Corporate Insurance Bond. Presented by Adrian Boyko, CFP, CLU ChFC Regional Sales Manager-Saskatchewan

|

|

|

- Baldwin Phillips

- 8 years ago

- Views:

Transcription

1 Corporate Insurance Bond Presented by Adrian Boyko, CFP, CLU ChFC Regional Sales Manager-Saskatchewan

2 Agenda Taxation of personal income Taxation of corporate income Business structures Corporate insurance and tax Corporate insurance planning Building the cases Corporate Insurance Bond Understanding permanent whole life How it works The secrets

3 Saskatchewan personal tax* rate Combined Saskatchewan and federal personal income tax-rate brackets: 2014 Up to $43,561 26% $43,562 to $87,123 35% $87,124 to $135,054 39% $135,055 and over 44% * All tax information contained in this presentation, whether personal or corporate, is based on current CRA rules and are subject to change at any time.

4 Should you take salary, dividends or both? Salary considerations: RRSP contribution room Canada Pension Plan benefit 2014 maximum CPP benefit $12,150 Personal tax credits Medical, donations, child care tax credits, etc. Dividend considerations No CPP contributions (9.9% of salary) No EI contribution Saving could be directed to TFSA *YMPE $52,500 covered

5 Saskatchewan corporate tax rates (CCPC) Combined federal and provincial rates 2014 Small business rate - first $500,000 13% General business rate (M&P) 25% General business rate (Non M&P) 28% Investment income (rental, interest, royalty, etc.) 46.7% Dividends 33% Capital Gains 22% Eligible dividends If a Canadian-controlled private corporation ( CCPC) has both a general rate income pool (GRIP) and refundable dividend tax on hand (RDTOH) in 2013, there is an advantage for individuals over the $509,000 tax bracket to paying out eligible dividends to recover RDTOH as the personal tax rate on eligible dividends is lower than the 33.33% refund that the corporation will receive. (Personal 24.81%)

in 2013, there is an advantage for individuals over the $509,000 tax bracket to paying out eligible dividends to recover RDTOH as the personal tax rate on")

6 Do you need a holding company? Advantages can be numerous Potential tax saving Creditor protection Helps purify operating company Makes the operating business more saleable Disadvantages Cost and complexity

7 Do you need a holding company? Tax advantages and income splitting opportunities Cash value life insurance (tax advantaged) Certain tax efficient funds 20-30% more funds available for investment Investments inside a holding company Invest in : real estate, securities, private investments, life insurance policies, etc. taxed virtually the same as personal income (46.7% corporate vs 44% personal)

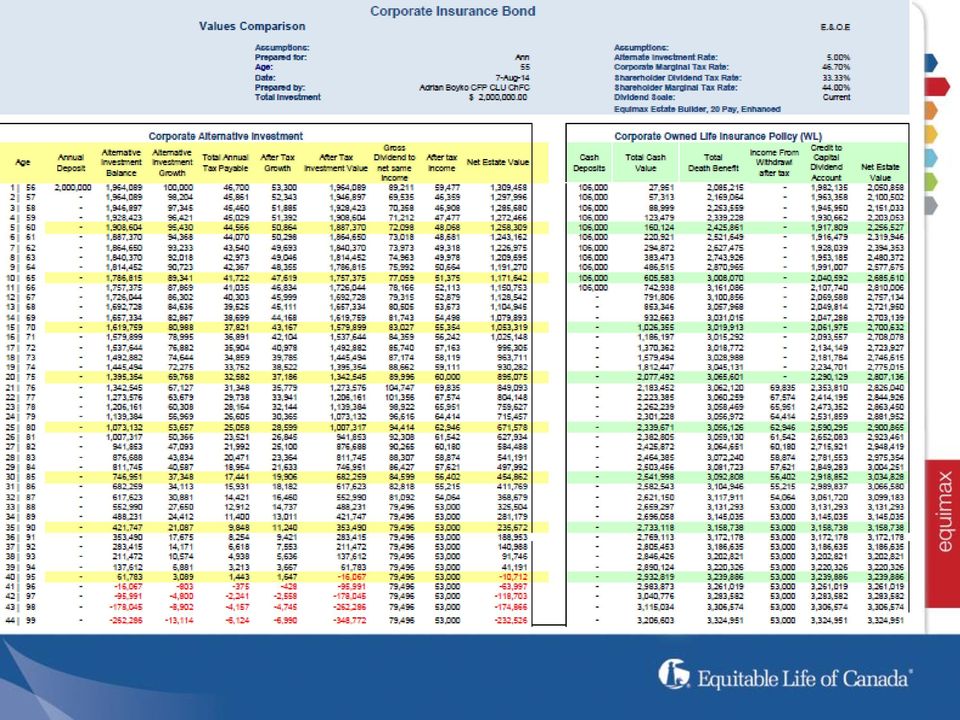

8 Corporate Insurance Bond...client profile Who is it for? Shareholders of Canadian controlled, private corporations Age 45 and older Strong desire to leave a legacy at death Receptive to long-term planning strategies

9 Corporate Insurance Bond...client profile Holdco with surplus funds to invest Situation Has retained profits or surplus cash Income not needed Corporation currently invests in: GICs Mutual funds Other taxable investments

10 Desired outcomes You (shareholders) want A financial planning strategy that will increase the funds available when you retire The capital to grow tax efficiently To pass on some of the capital to your favorite charity To pass on the bulk of your enhanced estate to your heirs

11 Options to consider Reduce the amount of current and future tax your corporation pays Replace the taxable investments within your corporation with a tax-advantaged vehicle Increase the funds available to your heirs Create a mechanism to move funds out of your corporation tax free on terminal Disposition

12 How does the Corporate Insurance Bond work? Corporation purchases a life insurance policy Corporation is named beneficiary Corporation deposits funds into the policy The cash value grows on a tax-advantaged basis

13 Corporate insurance & tax The CSV is an asset the company can control, so it should be included on the balance sheet* When death occurs the death benefit will be paid to the corporation The CSV component of the death benefit will be eliminated because of that The gross death benefit will be reflected in the financial statement however will not attract any tax liability The corporation also has the proceeds from the death benefit which will be credited to the Capital Dividend Account *James & Deborah Kraft Advisor.ca Feb 14, 2014

14 Result Corporate investment dollars Taxed at the top rate of 46.70% in Saskatchewan is converted $ now in tax-advantaged environment Increases amounts available for retirement Increase the amounts that pass to heirs tax free

15 Case study #1 Corporate Insurance Bond

16 Situation The client Ann - age 55, non-smoker, widow Business owner of Investment Holdco The situation She has a tax liability of $2,000,000 Has assets in Holdco of $2,000,000 Objective She wants to know if she can use the investments in Holdco more tax efficiently to enhance her children s and grandchild's estate values Would like income if possible

17 Strategies Leave the $2,000,000 to grow at interest in Ann s corporation (no insurance) Purchase insurance to cover tax liability Purchase annuity for income Deposit money into segregated fund* SWP cash from segregated fund Deposit cash from SWP to Equimax life insurance policy * Any amount that is allocated to a segregated fund is invested at the risk of the contractholder and may increase or decrease in value. Past performance does not guarantee future performance.

18 Strategy details Purchase a non-prescribed annuity Immediately create an annual income of $60,000 for 20 years ($897,014) Capital left $1,102,986 Purchase a segregated fund Use SWP and deplete capital of $1,102,986 over 11 years at 4% Income generated $125,000 Tax at high point $19,063 Purchase Equimax Deposit $106,000 annually for 11 years (from SWP) Take income from years 20 to 45 Outcomes?

Take income from years 20 to 45")

19 Corporate Insurance Bond

20 Recap objectives & outcomes Objective Corporate investments Corporate Insurance Bond Leave estate NO YES Have income Age Age Pay taxes of $2,000,000 Balances received or owed by estate YES Same net income Income stops at age 95 No Year 1 - $ 690,542 Age 75 - $1,104,925 Age 95 - $2,000,000 YES $ 60,000 gross $100,000 gross Yes Year 1 $ 983,138 Age 75 $ 870,136 Age 95 $1,239,886 Age 100 $1,322,377

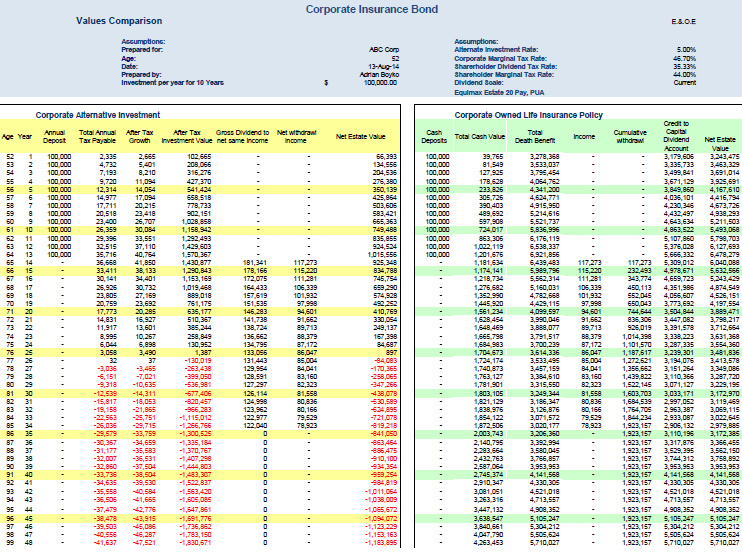

21 Case study #2 Using the strategy to increase income and tax-advantaged growth Planning for retirement income

22 Situation Case study #2 Successful corporation (OPCO) Owners Rick 52 Janice 36 Income coming up to Holdco Approximately $100,000 per year Will retire at Rick s age 65 Want income from Holdco from age 65-85

23 Assumptions used Investments inside of Holdco earn 5% Corporate Marginal Tax rate 46.70% Shareholder dividend tax rate 35.33% Equimax used current dividend scale Income taxed at 35% in policy at withdrawal

24

25 Results by the numbers Objective income Corporate investment Corporate Insurance Bond Deposit for 13 years $100,000 yearly $100,000 yearly Net estate Rick s Age 65 Age 75 Age 85 Age 95 $1,015,556 $ 84,687 $ 0 $ 0 $6,478,279 $3,554,360 $2,979,885 $4,908,352 Income Rick s age 85 Net after-tax income Age 65 Age 75 Age 85 *no income after age 76 NO $117,273 $ 87,172 $ 0* Yes $117,273 $ 87,172 $ 78,923

26 Corporate Insurance Bond Benefits: Increase estate value Tax-advantaged corporate capital Access to capital for income purposes Net death benefit for heirs or charities

27 Understanding participating whole life

28 Why participating whole life? Participating whole life insurance is a good choice for the risk averse client that: Likes guarantees Wants stable growth in their insurance policy Finds well diversified conservative investments appealing Wants hands-off investment management of their premiums vs. active management of universal life

29 What it means to own par whole life Guaranteed death benefit, cash values and premiums Eligible to participate in the distributable earnings of the Participating Account in the form of dividends Dividends are not guaranteed

30 How are dividends calculated?

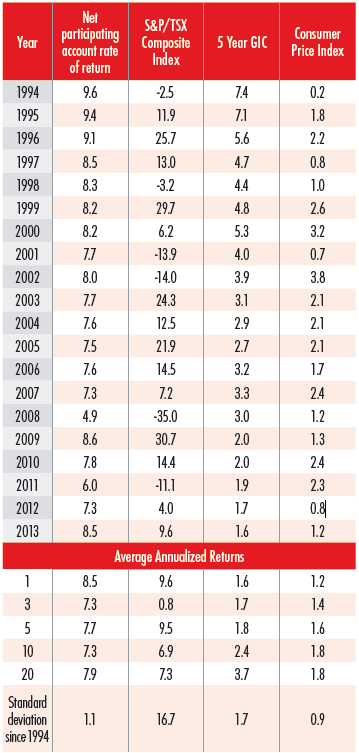

31 Participating Account experience components The main components: Investment performance Mortality and lapse Expenses Other components: Policy loans

32 Mortality and lapse Mortality experience tends to be relatively stable Has generally improved over time About 30-40% of the total dividend, depending on age and duration Lapse experience also tends to be fairly stable This component will vary by gender, smoking status, issue age and policy duration

33 Expenses Expenses tend to be a fairly small part of the total dividend This component looks at the difference between estimated and actual administration expenses

34 Investment performance The interest portion of the dividend is typically the largest portion of the dividend About 40-65% of the total dividend, depending on age and duration Based on the rate of return earned on the Participating Account assets Will increase by policy duration as the guaranteed cash value increases

35 Definitions Participating Account rate of return (or Par Yield) The rate of return earned on the Participating Account assets in a given calendar year Dividend scale interest rate The rate used in setting the dividend scale Based on recent investment experience in the Participating Account In setting this rate, actual experience will be smoothed to reduce volatility (e.g. equity returns) Dividend interest component A calculated factor based roughly on the guaranteed cash value and the difference between: Dividend scale interest rate, less investment-related expenses, and the interest rate assumed in setting the guaranteed values

36 Policy loans Policy loans form part of the assets within the Participating Account If the policy loan rate is significantly lower than the returns earned on other assets, high policy loan activity will have a negative impact on policy dividends Under the contribution principle, policy loan activity is reflected in the dividends by class The actions of a subset of policyholders will impact the dividends of an entire class

37 Participating Account investments

38 Participating Account investments

39 Participating Account investments

40 Dividend scale interest rate The current dividend scale interest rate is effective July 1, 2014 to June 30, 2015

41 Response to market conditions Sources: Statistics Canada, Bank of Canada, Equitable Life of Canada. Historical Results are not indicative of future performance. As of December 31, 2013.

42

43 Corporate Insurance Bond will help you qualify for our next conference

44

45 Conference at-a-glance CONFERENCE DATES April 1 7, 2016 DESTINATION TWO-YEAR QUALIFICATION PERIOD January 1, 2014 to December 31, 2015 MINIMUM QUALIFICATION REQUIREMENTS 135,000 Conference Credits and 20 settled policies. Space aboard the Avalon Visionary is limited. The top 40 qualifying Individual Advisors with the highest Conference Credits will be eligible to be invited to attend.

46 The best of Holland and Belgium right at your door Awe-inspiring Itinerary Day 1 Amsterdam (Embarkation) Day 2 Amsterdam Day 3 Antwerp Day 4 Ghent Day 5 Keukenhof Gardens Schoonhoven Day 6 Amsterdam (Disembarkation)

47 Won t you join us?

48 Disclaimer This presentation is intended for information purposes only and is provided with the understanding that it does not render investment, legal, accounting, tax or other professional advice. Equitable Life has made every effort to ensure the accuracy of this presentation, however accuracy is not guaranteed. If the information presented here differs from that contained in any Equitable Life policy contract, the policy contract prevails in all cases. If this presentation contains competitive information, we've made every effort to ensure its accuracy as of the date of the original oral presentation. We cannot, however, guarantee the accuracy and, if you have any questions regarding this information, you should contact the competitor directly. Dividends are not guaranteed. They are subject to change and will vary based on the actual investment returns in the Participating Account as well as mortality, expense, lapse, claims experience, taxes and other experience of the participating block of policies. Decreases in the dividend scale do not affect the guaranteed premium, guaranteed cash values, or guaranteed death benefit amount. A copy of Equitable Life s Dividend Policy and Participating Account Management Policy can be found on our website at Any amount that is allocated to a segregated fund is invested at the risk of the contractholder and may increase or decrease in value. Past performance does not guarantee future performance. denotes a trademark of The Equitable Life Insurance Company of Canada. Reproduction or redistribution of this presentation, in whole or in part, without permission from Equitable Life is forbidden The Equitable Life Insurance Company of Canada. All Rights Reserved.

49 Questions?

Whole Life Insurance. John Perre Regional Life Sales Manager

Introduction to Whole Life Insurance John Perre Regional Life Sales Manager Agenda Introduction to Equitable Life Stock company VS a mutual company Benefits of dealing with a Mutual Company Introduction

Introduction to Whole Life Insurance John Perre Regional Life Sales Manager Agenda Introduction to Equitable Life Stock company VS a mutual company Benefits of dealing with a Mutual Company Introduction

A CLOSER LOOK AT LIFE INSURANCE

Equitable Life offers term plans, a participating whole life plan, a non-participating whole life plan and two universal life plans. This chart takes a closer look at and highlights some of the key differences

Equitable Life offers term plans, a participating whole life plan, a non-participating whole life plan and two universal life plans. This chart takes a closer look at and highlights some of the key differences

Solut!ons for financial planning

Understanding your options this RRSP season 16 Solut!ons for financial planning Consider mutual funds and segregated fund contracts You ve likely heard it before: you should regularly contribute to a Registered

Understanding your options this RRSP season 16 Solut!ons for financial planning Consider mutual funds and segregated fund contracts You ve likely heard it before: you should regularly contribute to a Registered

EQUIMAX PARTICIPATING WHOLE LIFE

EQUIMAX PARTICIPATING WHOLE LIFE equimax ADVISOR GUIDE YOUR GUIDE TO EQUIMAX 6 ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations

EQUIMAX PARTICIPATING WHOLE LIFE equimax ADVISOR GUIDE YOUR GUIDE TO EQUIMAX 6 ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations

Protection Solutions. This is all about. Insured Annuities. with Standard Life

Protection Solutions This is all about Insured Annuities with Standard Life Hello. What is an Insured Annuity? The insured annuity uses two products: a prescribed annuity and life insurance. The prescribed

Protection Solutions This is all about Insured Annuities with Standard Life Hello. What is an Insured Annuity? The insured annuity uses two products: a prescribed annuity and life insurance. The prescribed

CANADIAN CORPORATE TAXATION. A General Guide January 31, 2011 TABLE OF CONTENTS INCORPORATION OF A BUSINESS 1 POTENTIAL ADVANTAGES OF INCORPORATION 1

CANADIAN CORPORATE TAXATION A General Guide January 31, 2011 TABLE OF CONTENTS PART A PAGE INCORPORATION OF A BUSINESS 1 POTENTIAL ADVANTAGES OF INCORPORATION 1 POTENTIAL DISADVANTAGES OF INCORPORATION

CANADIAN CORPORATE TAXATION A General Guide January 31, 2011 TABLE OF CONTENTS PART A PAGE INCORPORATION OF A BUSINESS 1 POTENTIAL ADVANTAGES OF INCORPORATION 1 POTENTIAL DISADVANTAGES OF INCORPORATION

Understanding Participating Whole. equimax

Understanding Participating Whole Life Insurance equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies in Canada. For generations

Understanding Participating Whole Life Insurance equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies in Canada. For generations

holistic retirement advice

Protecting your v business with holistic retirement advice a Let s talk about the Corporate Investment Shelter strategy a Life insurance is wealth protection Total wealth = human capital + financial capital

Protecting your v business with holistic retirement advice a Let s talk about the Corporate Investment Shelter strategy a Life insurance is wealth protection Total wealth = human capital + financial capital

Maximizing Your Philanthropic Gift: Effective Charitable Giving Strategies Using Your Holding Company

Maximizing Your Philanthropic Gift: Effective Charitable Giving Strategies Using Your Holding Company Canadians are generous people. Every year, thousands of Canadians support the causes they believe in

Maximizing Your Philanthropic Gift: Effective Charitable Giving Strategies Using Your Holding Company Canadians are generous people. Every year, thousands of Canadians support the causes they believe in

Corporate Estate Transfer Strategy

Transamerica s Monarch Series Client Guide Corporate Estate Transfer Strategy Monarch Series The logic behind the solution Monarch Series The logic behind the solution The logic behind the solution Transamerica

Transamerica s Monarch Series Client Guide Corporate Estate Transfer Strategy Monarch Series The logic behind the solution Monarch Series The logic behind the solution The logic behind the solution Transamerica

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

Registered Retirement Income Funds

Registered Retirement Income Funds Registered Retirement Income Funds Most Canadians are familiar with registered retirement savings plans (RSPs). Many spend decades accumulating wealth in these tax deferred

Registered Retirement Income Funds Registered Retirement Income Funds Most Canadians are familiar with registered retirement savings plans (RSPs). Many spend decades accumulating wealth in these tax deferred

Year End Tax Update Fall 2015

Year End Tax Update Fall 2015 Kevin Tran Director, Tax Advisory Services October 2015 August 2015 Agenda 1 Proposed Tax Changes Liberal Platform 2 Year-End Tax Planning - Simple Ideas 3 Distribution Planning

Year End Tax Update Fall 2015 Kevin Tran Director, Tax Advisory Services October 2015 August 2015 Agenda 1 Proposed Tax Changes Liberal Platform 2 Year-End Tax Planning - Simple Ideas 3 Distribution Planning

> The Role of Insurance in Wealth Planning

> The Role of Insurance in Wealth Planning Tax-sheltered investing using life insurance A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Tax-sheltered investing using life insurance

> The Role of Insurance in Wealth Planning Tax-sheltered investing using life insurance A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Tax-sheltered investing using life insurance

insurance solutions isn t static, neither is your business Protect life Corporate collateral loan strategy

Life insurance solutions isn t static, neither is your business Protect life Corporate collateral loan strategy Increase your business cash flow with corporately owned life insurance from Canada Life Business

Life insurance solutions isn t static, neither is your business Protect life Corporate collateral loan strategy Increase your business cash flow with corporately owned life insurance from Canada Life Business

CIFPs 11 th Annual National Conference. Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning. May 2013

Tax & Estate Planning for Business Owners CIFPs 11 th Annual National Conference Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning May 2013 DISCLAIMER The information provided is general in nature

Tax & Estate Planning for Business Owners CIFPs 11 th Annual National Conference Frank Di Pietro, CFA, CFP Director, Tax & Estate Planning May 2013 DISCLAIMER The information provided is general in nature

equimax Par Whole Life GUIDE equimax YOUR GUIDE TO EQUIMAX 02

YOUR GUIDE TO EQUIMAX equimax CLIENT GUIDE YOUR GUIDE TO EQUIMAX 02 ABOUT EQUITABLE LIFE OF CANADA Equitable Life is the largest federally regulated mutual life insurance company in Canada. For generations

YOUR GUIDE TO EQUIMAX equimax CLIENT GUIDE YOUR GUIDE TO EQUIMAX 02 ABOUT EQUITABLE LIFE OF CANADA Equitable Life is the largest federally regulated mutual life insurance company in Canada. For generations

Corporate estate transfer with cash withdrawal

Life Insurance Solutions guarantees products assets opportunities growth capital protection income benefit solutions options stability Plan today. Provide tomorrow. Corporate estate transfer with cash

Life Insurance Solutions guarantees products assets opportunities growth capital protection income benefit solutions options stability Plan today. Provide tomorrow. Corporate estate transfer with cash

Business Insurance Part 2

Business Insurance Part 2 Insurance Concepts for Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Owner Insurance Concepts > Buy Sell > Key Person

Business Insurance Part 2 Insurance Concepts for Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Owner Insurance Concepts > Buy Sell > Key Person

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

How Can You Reduce Your Taxes?

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

RON GRAHAM AND ASSOCIATES LTD. 10585 111 Street NW, Edmonton, Alberta, T5M 0L7 Telephone (780) 429-6775 Facsimile (780) 424-0004 Email rgraham@rgafinancial.com How Can You Reduce Your Taxes? Tax Brackets.

Estate Planning. Insured Inheritance. Income Shelter. Insured Annuity. Capital Gains Protector

Estate Planning Insured Inheritance The Insured Inheritance concept demonstrates an opportunity to shelter a lump sum investment from income tax and to ensure that the maximum tax-free dollars become available

Estate Planning Insured Inheritance The Insured Inheritance concept demonstrates an opportunity to shelter a lump sum investment from income tax and to ensure that the maximum tax-free dollars become available

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR Participate in your brighter future with Sun Life Financial. Participating life insurance is a powerful tool that protects

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR Participate in your brighter future with Sun Life Financial. Participating life insurance is a powerful tool that protects

INCORPORATING YOUR BUSINESS

November 2014 CONTENTS Advantages of incorporation Advantages of an SBC Summary INCORPORATING YOUR BUSINESS If you carry on a business, there are many tax planning opportunities which become available

November 2014 CONTENTS Advantages of incorporation Advantages of an SBC Summary INCORPORATING YOUR BUSINESS If you carry on a business, there are many tax planning opportunities which become available

TAX-EXEMPT LIFE INSURANCE

TAX-EXEMPT LIFE INSURANCE For wealth creation and estate maximization The strategies, advice and technical content in this publication are provided for the general guidance and benefit of our clients,

TAX-EXEMPT LIFE INSURANCE For wealth creation and estate maximization The strategies, advice and technical content in this publication are provided for the general guidance and benefit of our clients,

Introducing. Tax-Free Savings Accounts

Introducing Tax-Free Savings Accounts Tax-Free Savings Accounts A new way to save Tax-free savings accounts were introduced by the federal government in the 2008 budget as an incentive for Canadians to

Introducing Tax-Free Savings Accounts Tax-Free Savings Accounts A new way to save Tax-free savings accounts were introduced by the federal government in the 2008 budget as an incentive for Canadians to

Fact Finding Guide. Estate Preservation

Fact Finding Guide Estate Preservation Fact Finding Guide This Fact Finding Guide helps you gather the important information you need to show your clients how life insurance can be used to offset final

Fact Finding Guide Estate Preservation Fact Finding Guide This Fact Finding Guide helps you gather the important information you need to show your clients how life insurance can be used to offset final

INVESTMENT HOLDING COMPANIES

INVESTMENT HOLDING COMPANIES > RBC DOMINION SECURITIES INC. FINANCIAL PLANNING PUBLICATIONS At RBC Dominion Securities Inc., we have been helping clients achieve their financial goals since 1901. Today,

INVESTMENT HOLDING COMPANIES > RBC DOMINION SECURITIES INC. FINANCIAL PLANNING PUBLICATIONS At RBC Dominion Securities Inc., we have been helping clients achieve their financial goals since 1901. Today,

THE TAX-FREE SAVINGS ACCOUNT

THE TAX-FREE SAVINGS ACCOUNT The 2008 federal budget introduced the Tax-Free Savings Account (TFSA) for individuals beginning in 2009. The TFSA allows you to set money aside without paying tax on the income

THE TAX-FREE SAVINGS ACCOUNT The 2008 federal budget introduced the Tax-Free Savings Account (TFSA) for individuals beginning in 2009. The TFSA allows you to set money aside without paying tax on the income

Corporate asset efficiency

Life insurance solutions Corporate asset efficiency Manage. Access. Preserve. A smart solution for professionals permanent life insurance, a unique asset that can offer tax-advantaged growth. Consider

Life insurance solutions Corporate asset efficiency Manage. Access. Preserve. A smart solution for professionals permanent life insurance, a unique asset that can offer tax-advantaged growth. Consider

TAX, RETIREMENT & ESTATE PLANNING SERVICES. Registered Retirement Savings Plan (RRSP) THE FACTS

THE FACTS") TAX, RETIREMENT & ESTATE PLANNING SERVICES Registered Retirement Savings Plan (RRSP) THE FACTS Table of contents What is an RRSP?... 3 Why should I contribute to an RRSP?... 4 When can I contribute?...

TAX, RETIREMENT & ESTATE PLANNING SERVICES Registered Retirement Savings Plan (RRSP) THE FACTS Table of contents What is an RRSP?... 3 Why should I contribute to an RRSP?... 4 When can I contribute?...

Universal Life. What is Universal Life? The Structure of a Universal Life Policy. A Flexible, Tax-Sheltered Investment Program

Many Canadians consider their Registered Retirement Saving Plan (RRSP) to be their best tax shelter. However, Universal Life (UL) insurance has become an increasingly popular long-term financial planning

Many Canadians consider their Registered Retirement Saving Plan (RRSP) to be their best tax shelter. However, Universal Life (UL) insurance has become an increasingly popular long-term financial planning

INSURED ANNUITY STRATEGY. Help your clients increase their after-tax income with universal life, without reducing the estate for their heirs.

INSURED ANNUITY STRATEGY Help your clients increase their after-tax income with universal life, without reducing the estate for their heirs. Here s the story Dennis and Rosemary, ages 68 and 64, have worked

INSURED ANNUITY STRATEGY Help your clients increase their after-tax income with universal life, without reducing the estate for their heirs. Here s the story Dennis and Rosemary, ages 68 and 64, have worked

Performance Annuity. with Standard Life. Your guide to. Investment Solutions

Investment Solutions Your guide to Performance Annuity with Standard Life For insurance representative use only. This document is not intended for public distribution. title Hello. Performance Annuity:

Investment Solutions Your guide to Performance Annuity with Standard Life For insurance representative use only. This document is not intended for public distribution. title Hello. Performance Annuity:

Life insurance solutions for. business owners

Life insurance solutions for business owners Life insurance solutions for business owners What s the best life insurance for business owners? It depends on where you see yourself in the future and at which

Life insurance solutions for business owners Life insurance solutions for business owners What s the best life insurance for business owners? It depends on where you see yourself in the future and at which

Planning your client s future

Planning your client s future Using insurance for your client s corporate planning needs TAX, RETIREMENT & ESTATE PLANNING SERVICES This information is for advisor use only. It is not intended for clients.

Planning your client s future Using insurance for your client s corporate planning needs TAX, RETIREMENT & ESTATE PLANNING SERVICES This information is for advisor use only. It is not intended for clients.

retirement income solutions *Advisor Design guide for Life s brighter under the sun What s inside Retirement income solutions advisor guide USE ONLY

Retirement income solutions advisor guide *Advisor USE ONLY Design guide for retirement income solutions What s inside Discussing retirement needs with clients Retirement income product comparison Creating

Retirement income solutions advisor guide *Advisor USE ONLY Design guide for retirement income solutions What s inside Discussing retirement needs with clients Retirement income product comparison Creating

YOU CAN OWN? WHY RENT WHEN

WHY RENT WHEN YOU CAN OWN? A COMPARISON OF TERM & PERMANENT LIFE INSURANCE This guide helps you understand the differences between term and permanent coverage by comparing them to renting versus owning

WHY RENT WHEN YOU CAN OWN? A COMPARISON OF TERM & PERMANENT LIFE INSURANCE This guide helps you understand the differences between term and permanent coverage by comparing them to renting versus owning

TAX, RETIREMENT & ESTATE PLANNING SERVICES. Clawback calculator user guide

TAX, RETIREMENT & ESTATE PLANNING SERVICES Clawback calculator user guide Table of contents Introduction... 3 Fully taxable and investment income Fully taxable income... 4 Investment income... 5 Deductions

TAX, RETIREMENT & ESTATE PLANNING SERVICES Clawback calculator user guide Table of contents Introduction... 3 Fully taxable and investment income Fully taxable income... 4 Investment income... 5 Deductions

Bye-bye Bonus! Why small business owners may prefer dividends over a bonus

Bye-bye Bonus! Why small business owners may prefer dividends over a bonus Jamie Golombek Managing Director, Tax & Estate Planning, CI Wealth Advisory Services September 2015 Traditionally, many Canadian

Bye-bye Bonus! Why small business owners may prefer dividends over a bonus Jamie Golombek Managing Director, Tax & Estate Planning, CI Wealth Advisory Services September 2015 Traditionally, many Canadian

The Corporate Asset Transfer Plan. Someone is going to profit from all of your client s hard work. Shouldn t it be their family?

The Corporate Asset Transfer Plan Someone is going to profit from all of your client s hard work. Shouldn t it be their family? Target Market Owners of privately controlled Canadian corporations who are

The Corporate Asset Transfer Plan Someone is going to profit from all of your client s hard work. Shouldn t it be their family? Target Market Owners of privately controlled Canadian corporations who are

> The Role of Insurance in Wealth Planning

> The Role of Insurance in Wealth Planning Executive retirement solutions A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Executive retirement solutions Everyone wants enough retirement

> The Role of Insurance in Wealth Planning Executive retirement solutions A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Executive retirement solutions Everyone wants enough retirement

Registered Retirement Income Funds

Registered Retirement Income Funds The Income Tax Act states that a Registered Retirement Savings Plan (RRSP) matures by December 31 of the year in which the planholder (annuitant) reaches age 69. At the

Registered Retirement Income Funds The Income Tax Act states that a Registered Retirement Savings Plan (RRSP) matures by December 31 of the year in which the planholder (annuitant) reaches age 69. At the

Total Financial Solutions. Practical Perspectives on Tax Planning

TM Trademark used under authorization and control of The Bank of Nova Scotia. ScotiaMcLeod is a division of Scotia Capital Inc., Member CIPF. All insurance products are sold through ScotiaMcLeod Financial

TM Trademark used under authorization and control of The Bank of Nova Scotia. ScotiaMcLeod is a division of Scotia Capital Inc., Member CIPF. All insurance products are sold through ScotiaMcLeod Financial

Creating a Life Legacy

Creating a Life Legacy Prepared for: Client Presented by: Bernie Geiss, TEP, FEA, CLU, CFP Cove Continuity Advisors Inc. October 2009 Issues and Considerations Successful investors have accumulated capital

Creating a Life Legacy Prepared for: Client Presented by: Bernie Geiss, TEP, FEA, CLU, CFP Cove Continuity Advisors Inc. October 2009 Issues and Considerations Successful investors have accumulated capital

financial planning & advice

financial planning & advice Tips for successful investing. Start early and invest regularly Do your homework take the time to become an informed investor Develop an investment strategy you are comfortable

financial planning & advice Tips for successful investing. Start early and invest regularly Do your homework take the time to become an informed investor Develop an investment strategy you are comfortable

Income Splitting CONTENTS

June 2012 CONTENTS The attribution rules Family income splitting Business income splitting Income splitting through corporations Income splitting in retirement Summary Income Splitting With Canada s high

June 2012 CONTENTS The attribution rules Family income splitting Business income splitting Income splitting through corporations Income splitting in retirement Summary Income Splitting With Canada s high

> The Role of Insurance in Wealth Planning

> The Role of Insurance in Wealth Planning Insurance solutions for planned giving A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Insurance solutions for planned giving Charitable

> The Role of Insurance in Wealth Planning Insurance solutions for planned giving A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Insurance solutions for planned giving Charitable

Roth IRAs and Conversions

Roth IRAs and Conversions When the law that created Roth IRAs was originally enacted there were two eligibility limits placed on them. The first affected an individual s ability to contribute to the Roth-

Roth IRAs and Conversions When the law that created Roth IRAs was originally enacted there were two eligibility limits placed on them. The first affected an individual s ability to contribute to the Roth-

PLAIN TALK about LIFE INSURANCE

PLAIN TALK about LIFE INSURANCE Having the right life insurance protection can have an enormous effect on your life and the lives of those you love. A proper financial security plan can mean the difference

PLAIN TALK about LIFE INSURANCE Having the right life insurance protection can have an enormous effect on your life and the lives of those you love. A proper financial security plan can mean the difference

Life Insurance and Financial Planning Moving from Needing to Wanting. Or Why do High Net Worth Clients Buy Life Insurance. Important information

Life Insurance and Financial Planning Moving from Needing to Wanting Florence Marino, LL.B., TEP AVP Tax & Estate Planning Group Or Why do High Net Worth Clients Buy Life Insurance Florence Marino, LL.B.,

Life Insurance and Financial Planning Moving from Needing to Wanting Florence Marino, LL.B., TEP AVP Tax & Estate Planning Group Or Why do High Net Worth Clients Buy Life Insurance Florence Marino, LL.B.,

Financial security at death. Why life insurance? Let s talk about how life insurance protects you

Financial security at death Why life insurance? Let s talk about how life insurance protects you Who needs life insurance? People with responsibility for others n Take care of the immediate challenges

Financial security at death Why life insurance? Let s talk about how life insurance protects you Who needs life insurance? People with responsibility for others n Take care of the immediate challenges

Continuing Education for Advisors

Continuing Education for Advisors knowledge continuing training educate online awareness participate Participating life insurance Learning objectives By the end of this course you will be able to: Explain

Continuing Education for Advisors knowledge continuing training educate online awareness participate Participating life insurance Learning objectives By the end of this course you will be able to: Explain

NexGen Tax Cases The Corporate Tax Deferral and Income Program

2014 NexGen Tax Cases The Corporate Tax Deferral and Income Program Business owners and managers in Canada who have incorporated have two major income tax advantages available to them over those who have

2014 NexGen Tax Cases The Corporate Tax Deferral and Income Program Business owners and managers in Canada who have incorporated have two major income tax advantages available to them over those who have

plain talk about life insurance

plain talk about life insurance The right life insurance can have an enormous effect on your life and the lives of those you love. It can mean the difference between leaving your loved ones well positioned

plain talk about life insurance The right life insurance can have an enormous effect on your life and the lives of those you love. It can mean the difference between leaving your loved ones well positioned

How To Get A Pension In Canada

Easy Guide to Retirement Income Options Contents PAGE 1: Your retirement income choices... 2 1. Convert your RSP into an annuity... 2 a. Life Annuity... 2 b. Term Certain Annuity to Age 90... 2 2. Convert

Easy Guide to Retirement Income Options Contents PAGE 1: Your retirement income choices... 2 1. Convert your RSP into an annuity... 2 a. Life Annuity... 2 b. Term Certain Annuity to Age 90... 2 2. Convert

Tax Planning 101 for Canadian Investors

Tax Planning 101 for Canadian Investors Tariq Ali Asghar www.emergingstar.com 1 TABLE OF CONTENTS Goal of Tax Planning Analysis Part One: Tax Planning and Investment Management Strategies 1. Different

Tax Planning 101 for Canadian Investors Tariq Ali Asghar www.emergingstar.com 1 TABLE OF CONTENTS Goal of Tax Planning Analysis Part One: Tax Planning and Investment Management Strategies 1. Different

Investing With Whole Life Participating Insurance For Affluent Families

Investing With Whole Life Participating Insurance For Affluent Families By Norm Ayoub, Director, Business Advisory Board HighView Financial Group November 2011 Overview: The foundation of any good financial

Investing With Whole Life Participating Insurance For Affluent Families By Norm Ayoub, Director, Business Advisory Board HighView Financial Group November 2011 Overview: The foundation of any good financial

Personal retirement account A retirement savings strategy. Show clients a tax-preferred solution to enhance retirement income

Personal retirement account A retirement savings strategy using PARTICIPATING life insurance Show clients a tax-preferred solution to enhance retirement income 2 Personal retirement account Here s the

Personal retirement account A retirement savings strategy using PARTICIPATING life insurance Show clients a tax-preferred solution to enhance retirement income 2 Personal retirement account Here s the

year-end tax planning opportunities

year-end tax planning opportunities These important tax and financial planning moves can help prepare you for the upcoming tax season and better align your portfolio with your short- and long-term goals.

year-end tax planning opportunities These important tax and financial planning moves can help prepare you for the upcoming tax season and better align your portfolio with your short- and long-term goals.

Tax Planning Opportunities Involving Professional Corporations

Tax Planning Opportunities Involving Professional Corporations A Discussion Paper Prepared by: Alan Koop, CA Prepared for: The Saskatchewan Provincial Court Judges Association Table of Contents Executive

Tax Planning Opportunities Involving Professional Corporations A Discussion Paper Prepared by: Alan Koop, CA Prepared for: The Saskatchewan Provincial Court Judges Association Table of Contents Executive

APPENDIX 4 - LIFE INSURANCE POLICIES PREMIUMS, RESERVES AND TAX TREATMENT

APPENDIX 4 - LIFE INSURANCE POLICIES PREMIUMS, RESERVES AND TAX TREATMENT Topics in this section include: 1.0 Types of Life Insurance 1.1 Term insurance 1.2 Type of protection 1.3 Premium calculation for

APPENDIX 4 - LIFE INSURANCE POLICIES PREMIUMS, RESERVES AND TAX TREATMENT Topics in this section include: 1.0 Types of Life Insurance 1.1 Term insurance 1.2 Type of protection 1.3 Premium calculation for

Everything you need to know about Tax-Free Savings Accounts (TFSAs)

") Tax, Retirement & Estate Planning Services TAX-FREE SAVINGS ACCOUNT THE FACTS Everything you need to know about Tax-Free Savings Accounts (TFSAs) Until 2009, many Canadians held their savings in Registered

Tax, Retirement & Estate Planning Services TAX-FREE SAVINGS ACCOUNT THE FACTS Everything you need to know about Tax-Free Savings Accounts (TFSAs) Until 2009, many Canadians held their savings in Registered

Investor Guide. RRIF Investing. Managing your money in retirement

Investor Guide RRIF Investing Managing your money in retirement 1 What s inside It s almost time to roll over your RRSP...3 RRIFs...4 Frequently asked questions...5 Manage your RRIF...8 Your advisor...10

Investor Guide RRIF Investing Managing your money in retirement 1 What s inside It s almost time to roll over your RRSP...3 RRIFs...4 Frequently asked questions...5 Manage your RRIF...8 Your advisor...10

Business Insurance Part 1

Business Insurance Part 1 Working with Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Structures and Taxation A PARTNER YOU CAN TRUST. 1 Business

Business Insurance Part 1 Working with Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Structures and Taxation A PARTNER YOU CAN TRUST. 1 Business

Professional Corporations. Presented by Raza Husain, CA

Professional Corporations Presented by Raza Husain, CA Should I Incorporate? Questions: Does the professional practice generate more net income than is needed to meet the lifestyle expenses of the professional?

Professional Corporations Presented by Raza Husain, CA Should I Incorporate? Questions: Does the professional practice generate more net income than is needed to meet the lifestyle expenses of the professional?

Incorporating your farm. Is it right for you?

Incorporating your farm Is it right for you? RBC Royal Bank Incorporating your farm 2 The following article was written by RBC Wealth Management Services If you have considered incorporating your farm,

Incorporating your farm Is it right for you? RBC Royal Bank Incorporating your farm 2 The following article was written by RBC Wealth Management Services If you have considered incorporating your farm,

Your guide to Canada Life s participating life insurance. Estate Achiever Wealth Achiever

Your guide to Canada Life s participating life insurance Estate Achiever Wealth Achiever This guide provides an overview of key features of participating life insurance products offered by Canada Life.

Your guide to Canada Life s participating life insurance Estate Achiever Wealth Achiever This guide provides an overview of key features of participating life insurance products offered by Canada Life.

UNIVERSAL LIFE INSURANCE YOUR 5-MINUTE GUIDE. Flexible protection for what s most important in life

UNIVERSAL LIFE INSURANCE YOUR 5-MINUTE GUIDE Flexible protection for what s most important in life Protection for all the moments that matter Be sure to choose a product that meets long-term life insurance

UNIVERSAL LIFE INSURANCE YOUR 5-MINUTE GUIDE Flexible protection for what s most important in life Protection for all the moments that matter Be sure to choose a product that meets long-term life insurance

Charitable Planned Giving

` Insuring the Future In this Newsletter: Charitable Planned Giving Legislative Changes John Jordan, CFP CERTIFIED FINANCIAL PLANNER Phone: (519) 272-3112 Toll Free: (866) 272-3112 Fax: (519) 662-6414

` Insuring the Future In this Newsletter: Charitable Planned Giving Legislative Changes John Jordan, CFP CERTIFIED FINANCIAL PLANNER Phone: (519) 272-3112 Toll Free: (866) 272-3112 Fax: (519) 662-6414

CURRICULUM LLQP MODULE: Life insurance DURATION OF THE EXAM: 75 minutes - NUMBER OF QUESTIONS: 30 questions

CURRICULUM LLQP MODULE: DURATION OF THE EXAM: 75 minutes - NUMBER OF QUESTIONS: 30 questions Competency: Recommend individual and group life insurance products adapted to the client s needs and situation

CURRICULUM LLQP MODULE: DURATION OF THE EXAM: 75 minutes - NUMBER OF QUESTIONS: 30 questions Competency: Recommend individual and group life insurance products adapted to the client s needs and situation

The Corporate Investment Shelter. Corporate investments

September 2012 The Corporate Investment Shelter Many successful business owners retire with more assets than they need to live well. With that realization, their focus can shift from providing retirement

September 2012 The Corporate Investment Shelter Many successful business owners retire with more assets than they need to live well. With that realization, their focus can shift from providing retirement

How To Tax A Life Insurance Policy On A Policy In The United States

Taxation of Life Insurance Policy Loans and Dividends Introduction Policyholders are required to include in income any gains realized upon the disposition of all or a portion of their interest in a life

Taxation of Life Insurance Policy Loans and Dividends Introduction Policyholders are required to include in income any gains realized upon the disposition of all or a portion of their interest in a life

Understanding Your Life Insurance Options

Understanding Your Life Insurance Options Designed for: Client Designed by: Bernie Geiss, TEP, FEA, CLU, CFP Cove Continuity Advisors Inc. Life Insurance: An Integral Part of Most Financial Plans The primary

Understanding Your Life Insurance Options Designed for: Client Designed by: Bernie Geiss, TEP, FEA, CLU, CFP Cove Continuity Advisors Inc. Life Insurance: An Integral Part of Most Financial Plans The primary

Corporate Insured Retirement Plan. Because successful businesses need security and income

Corporate Insured Retirement Plan Because successful businesses need security and income The Opportunity Business owners who need insurance to Fund a buy-sell agreement between partners of the company

Corporate Insured Retirement Plan Because successful businesses need security and income The Opportunity Business owners who need insurance to Fund a buy-sell agreement between partners of the company

Your Company Name Retirement Compensation Arrangement (current date) page 1 of 6

page 1 of 6") (current date) page 1 of 6 "Generating additional retirement income through tax sheltered accumulation!" Many businesses would like to provide additional compensation for key employees. This could include

(current date) page 1 of 6 "Generating additional retirement income through tax sheltered accumulation!" Many businesses would like to provide additional compensation for key employees. This could include

Sample retirement plan prepared with. The Canadian Retirement Planner s Software. For information visit http://www.gobeil.ca/

RETIREMENT PLAN PROVINCE OF ONTARIO AS AT JANUARY 1, 2012 PREPARED BY DAVID GOBEIL, CA, CFP NOVEMBER 14, 2011 VERSION DRAFT Sample retirement plan prepared with The Canadian Retirement Planner s Software

RETIREMENT PLAN PROVINCE OF ONTARIO AS AT JANUARY 1, 2012 PREPARED BY DAVID GOBEIL, CA, CFP NOVEMBER 14, 2011 VERSION DRAFT Sample retirement plan prepared with The Canadian Retirement Planner s Software

universal life UNIVERSAL LIFE INVESTOR PROFILER QUESTIONNAIRE

universal life UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE Universal life combines the benefits of cost-effective life insurance protection with tax-advantaged

universal life UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE UNIVERSAL LIFE INVEST PROFILER QUESTIONNAIRE Universal life combines the benefits of cost-effective life insurance protection with tax-advantaged

Immediate Annuities. Reno J. Frazzitta Investment Advisor Representative 877-909-7233 www.thesmartmoneyguy.com

Reno J. Frazzitta Investment Advisor Representative 877-909-7233 www.thesmartmoneyguy.com Immediate Annuities Page 1 of 7, see disclaimer on final page Immediate Annuities What is an immediate annuity?

Reno J. Frazzitta Investment Advisor Representative 877-909-7233 www.thesmartmoneyguy.com Immediate Annuities Page 1 of 7, see disclaimer on final page Immediate Annuities What is an immediate annuity?

>Most investors spend the majority of their time thinking and planning

Generating Retirement Income using a Systematic Withdrawal Plan SPECIAL REPORT >Most investors spend the majority of their time thinking and planning around how best to save for retirement. But once you

Generating Retirement Income using a Systematic Withdrawal Plan SPECIAL REPORT >Most investors spend the majority of their time thinking and planning around how best to save for retirement. But once you

Whole life insurance. 5-minute guide. The promise of life insurance.

Whole life insurance 5-minute guide The promise of life insurance. Keep your promise As a spouse or parent, you ve made a commitment to take care of and provide for your family. If you ve built your own

Whole life insurance 5-minute guide The promise of life insurance. Keep your promise As a spouse or parent, you ve made a commitment to take care of and provide for your family. If you ve built your own

YOUR GUIDE TO EQUILIFE LIMITED PAY UNIVERSAL LIFE

YOUR GUIDE TO EQUILIFE LIMITED PAY UNIVERSAL LIFE equilife CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

YOUR GUIDE TO EQUILIFE LIMITED PAY UNIVERSAL LIFE equilife CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

EMPLOYEE STOCK OPTIONS

TAX LETTER May 2015 EMPLOYEE STOCK OPTIONS FOREIGN EXCHANGE GAINS AND LOSSES CAREGIVER AND INFIRM DEPENDENT CREDITS MAKING TAX INSTALMENTS EARNED INCOME FOR RRSP PURPOSES AROUND THE COURTS EMPLOYEE STOCK

TAX LETTER May 2015 EMPLOYEE STOCK OPTIONS FOREIGN EXCHANGE GAINS AND LOSSES CAREGIVER AND INFIRM DEPENDENT CREDITS MAKING TAX INSTALMENTS EARNED INCOME FOR RRSP PURPOSES AROUND THE COURTS EMPLOYEE STOCK

The Lifetime Capital Gains Exemption

The Lifetime Capital Gains Exemption Introduction This Tax Topic briefly reviews the rules contained in section 110.6 of the Income Tax Act (the "Act") concerning the lifetime capital gains exemption and

The Lifetime Capital Gains Exemption Introduction This Tax Topic briefly reviews the rules contained in section 110.6 of the Income Tax Act (the "Act") concerning the lifetime capital gains exemption and

Income Taxes module. After covering the topics in the module booklets or web pages and this workshop, learners will be able to:

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

Income Taxes module Trainer s Introduction Most people are aware that they must file an income tax return in Canada, if only to claim back any excess taxes that were withheld from their income. Filing

YEAR-END TAX PLANNER November 2014

YEAR-END TAX PLANNER November 2014 Inside this issue: Dear Clients and Friends, as we approach the end of another year, now would be a good time to consider some tax planning measures that could help reduce

YEAR-END TAX PLANNER November 2014 Inside this issue: Dear Clients and Friends, as we approach the end of another year, now would be a good time to consider some tax planning measures that could help reduce

Module 5 - Saving HANDOUT 5-7

HANDOUT 5-7 Savings Tools (detailed) 5 Contents High interest savings account This is a type of deposit account. The bank pays you interest. The rate changes with the prime rate set by the bank. This is

HANDOUT 5-7 Savings Tools (detailed) 5 Contents High interest savings account This is a type of deposit account. The bank pays you interest. The rate changes with the prime rate set by the bank. This is

London Life participating life insurance

Your guide to London Life participating life insurance Value, strength and choice What you ll learn from this guide This guide, combined with professional advice from your financial security advisor, helps

Your guide to London Life participating life insurance Value, strength and choice What you ll learn from this guide This guide, combined with professional advice from your financial security advisor, helps

plaintalk about life insurance

plaintalk about life insurance The right life insurance protection can have an enormous effect on your life and the lives of those you love. It can mean the difference between leaving your loved ones well

plaintalk about life insurance The right life insurance protection can have an enormous effect on your life and the lives of those you love. It can mean the difference between leaving your loved ones well

EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/75 AND GUARANTEED INVESTMENT FUNDS 75/100 INFORMATION FOLDER AND CONTRACT PROVISIONS

THE EMPIRE LIFE INSURANCE COMPANY EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/75 AND GUARANTEED INVESTMENT FUNDS 75/100 INFORMATION FOLDER AND CONTRACT PROVISIONS This document contains the information

THE EMPIRE LIFE INSURANCE COMPANY EMPIRE LIFE GUARANTEED INVESTMENT FUNDS 75/75 AND GUARANTEED INVESTMENT FUNDS 75/100 INFORMATION FOLDER AND CONTRACT PROVISIONS This document contains the information

This strategy gives a person the ability to take advantage of the tax-sheltering ability of a life insurance policy.

Insuring the Future In this Newsletter: Supplementing Retirement Income Who should be looking at this strategy? The Registered Savings Problem John Jordan, CFP CERTIFIED FINANCIAL PLANNER Phone: (519)

Insuring the Future In this Newsletter: Supplementing Retirement Income Who should be looking at this strategy? The Registered Savings Problem John Jordan, CFP CERTIFIED FINANCIAL PLANNER Phone: (519)

TAX, RETIREMENT & ESTATE PLANNING SERVICES. A Guide to Leveraged Life Insurance WHAT YOU NEED TO KNOW BEFORE YOU LEVERAGE YOUR LIFE INSURANCE POLICY

TAX, RETIREMENT & ESTATE PLANNING SERVICES A Guide to Leveraged Life Insurance WHAT YOU NEED TO KNOW BEFORE YOU LEVERAGE YOUR LIFE INSURANCE POLICY This guide provides information on leveraged life insurance.

TAX, RETIREMENT & ESTATE PLANNING SERVICES A Guide to Leveraged Life Insurance WHAT YOU NEED TO KNOW BEFORE YOU LEVERAGE YOUR LIFE INSURANCE POLICY This guide provides information on leveraged life insurance.

Are Insurance Premiums Deductible?

Are Insurance Premiums Deductible? August 2014 Can I deduct the premiums? That s a question you probably hear when you re presenting an insurance concept. Unfortunately, the answer is generally no insurance

Are Insurance Premiums Deductible? August 2014 Can I deduct the premiums? That s a question you probably hear when you re presenting an insurance concept. Unfortunately, the answer is generally no insurance