 LEASES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 17 (Revised 2003), Leases, published by the International

IPSAS 13 LEASES Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 17 (Revised 2003), Leases, published by the International

Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

September 2014 Aerospace & Defense Spotlight The Converged Revenue Recognition Model Has Landed In This Issue: Background Key Accounting Issues Effective Date and Transition Challenges for A&D Entities

How To Account For Property, Plant And Equipment

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

International Accounting Standard 16 Property, Plant and Equipment Objective 1 The objective of this Standard is to prescribe the accounting treatment for property, plant and equipment so that users of

Income Taxes STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD

STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD Income Taxes This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective for annual periods beginning

STATUTORY BOARD SB-FRS 12 FINANCIAL REPORTING STANDARD Income Taxes This version of the Statutory Board Financial Reporting Standard does not include amendments that are effective for annual periods beginning

CLASSIFICATION OF LEASES

284 Accounting Standard (AS) 19 Leases Contents OBJECTIVE SCOPE Paragraphs 1-2 DEFINITIONS 3-4 CLASSIFICATION OF LEASES 5-10 LEASES IN THE FINANCIAL STATEMENTS OF LESSEES 11-25 Finance Leases 11-22 Operating

284 Accounting Standard (AS) 19 Leases Contents OBJECTIVE SCOPE Paragraphs 1-2 DEFINITIONS 3-4 CLASSIFICATION OF LEASES 5-10 LEASES IN THE FINANCIAL STATEMENTS OF LESSEES 11-25 Finance Leases 11-22 Operating

HKAS 36 Revised June November 2014. Hong Kong Accounting Standard 36. Impairment of Assets

HKAS 36 Revised June November 2014 Hong Kong Accounting Standard 36 Impairment of Assets HKAS 36 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

HKAS 36 Revised June November 2014 Hong Kong Accounting Standard 36 Impairment of Assets HKAS 36 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting

Statement of Financial Accounting Standards No. 13

Statement of Financial Accounting Standards No. 13 FAS13 Status Page FAS13 Summary Accounting for Leases November 1976 Financial Accounting Standards Board of the Financial Accounting Foundation 401 MERRITT

Statement of Financial Accounting Standards No. 13 FAS13 Status Page FAS13 Summary Accounting for Leases November 1976 Financial Accounting Standards Board of the Financial Accounting Foundation 401 MERRITT

Indian Accounting Standard (Ind AS) 115, Revenue from Contracts with Customers

115, Revenue from Contracts with Customers") Indian Accounting Standard (Ind AS) 115, Revenue from Contracts with Customers (The Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs

Indian Accounting Standard (Ind AS) 115, Revenue from Contracts with Customers (The Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs

Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard

SME-FRF & SME-FRS Issued August 2005Revised February 2011 Effective for a Qualifying Entity s financial statements that cover a period beginning on or after 1 January 2005 Effective for a Qualifying Entity's

SME-FRF & SME-FRS Issued August 2005Revised February 2011 Effective for a Qualifying Entity s financial statements that cover a period beginning on or after 1 January 2005 Effective for a Qualifying Entity's

Sri Lanka Accounting Standard-LKAS 7. Statement of Cash Flows

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Sri Lanka Accounting Standard-LKAS 7 Statement of Cash Flows CONTENTS SRI LANKA ACCOUNTING STANDARD-LKAS 7 STATEMENT OF CASH FLOWS paragraphs OBJECTIVE SCOPE 1 3 BENEFITS OF CASH FLOW INFORMATION 4 5 DEFINITIONS

Accounting for Real Estate Developers. Presented by: CA. Sandeep Shah Partner N A Shah Associates

Accounting for Real Estate Developers Presented by: CA. Sandeep Shah Partner N A Shah Associates 1 Contents Background Accounting under Indian GAAP Accounting under IFRS Exposure draft-revenue from Contracts

Accounting for Real Estate Developers Presented by: CA. Sandeep Shah Partner N A Shah Associates 1 Contents Background Accounting under Indian GAAP Accounting under IFRS Exposure draft-revenue from Contracts

EUROPEAN UNION ACCOUNTING RULE 6 INTANGIBLE ASSETS

EUROPEAN UNION ACCOUNTING RULE 6 INTANGIBLE ASSETS Page 2 of 17 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of intangible assets... 4 5. Recognition and Measurement... 5

EUROPEAN UNION ACCOUNTING RULE 6 INTANGIBLE ASSETS Page 2 of 17 I N D E X 1. Objective... 3 2. Scope... 3 3. Definitions... 3 4. Definition of intangible assets... 4 5. Recognition and Measurement... 5

HKAS 12 Revised May November 2014. Hong Kong Accounting Standard 12. Income Taxes

HKAS 12 Revised May November 2014 Hong Kong Accounting Standard 12 Income Taxes HKAS 12 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting Standard

HKAS 12 Revised May November 2014 Hong Kong Accounting Standard 12 Income Taxes HKAS 12 COPYRIGHT Copyright 2014 Hong Kong Institute of Certified Public Accountants This Hong Kong Financial Reporting Standard

technical factsheet 185 Stock and work in progress

technical factsheet 185 Stock and work in progress CONTENTS Page 1 Introduction 1 2 Legislative requirement 1 3 Accounting standards 3 4 Examples 6 5 Checklist 7 6 Sources of information 9 This technical

technical factsheet 185 Stock and work in progress CONTENTS Page 1 Introduction 1 2 Legislative requirement 1 3 Accounting standards 3 4 Examples 6 5 Checklist 7 6 Sources of information 9 This technical

Impairment of Assets

Compiled AASB Standard AASB 136 Impairment of Assets This compiled Standard applies to annual reporting periods beginning on or after 1 January 2010. Early application is permitted. It incorporates relevant

Compiled AASB Standard AASB 136 Impairment of Assets This compiled Standard applies to annual reporting periods beginning on or after 1 January 2010. Early application is permitted. It incorporates relevant

Customer Loyalty Programmes

INTERPRETATION OF STATUTORY BOARD FINANCIAL REPORTING STANDARD INT SB-FRS 113 Customer Loyalty Programmes This version of INT SB-FRS 113 does not include amendments that are effective for annual periods

INTERPRETATION OF STATUTORY BOARD FINANCIAL REPORTING STANDARD INT SB-FRS 113 Customer Loyalty Programmes This version of INT SB-FRS 113 does not include amendments that are effective for annual periods

7 Contract Costing. Basic Concepts. Contract Costing

7 Contract Costing Basic Concepts Contract Costing Sub-contract Extra work Work Certified Value of Work Certified Cost of work certified Work uncertified Progress Payment Contract costing is a form of

7 Contract Costing Basic Concepts Contract Costing Sub-contract Extra work Work Certified Value of Work Certified Cost of work certified Work uncertified Progress Payment Contract costing is a form of

STANDARD FINANCIAL REPORTING P ROVISIONS, C ONTINGENT L IABILITIES AND C ONTINGENT A SSETS ACCOUNTING STANDARDS BOARD

ACCOUNTING STANDARDS BOARD SEPTEMBER 1998 FRS 12 12 P ROVISIONS, FINANCIAL REPORTING STANDARD C ONTINGENT L IABILITIES AND C ONTINGENT A SSETS ACCOUNTING STANDARDS BOARD Financial Reporting Standard 12

ACCOUNTING STANDARDS BOARD SEPTEMBER 1998 FRS 12 12 P ROVISIONS, FINANCIAL REPORTING STANDARD C ONTINGENT L IABILITIES AND C ONTINGENT A SSETS ACCOUNTING STANDARDS BOARD Financial Reporting Standard 12

CHAPTER 11 U.S. GAAP AND INTERNATIONAL ACCOUNTING STANDARDS

CHAPTER 11 U.S. GAAP AND INTERNATIONAL ACCOUNTING STANDARDS CONTENTS Introduction 11.02 Accounting Sources for Construction Contractors 11.03 U.S. GAAP 11.03 IFRS 11.04 Problems with U.S. GAAP for Contractors

CHAPTER 11 U.S. GAAP AND INTERNATIONAL ACCOUNTING STANDARDS CONTENTS Introduction 11.02 Accounting Sources for Construction Contractors 11.03 U.S. GAAP 11.03 IFRS 11.04 Problems with U.S. GAAP for Contractors

NEPAL ACCOUNTING STANDARDS ON INVENTORIES CONTENTS Paragraphs

NAS 04 NEPAL ACCOUNTING STANDARDS ON INVENTORIES CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9-32 Cost of inventories 10-21 Costs of purchase 11 Costs of conversion

NAS 04 NEPAL ACCOUNTING STANDARDS ON INVENTORIES CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9-32 Cost of inventories 10-21 Costs of purchase 11 Costs of conversion

ACCOUNTING FOR LEASES AND HIRE PURCHASE CONTRACTS

Issued 07/85 Revised 06/90 New Zealand Society of Accountants STATEMENT OF STANDARD ACCOUNTING PRACTICE NO. 18 Revised 1990 ACCOUNTING FOR LEASES AND HIRE PURCHASE CONTRACTS Issued by the Council, New

Issued 07/85 Revised 06/90 New Zealand Society of Accountants STATEMENT OF STANDARD ACCOUNTING PRACTICE NO. 18 Revised 1990 ACCOUNTING FOR LEASES AND HIRE PURCHASE CONTRACTS Issued by the Council, New

Terms and Conditions of Offer and Contract (Works & Services) Conditions of Offer

Conditions of Offer") Conditions of Offer A1 The offer documents comprise the offer form, letter of invitation to offer (if any), these Conditions of Offer and Conditions of Contract (Works & Services), the Working with Queensland

Conditions of Offer A1 The offer documents comprise the offer form, letter of invitation to offer (if any), these Conditions of Offer and Conditions of Contract (Works & Services), the Working with Queensland

Investments in Associates and Joint Ventures

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 28 Investments in Associates and Joint Ventures This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 28 Investments in Associates and Joint Ventures This standard applies for annual periods beginning on or after 1 January 2013. Earlier application is

Statutory Financial Reporting Policy

Statutory Financial Reporting Policy Reference Number: 3.15 12/270185 Type: Council Category: Corporate Services Relevant Community Plan Outcome: Demonstrate effective leadership with strong community

Statutory Financial Reporting Policy Reference Number: 3.15 12/270185 Type: Council Category: Corporate Services Relevant Community Plan Outcome: Demonstrate effective leadership with strong community

Stripping Costs in the Production Phase of a Surface Mine

INTERPRETATION OF STATUTORY BOARD FINANCIAL REPORTING STANDARD INT SB-FRS 120 Stripping Costs in the Production Phase of a Surface Mine This version of INT SB-FRS 120 does not include amendments that are

INTERPRETATION OF STATUTORY BOARD FINANCIAL REPORTING STANDARD INT SB-FRS 120 Stripping Costs in the Production Phase of a Surface Mine This version of INT SB-FRS 120 does not include amendments that are

Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards

July 2014 Financial Reporting Center Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards In May 2014, FASB issued Accounting Standards Update (ASU) 2014-09, Revenue

July 2014 Financial Reporting Center Financial Reporting Brief: Roadmap to Understanding the New Revenue Recognition Standards In May 2014, FASB issued Accounting Standards Update (ASU) 2014-09, Revenue

NEPAL ACCOUNTING STANDARDS ON INVESTMENT IN ASSOCIATES

NAS 25 NEPAL ACCOUNTING STANDARDS ON INVESTMENT IN ASSOCIATES CONTENTS Paragraphs SCOPE 1-2 DEFINITIONS 3-13 Significant influence 7-11 Equity method 12-13 APPLICATION OF THE EQUITY METHOD 14-33 Impairment

NAS 25 NEPAL ACCOUNTING STANDARDS ON INVESTMENT IN ASSOCIATES CONTENTS Paragraphs SCOPE 1-2 DEFINITIONS 3-13 Significant influence 7-11 Equity method 12-13 APPLICATION OF THE EQUITY METHOD 14-33 Impairment

Indian Accounting Standard (Ind AS) 2 Inventories. Cost of agricultural produce harvested from biological assets 20

2 Inventories. Cost of agricultural produce harvested from biological assets 20") Contents OBJECTIVE Indian Accounting Standard (Ind AS) 2 Inventories Paragraphs 1 SCOPE 2-5 DEFINITIONS 6-8 MEASUREMENT OF INVENTORIES Cost of inventories 10-22 Costs of purchase Costs of conversion Other

Contents OBJECTIVE Indian Accounting Standard (Ind AS) 2 Inventories Paragraphs 1 SCOPE 2-5 DEFINITIONS 6-8 MEASUREMENT OF INVENTORIES Cost of inventories 10-22 Costs of purchase Costs of conversion Other

NAS 09 NEPAL ACCOUNTING STANDARDS ON INCOME TAXES

NAS 09 NEPAL ACCOUNTING STANDARDS ON INCOME TAXES CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 DEFINITIONS 5-11 Tax Base 7-11 RECOGNITION OF CURRENT TAX LIABILITIES AND CURRENT TAX ASSETS 12-14 RECOGNITION

NAS 09 NEPAL ACCOUNTING STANDARDS ON INCOME TAXES CONTENTS Paragraphs OBJECTIVE SCOPE 1-4 DEFINITIONS 5-11 Tax Base 7-11 RECOGNITION OF CURRENT TAX LIABILITIES AND CURRENT TAX ASSETS 12-14 RECOGNITION

Contingencies and Events Occurring After the Balance Sheet Date

40 Accounting Standard (AS) 4 Contingencies and Events Occurring After the Balance Sheet Date Contents INTRODUCTION Paragraphs 1-3 Definitions 3 EXPLANATION 4-9 Contingencies 4-7 Accounting Treatment of

40 Accounting Standard (AS) 4 Contingencies and Events Occurring After the Balance Sheet Date Contents INTRODUCTION Paragraphs 1-3 Definitions 3 EXPLANATION 4-9 Contingencies 4-7 Accounting Treatment of

International Accounting Standard 36 Impairment of Assets

International Accounting Standard 36 Impairment of Assets Objective 1 The objective of this Standard is to prescribe the procedures that an entity applies to ensure that its assets are carried at no more

International Accounting Standard 36 Impairment of Assets Objective 1 The objective of this Standard is to prescribe the procedures that an entity applies to ensure that its assets are carried at no more

New on the Horizon: Revenue recognition for building and construction

NOVEMBER 2011 Building & Construction New on the Horizon: Revenue recognition for building and construction KPMG s Building & Construction practice KPMG s Building & Construction practice provides integrated

NOVEMBER 2011 Building & Construction New on the Horizon: Revenue recognition for building and construction KPMG s Building & Construction practice KPMG s Building & Construction practice provides integrated

International Accounting Standard 2 Inventories

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

International Accounting Standard 2 Inventories Objective 1 The objective of this Standard is to prescribe the accounting treatment for inventories. A primary issue in accounting for inventories is the

IFRS 15: an overview of the new principles of revenue recognition

IFRS 15: an overview of the new principles of revenue recognition December 2014 I n May 2014, the IASB published IFRS 15, Revenue from Contracts with Customers. Simultaneously, the FASB published ASU 2014-09

IFRS 15: an overview of the new principles of revenue recognition December 2014 I n May 2014, the IASB published IFRS 15, Revenue from Contracts with Customers. Simultaneously, the FASB published ASU 2014-09

NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

NAS 21 NEPAL ACCOUNTING STANDARDS ON BUSINESS COMBINATIONS CONTENTS Paragraphs OBJECTIVE 1 SCOPE 2-14 Identifying a business combination 5-10 Business combinations involving entities under common control

New aspects of revenues and expenses accounting for construction contracts

New aspects of revenues and expenses accounting for construction contracts Lilia Grigoroi The Academy of Economics Studies of Moldova, Accounting and Audit Department email: lilia@grigoroi.com Angela Popovici

New aspects of revenues and expenses accounting for construction contracts Lilia Grigoroi The Academy of Economics Studies of Moldova, Accounting and Audit Department email: lilia@grigoroi.com Angela Popovici

International Accounting Standard 12 Income Taxes. Objective. Scope. Definitions IAS 12

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the accounting treatment for income taxes. The principal issue in accounting for income taxes

Investments in Associates

Indian Accounting Standard (Ind AS) 28 Investments in Associates Investments in Associates Contents Paragraphs SCOPE 1 DEFINITIONS 2-12 Significant Influence 6-10 Equity Method 11-12 APPLICATION OF THE

Indian Accounting Standard (Ind AS) 28 Investments in Associates Investments in Associates Contents Paragraphs SCOPE 1 DEFINITIONS 2-12 Significant Influence 6-10 Equity Method 11-12 APPLICATION OF THE

Investments in Associates and Joint Ventures

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

International Accounting Standard 28 Investments in Associates and Joint Ventures In April 2001 the International Accounting Standards Board (IASB) adopted IAS 28 Accounting for Investments in Associates,

Stripping Costs in the Production Phase of a Surface Mine

IFRIC Interpretation 20 Stripping Costs in the Production Phase of a Surface Mine In October 2011 the International Accounting Standards Board issued IFRIC 20 Stripping Costs in the Production Phase of

IFRIC Interpretation 20 Stripping Costs in the Production Phase of a Surface Mine In October 2011 the International Accounting Standards Board issued IFRIC 20 Stripping Costs in the Production Phase of

Leases (Topic 840) Proposed Accounting Standards Update. Issued: August 17, 2010 Comments Due: December 15, 2010

Proposed Accounting Standards Update. Issued: August 17, 2010 Comments Due: December 15, 2010") Proposed Accounting Standards Update Issued: August 17, 2010 Comments Due: December 15, 2010 Leases (Topic 840) This Exposure Draft of a proposed Accounting Standards Update of Topic 840 is issued by the

Proposed Accounting Standards Update Issued: August 17, 2010 Comments Due: December 15, 2010 Leases (Topic 840) This Exposure Draft of a proposed Accounting Standards Update of Topic 840 is issued by the

Tender forms and letters 1. Final accounts 7 Cost items 7 Presenting the final account 9. Retention and defects liability period 11.

Contents Tender forms and letters 1 Final accounts 7 Cost items 7 Presenting the final account 9 Retention and defects liability period 11 Summary 14 Tender forms and letters Often clients/architects require

Contents Tender forms and letters 1 Final accounts 7 Cost items 7 Presenting the final account 9 Retention and defects liability period 11 Summary 14 Tender forms and letters Often clients/architects require

Financial Instruments: Recognition and Measurement

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

IFRS 15 Revenue from Contracts with Customers

May 2014 International Financial Reporting Standard IFRS 15 Revenue from Contracts with Customers International Financial Reporting Standard 15 Revenue from Contracts with Customers IFRS 15 Revenue from

May 2014 International Financial Reporting Standard IFRS 15 Revenue from Contracts with Customers International Financial Reporting Standard 15 Revenue from Contracts with Customers IFRS 15 Revenue from

(b) financial instruments (Ind AS 32, Financial Instruments: Presentation and Ind AS 109, Financial Instruments and ); and

financial instruments (Ind AS 32, Financial Instruments: Presentation and Ind AS 109, Financial Instruments and ); and") Indian Accounting Standard (Ind AS) 2 Inventories (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold italic type indicate

Indian Accounting Standard (Ind AS) 2 Inventories (This Indian Accounting Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold italic type indicate

New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12)

") New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12) Issued November 2004 and incorporates amendments up to and including 31 October 2010 other than consequential amendments

New Zealand Equivalent to International Accounting Standard 12 Income Taxes (NZ IAS 12) Issued November 2004 and incorporates amendments up to and including 31 October 2010 other than consequential amendments

International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations

EC staff consolidated version as of 21/06/2012, FOR INFORMATION PURPOSES ONLY EN IFRS 5 International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations Objective

EC staff consolidated version as of 21/06/2012, FOR INFORMATION PURPOSES ONLY EN IFRS 5 International Financial Reporting Standard 5 Non-current Assets Held for Sale and Discontinued Operations Objective

Revenue Recognition (Topic 605)

") Proposed Accounting Standards Update (Revised) Issued: November 14, 2011 and January 4, 2012 Comments Due: March 13, 2012 Revenue Recognition (Topic 605) Revenue from Contracts with Customers (including

Proposed Accounting Standards Update (Revised) Issued: November 14, 2011 and January 4, 2012 Comments Due: March 13, 2012 Revenue Recognition (Topic 605) Revenue from Contracts with Customers (including

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS. Year ended December 31, 2011

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS Year ended SAMPLE MANUFACTURING COMPANY LIMITED CONSOLIDATED FINANCIAL STATEMENTS For the year ended The information contained in

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE AGREEMENTS FOR THE CONSTRUCTION OF ASSETS FROM EXCHANGE TRANSACTIONS (IGRAP 8) Issued by the Accounting

ACCOUNTING STANDARDS BOARD INTERPRETATION OF THE STANDARDS OF GENERALLY RECOGNISED ACCOUNTING PRACTICE AGREEMENTS FOR THE CONSTRUCTION OF ASSETS FROM EXCHANGE TRANSACTIONS (IGRAP 8) Issued by the Accounting

International Accounting Standard 12 Income Taxes

EC staff consolidated version as of 21 June 2012, EN IAS 12 FOR INFORMATION PURPOSES ONLY International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the

EC staff consolidated version as of 21 June 2012, EN IAS 12 FOR INFORMATION PURPOSES ONLY International Accounting Standard 12 Income Taxes Objective The objective of this Standard is to prescribe the

International Accounting Standard 19 Employee Benefits

International Accounting Standard 19 Employee Benefits Objective The objective of this Standard is to prescribe the accounting and disclosure for employee benefits. The Standard requires an entity to recognise:

International Accounting Standard 19 Employee Benefits Objective The objective of this Standard is to prescribe the accounting and disclosure for employee benefits. The Standard requires an entity to recognise:

The consolidated financial statements of

Our 2014 financial statements The consolidated financial statements of plc and its subsidiaries (the Group) for the year ended 31 December 2014 have been prepared in accordance with International Financial

Our 2014 financial statements The consolidated financial statements of plc and its subsidiaries (the Group) for the year ended 31 December 2014 have been prepared in accordance with International Financial

Asset Protection Agreement Templates - Customer Explanatory Notes. Explanatory Notes on Asset Protection Agreement

Asset Protection Agreement Templates - Customer Explanatory Notes Explanatory Notes on Asset Protection Agreement Clause Heading Background The Asset Protection Agreement is intended for use where the

Asset Protection Agreement Templates - Customer Explanatory Notes Explanatory Notes on Asset Protection Agreement Clause Heading Background The Asset Protection Agreement is intended for use where the

Obtaining a Copy of this Interpretation

Obtaining a Copy of this Interpretation This Interpretation is available on the AASB website: www.aasb.gov.au. Alternatively, printed copies of this Interpretation are available for purchase by contacting:

Obtaining a Copy of this Interpretation This Interpretation is available on the AASB website: www.aasb.gov.au. Alternatively, printed copies of this Interpretation are available for purchase by contacting:

International Accounting Standard 20 Accounting for Government Grants and Disclosure of Government Assistance 1

International Accounting Standard 20 Accounting for Government Grants and Disclosure of Government Assistance 1 Scope 1 This Standard shall be applied in accounting for, and in the disclosure of, government

International Accounting Standard 20 Accounting for Government Grants and Disclosure of Government Assistance 1 Scope 1 This Standard shall be applied in accounting for, and in the disclosure of, government

Statement of Financial Accounting Standards No. 144

Statement of Financial Accounting Standards No. 144 FAS144 Status Page FAS144 Summary Accounting for the Impairment or Disposal of Long-Lived Assets August 2001 Financial Accounting Standards Board of

Statement of Financial Accounting Standards No. 144 FAS144 Status Page FAS144 Summary Accounting for the Impairment or Disposal of Long-Lived Assets August 2001 Financial Accounting Standards Board of

SIGNIFICANT GROUP ACCOUNTING POLICIES

SIGNIFICANT GROUP ACCOUNTING POLICIES Basis of consolidation Subsidiaries Subsidiaries are all entities over which the Group has the sole right to exercise control over the operations and govern the financial

SIGNIFICANT GROUP ACCOUNTING POLICIES Basis of consolidation Subsidiaries Subsidiaries are all entities over which the Group has the sole right to exercise control over the operations and govern the financial

Sri Lanka Accounting Standard-LKAS 19. Employee Benefits

Sri Lanka Accounting Standard-LKAS 19 Employee Benefits CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 19 EMPLOYEE BENEFITS OBJECTIVE SCOPE 1 6 DEFINITIONS 7 SHORT-TERM EMPLOYEE BENEFITS 8 23 Recognition

Sri Lanka Accounting Standard-LKAS 19 Employee Benefits CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD-LKAS 19 EMPLOYEE BENEFITS OBJECTIVE SCOPE 1 6 DEFINITIONS 7 SHORT-TERM EMPLOYEE BENEFITS 8 23 Recognition

Property, Plant and Equipment

Compiled AASB Standard AASB 116 Property, Plant and Equipment This compiled Standard applies to annual reporting periods beginning on or after 1 July 2009. Early application is permitted. It incorporates

Compiled AASB Standard AASB 116 Property, Plant and Equipment This compiled Standard applies to annual reporting periods beginning on or after 1 July 2009. Early application is permitted. It incorporates

Sri Lanka Accounting Standard-LKAS 26. Accounting and Reporting by Retirement Benefit Plans

Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans -661- Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans Sri Lanka Accounting

Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans -661- Sri Lanka Accounting Standard-LKAS 26 Accounting and Reporting by Retirement Benefit Plans Sri Lanka Accounting

How To Account For Events After The Balance Sheet Date

NAS 05 NEPAL ACCOUNTING STANDARDS ON EVENTS AFTER THE BALANCE SHEET DATE CONTENTS Paragraphs OBJECTIVE SCOPE 1-2 DEFINITIONS 3-7 RECOGNITION AND MEASUREMENT 8-13 Adjusting events after the balance sheet

NAS 05 NEPAL ACCOUNTING STANDARDS ON EVENTS AFTER THE BALANCE SHEET DATE CONTENTS Paragraphs OBJECTIVE SCOPE 1-2 DEFINITIONS 3-7 RECOGNITION AND MEASUREMENT 8-13 Adjusting events after the balance sheet

Agreement on Software and Database Terms of Use and Maintenance Terms

Agreement on Software and Database Terms of Use and Maintenance Terms between Radlabor GmbH, Schwarzwaldstr. 175 D-79117 Freiburg Germany and - hereinafter Provider - the company or natural person, denominated

Agreement on Software and Database Terms of Use and Maintenance Terms between Radlabor GmbH, Schwarzwaldstr. 175 D-79117 Freiburg Germany and - hereinafter Provider - the company or natural person, denominated

technical factsheet 183 Leases

technical factsheet 183 Leases CONTENTS Page 1 Introduction 1 2 Legislative requirement 1 3 Accounting standards 2 4 Examples 6 5 Checklist 8 6 Sources of information 11 This technical factsheet is for

technical factsheet 183 Leases CONTENTS Page 1 Introduction 1 2 Legislative requirement 1 3 Accounting standards 2 4 Examples 6 5 Checklist 8 6 Sources of information 11 This technical factsheet is for