Valuation of Investment Management ( IM ) Firms

|

|

|

- Brianna Wilson

- 8 years ago

- Views:

Transcription

1 Valuation of Investment Management ( IM ) Firms PRESENTATION BY: Terence L. Griswold, ASA Managing Director Empire Valuation Consultants, LLC CFA Society of Rochester March 26, 2013

2 Agenda Part I: Operating Trends Death (and Rebirth) of Equities Pressure on Profitability Is the Industry Becoming Commoditized? Part II: Valuation Considerations Concepts of Value Valuation Approaches Other Valuation Considerations The Valuation Gap Part III: The Art of the Deal The Decision to Sell Deal Types & Typical Structures 2

3 PART 1: Operating Trends 3

4 Operating Trends (I) Death of Equities? The Cult of Equity Is Dying. Bill Gross Is the above statement true? Data through the end of 2012 supports the notion that investors are falling out of love with equities. In 2012, equity mutual fund flows were negative for the fifth straight year, while inflows to bond funds remained robust (Details on next slide). Returns on bonds have experienced an unprecedented run in the past twenty years. Since bond funds have lower fees, this has directly impacted the profitability (and ultimately the value) of asset managers. 4

. Returns on bonds have experienced an unprecedented run in the past twenty years.")

5 Operating Trends (II) Death of Equities? Investment Company Institute ( ICI ) Data Supports the Decline in Equities through 2012, BUT... Year/Quarter Mutual Fund Flows ($B) Equity Hybrid Bond 2008 $(234) $(18) $ $(9) $23 $ $(37) $23 $ $(98) $84 $239 1Q 2012 $(9) $58 $215 2Q 2012 $(18) $3 $155 3Q 2012 $(52) $16 $86 4Q 2012 $(70) $3 $66 5

$23 $376 2010 $(37) $23 $241 2011 $(98) $84 $239 1Q 2012 $(9) $58 $215 2Q 2012 $(18)")

6 Operating Trends (III) Rebirth of Equities? ICI Data show that flows to equity funds totaled $38 billion in January This was the largest monthly net inflow post-financial crisis. Equity fund inflows outpaced bond fund inflows for the first time since January Virtually all equity indices have posted positive returns YTD through March 15, with the S&P 500 and Dow Jones Industrial Average trading near alltime highs. Key Takeaways? 6

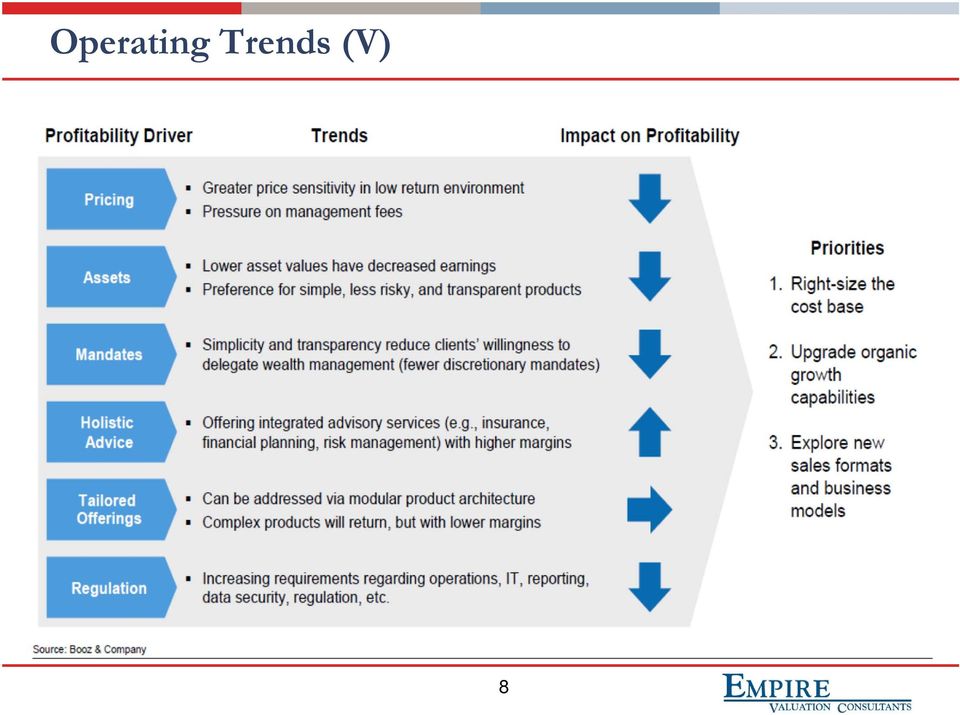

7 Operating Trends (IV) Profitability Is Under Pressure A recent study by Booz & Company has outlined several areas that impact the profitability of wealth management firms (U.S Wealth Management Survey: Trends and Emerging Business Models). Areas negatively impacting profitability include pressure on management fees, preference for less risky products, more simple mandates, and increasing regulation. Areas positively impacting profitability include offering integrated advice with higher margins, i.e., financial planning, risk management. In response to the profitability challenges, Booz has outlined the following priorities for wealth management firms: (1) right-size the cost basis; (2) upgrade organic growth capabilities; and (3) explore new sales formats and business models, i.e., the hybrid model. In the hybrid model, an RIA forms an alliance with a broker-dealer. This enables the owner of the RIA to offer additional services while still remaining independent. 7

8 Operating Trends (V) 8

9 Operating Trends (VI) Is the Industry Becoming Commoditized? Execution of trades has become commoditized, driven by technology and the rise of online brokers like E-Trade and Charles Schwab. Index investing has become commoditized with the acceleration of ETFs. Similarly, active management has more recently become commoditized through the rise of actively managed and alternative ETFs. The above factors have undoubtedly impacted the industry. Nonetheless, the industry has shown resilience by focusing on the unique needs and complex circumstances of the client. Additionally, since outcomes (returns) can vary greatly, it appears that commoditization will continue to be a nagging threat, rather than a fatal one. These factors affect IM firms operating risk and competitive advantage period, which are key elements of valuation. 9

can vary greatly, it appears that commoditization will continue to be a nagging threat, rather than a fatal one.")

10 PART 2: Valuation Considerations 10

11 Valuation Considerations (I) Value Drivers for IM Companies Size (reaching scale is important) Revenue Growth (organic growth or market growth) Revenue Source (commission-based or fee based) Client Demographics (client concentration, client tenure, new client ratio, client age) Relationship of Revenue to Owner of Firm Compensation and Expense Management Employee Demographics (number of employees, tenure, relationship with clients) These are factors that should all be considered by the valuator and directly impact company-specific risk (as well relative valuation multiples). 11

These are factors that should all be considered by the valuator and directly impact company-specific risk (as well relative")

12 Valuation Considerations (II) Concepts of Value Valuation Date: Usually determined by a specific event. Purpose (gifting, financial reporting, transaction): Valuations performed for one purpose are not necessarily transferable to another purpose. Standard of Value: A legal concept which influences the selection of methods and level of value. Most common include fair value and fair market value. Level of Value: Value can be different depending on the level of value under consideration. Levels of value range from nonmarketable minority positions to strategic control positions. The chart on the next slide highlights the attributes of the different levels. 12

13 Valuation Considerations (III) Levels of Value Chart (source: Mercer Capital website) 13

14 Valuation Considerations (IV) Valuation Approaches Employed in the IM space Income Approach Capitalization Discounted Cash Flow Market Approach Guideline Company Method Guideline Transaction Method What About Rules of Thumb? Application Example 14

15 Valuation Considerations (V) Capitalization of Income Method I. Derive Income Base The goal is to arrive at a normalized level of earnings (usually cash flow), which can be capitalized to derive a value. Non-recurring items should be adjusted out (examples include, gains and losses, extraordinary fees/expenses) Normalizing adjustments should be made (officers compensation restated to market, i.e, replacement value). Question: Is normalizing officers salary appropriate for valuations of minority interests? 15

Normalizing")

16 Valuation Considerations (VI) Capitalization of Income Method II. Determine Discount Rate Equity Cash Flows Discount Using Cost of Equity Components include: (1) the risk-free rate; (2) equity risk premium; (3) size premium; and (4) company-specific risk premium. Two common methods for estimating the cost of equity include the Capital Asset Pricing Model ( CAPM ) and the Build-up (Beta-adjusted or Plain). Cost of equity for investment management firms typically ranges between 10% and 20% (varies depending on size and risk profile of the subject). Debt Free (Invested Capital) Cash Flows Discount Using Weighted Average Cost of Capital (WACC) The required rate of return on all invested capital is the WACC, which is developed by: (1) separately estimating the costs of equity (as discussed above) and debt; and (2) weighting these costs based on an assumed capital structure (using market participants as a guide). 16

.")

17 Valuation Considerations (VII) Capitalization of Income Method III. Estimate Growth Rate Considerations: Should represent cash flow growth rate. General Economic Considerations (i.e., GDP growth). Industry-related Considerations. Company-specific Considerations, i.e., previously discussed value drivers). High-growth companies (due to sustainable competitive advantages) can be valued with a multi-stage growth model. Long-term growth rate is typically in-line with GDP growth, i.e., 3% to 4% 17

can be valued with a multi-stage growth model.")

18 Valuation Considerations (VIII) DCF Method Process is similar to the Capitalization Method Derive cash flow, Determine discount rate Select growth rate Since this method is predicated on the use of a forecast, the accuracy of which is unknown at the time of valuation, it is important to benchmark the assumptions utilized in a DCF analysis against a peer group. Benchmarking typically occurs in the form a ratio analysis. By analyzing ratios, the valuator must determine whether the subject s projections are overly aggressive or conservative relative to the comparison companies. When variances occur, their causes must be identified and addressed appropriately in the valuation, i.e., adjust the cash flows or discount rate as deemed appropriate. 18

19 Valuation Considerations (IX) Guideline Company Method I. Identifying Guideline Companies Primary Considerations Size Business Mix Operating and Financial Metrics (margins, growth rates, capital structure, capital spending requirements) Secondary Considerations Geographic Location Geographic Diversity 19

Secondary Considerations Geographic Location")

20 Valuation Considerations (X) Guideline Company Method (Continued) II. Selecting Multiples Price/Net Income or Cash Flow-Useful when there is a similarity in capital intensity, depreciation methods, and tax rates. Price/Sales-Useful when there is a uniform profit margin in the industry or when there is a strong correlation between Price/Sales and return on sales. Risk: does not account for firm s expense model. Price/AUM Useful when there is a similarity in effective management fee, i.e., revenue/aum and profit levels per dollar of AUM, i.e., net income/aum. More useful for pure play asset managers Not so applicable to trust companies or other business with significant amounts of assets under administration ( AUA ). Enterprise Value ( EV ) Multiples can be utilized instead of equity (price) multiples for each of the above in certain situations, i.e., to mitigate differences in capital intensity, capital structure, and tax rates. 20

21 Valuation Considerations (XI) Guideline Company Method (Continued) III. Applying Multiples Identify key differences between the subject and the guideline company group. Discover if any single guideline public company or subset of guideline public companies is more comparable to the subject; Select a multiple to apply to the subject based on qualitative and quantitative comparisons to the peer group. Must be able to support the selection of each multiple, whether it is a mean, median, or something other than a central tendency measurement. Result is a marketable minority interest value 21

22 Valuation Considerations (XII) Guideline Transaction Method Process is similar to the Guideline Company Method Identify relevant transactions Determine which multiples to utilize Perform qualitative and quantitative comparisons to sample companies Apply multiples based on above analysis Pay attention to level of value (if valuing a controlling position, make sure the comparable transactions were for control positions) Challenges with this method Limited number of transactions Staleness of transactions Data quality issues 22

23 Valuation Considerations (XIII) What About Rules-of -Thumb? Rules-of-Thumb are a short-cut way to arrive at a value, i.e., the average firm in the industry is valued at two times revenues or 5 times cash flow. Rules-of-Thumb fail to take into account (among other items): 1. Differences in effective management fees 2. Profitability 3. Differences in growth rates 4. Quality of AUM, clients As a result of the above, firms of above average quality can be under valued, while firms of below average quality can be over valued. Takeaway: Use with Discretion 23

24 Valuation Considerations (XIV) Other Valuation Considerations Tax Status of Entity Being Valued Non-operating Assets Premiums and Discounts Control Premium Discount for Lack of Control Discount for Non-voting Shares Discount for Lack of Marketability 24

25 Valuation Considerations (XV) The Valuation Gap (diverging perception of value between sellers and buyers) Some Causes for the Valuation Gap Poor Quality AUM/AUA, i.e., low margin Reliance on the skills and contacts of a limited number of individuals High compensation-related expenses Aging client base (draws on accounts leads to declining AUM) Ways to Bridge the Valuation Gap Reduce reliance on the principal (take your name off the door) Invest in the business (take reasonable compensation and leave the excess cash in the business for reinvestment) Train employees to be business generators and relationship managers Grow AUM through new products, markets, client demographic, etc. 25

26 Valuation Considerations (XVI) NOW WHAT? What types of transactions take place in the industry and how are deals structured? 26

27 PART 3: The Art of the Deal 27

28 The Art of the Deal (I) Reasons to Sell Grow Assets Increase Marketing/Distribution Cost Reduction Diversify Risk Reasons to Postpone Selling Temporarily Depressed Profitability Partnership Dissent Issues Extraneous Market Conditions (stage in economic cycle, investor perceptions, etc.) 28

29 The Art of the Deal (II) Deal Types & Typical Structures I. External Transactions External Sale Appropriate when internal candidates to purchase the business have not been identified. Since an external sale is usually strategic, it often will yield the highest price to the seller. Typical Structure Buyer pays seller a cash amount at closing. The balance is paid via earn-out, typically over three to five years. Earn-out payments are collateralized by the cash flows of the business. Sellers often receive a transition consulting contract if they plan to leave within the first couple of years. 29

30 The Art of the Deal (III) Deal Types & Typical Structures I. External Transactions (Continued) External Merger Usually done when the benefit of merging two firms outweighs the costs of doing so (benefits accrue to the merged firm in the form of higher margins). A selling firm might choose this option if some or all of the partners wish to stay with the merged firm. Typical Structure Often a cashless transaction The merged firms have their firms valued prior to the transaction and the merge their equity into a new organization. Ownership is divided on a pro-rata basis based on a host of factors, but primarily includes the pre-deal valuation and expected growth rates. Often there will be a valuation reset after a couple of years if adjustments are necessary, i.e., one of the firms is under-performing. 30

31 The Art of the Deal (IV) Deal Types & Typical Structures II. Internal Transactions Hire or Acquire Successor Usually assumes that there are no partners or junior advisors internally who would represent good candidates to assume control of the business. Typical Structure The successor typically purchases shares in stages. This is done as a hedge in case the new advisor is not compatible with the remaining employees or if he/she is unproven. Since the founder usually stays for a while, the deal structure will usually include a base salary plus commission. When ready to exit completely, there is usually a buyout formula in place to purchase the founders remaining equity after they depart. 31

32 The Art of the Deal (V) Deal Types & Typical Structures II. Internal Transactions (Continued) Sale to Internal Successor Can preserve the firms legacy, allow owners to gradually transfer control, and often means less change for the firm and its clients during transition. Transitioning ownership to an internal successor can take several years (5 to 10) to completely take place. Considerations Selling internally reduces the addressable market for the shares. This can result in lower selling prices and higher valuation discounts. Internal successors may have less access to capital relative to outside buyers. 32

33 The Art of the Deal: (Appendix) Source of Chart: Transition Planning, Charles Schwab Advisory Services 33

34 WRAP-UP Questions? 34

NACVA. National Association of Certified Valuators and Analysts

NACVA National Association of Certified Valuators and Analysts The Core Body of Knowledge for Business Valuations All rights reserved. No part of this work covered by the copyrights herein may be reproduced

NACVA National Association of Certified Valuators and Analysts The Core Body of Knowledge for Business Valuations All rights reserved. No part of this work covered by the copyrights herein may be reproduced

ANALYSIS AND MANAGEMENT

ANALYSIS AND MANAGEMENT T H 1RD CANADIAN EDITION W. SEAN CLEARY Queen's University CHARLES P. JONES North Carolina State University JOHN WILEY & SONS CANADA, LTD. CONTENTS PART ONE Background CHAPTER 1

ANALYSIS AND MANAGEMENT T H 1RD CANADIAN EDITION W. SEAN CLEARY Queen's University CHARLES P. JONES North Carolina State University JOHN WILEY & SONS CANADA, LTD. CONTENTS PART ONE Background CHAPTER 1

American Society of Appraisers. ASA Business Valuation Standards

American Society of Appraisers Business Valuation Standards This release of the approved Business Valuation Standards of the American Society of Appraisers contains all standards approved through February,

American Society of Appraisers Business Valuation Standards This release of the approved Business Valuation Standards of the American Society of Appraisers contains all standards approved through February,

COMMUNICATING THE VALUATION REPORT

COMMUNICATING THE VALUATION REPORT Dave Diehl, CFA Prairie Capital Advisors, Inc. ddiehl@prairiecap.com Chieoke Moore, CPA Prairie Capital Advisors, Inc. cmoore@prairiecap.com OUTLINE OF TODAY S PRESENTATION

COMMUNICATING THE VALUATION REPORT Dave Diehl, CFA Prairie Capital Advisors, Inc. ddiehl@prairiecap.com Chieoke Moore, CPA Prairie Capital Advisors, Inc. cmoore@prairiecap.com OUTLINE OF TODAY S PRESENTATION

NIKE Case Study Solutions

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

NIKE Case Study Solutions Professor Corwin This case study includes several problems related to the valuation of Nike. We will work through these problems throughout the course to demonstrate some of the

A Guide to Valuing Your Financial Advisory Practice

A Guide to Valuing Your Financial Advisory Practice A Guide to Valuing Your Financial Advisory Practice 1 If you re one of the many baby-boomer advisors in the financial services industry starting to think

A Guide to Valuing Your Financial Advisory Practice A Guide to Valuing Your Financial Advisory Practice 1 If you re one of the many baby-boomer advisors in the financial services industry starting to think

Clackamas County. Office of the Treasurer. Investment Policy. 2051 Kaen Rd, #430. Oregon City, Oregon 97045 503-742-5995 FAX 503-742-5996

Clackamas County Office of the Treasurer Investment Policy 2051 Kaen Rd, #430 Oregon City, Oregon 97045 503-742-5995 FAX 503-742-5996 shariand@co.clackamas.or.us 6/4/12 1 I. Objectives: Clackamas County

Clackamas County Office of the Treasurer Investment Policy 2051 Kaen Rd, #430 Oregon City, Oregon 97045 503-742-5995 FAX 503-742-5996 shariand@co.clackamas.or.us 6/4/12 1 I. Objectives: Clackamas County

CONSIDERATIONS IN BUYING AND SELLING A BUSINESS

CONSIDERATIONS IN BUYING AND SELLING A BUSINESS David H. Pettit, Esq. Feil, Pettit & Williams, PLC Charlottesville, VA I. Ownership A. Are the owners of sound mind and in agreement? B. Can the transaction

CONSIDERATIONS IN BUYING AND SELLING A BUSINESS David H. Pettit, Esq. Feil, Pettit & Williams, PLC Charlottesville, VA I. Ownership A. Are the owners of sound mind and in agreement? B. Can the transaction

Keyware Technologies N.V- valuation highlights

Keyware Technologies N.V- valuation highlights This memorandum brings a short summary of Keyware Technologies N.V's (hereinafter 'Keyware' or the 'Company') valuation report as of December 31, 2014. This

Keyware Technologies N.V- valuation highlights This memorandum brings a short summary of Keyware Technologies N.V's (hereinafter 'Keyware' or the 'Company') valuation report as of December 31, 2014. This

Business Value Drivers

Business Value Drivers by Kurt Havnaer, CFA, Business Analyst white paper A Series of Reports on Quality Growth Investing jenseninvestment.com Price is what you pay, value is what you get. 1 Introduction

Business Value Drivers by Kurt Havnaer, CFA, Business Analyst white paper A Series of Reports on Quality Growth Investing jenseninvestment.com Price is what you pay, value is what you get. 1 Introduction

Business Valuation and Exit Planning. Aaron J. Pryor, CFA, ASA

Business Valuation and Exit Planning Aaron J. Pryor, CFA, ASA Phases of a Business Valuation Assignment Define the valuation assignment What exactly is the subject of the valuation What is the purpose

Business Valuation and Exit Planning Aaron J. Pryor, CFA, ASA Phases of a Business Valuation Assignment Define the valuation assignment What exactly is the subject of the valuation What is the purpose

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

Fixed Income Liquidity in a Rising Rate Environment

Fixed Income Liquidity in a Rising Rate Environment 2 Executive Summary Ò Fixed income market liquidity has declined, causing greater concern about prospective liquidity in a potential broad market sell-off

Fixed Income Liquidity in a Rising Rate Environment 2 Executive Summary Ò Fixed income market liquidity has declined, causing greater concern about prospective liquidity in a potential broad market sell-off

Charles Carroll Financial Partners, LLC INVESTMENT ADVISORY CONTRACT

Charles Carroll Financial Partners, LLC INVESTMENT ADVISORY CONTRACT Charles Carroll Financial Partners Investment Advisory Contract 03-13 1 INVESTMENT AGREEMENT The undersigned ( Client ), being duly

Charles Carroll Financial Partners, LLC INVESTMENT ADVISORY CONTRACT Charles Carroll Financial Partners Investment Advisory Contract 03-13 1 INVESTMENT AGREEMENT The undersigned ( Client ), being duly

Investing in International Financial Markets

APPENDIX 3 Investing in International Financial Markets http:// Visit http://money.cnn.com for current national and international market data and analyses. The trading of financial assets (such as stocks

APPENDIX 3 Investing in International Financial Markets http:// Visit http://money.cnn.com for current national and international market data and analyses. The trading of financial assets (such as stocks

ALLOCATION STRATEGIES A, C, & I SHARES PROSPECTUS August 1, 2015

ALLOCATION STRATEGIES A, C, & I SHARES PROSPECTUS August 1, 2015 Investment Adviser: RidgeWorth Investments A Shares C Shares I Shares Aggressive Growth Allocation Strategy SLAAX CLVLX CVMGX Conservative

ALLOCATION STRATEGIES A, C, & I SHARES PROSPECTUS August 1, 2015 Investment Adviser: RidgeWorth Investments A Shares C Shares I Shares Aggressive Growth Allocation Strategy SLAAX CLVLX CVMGX Conservative

VALUATION JC PENNEY (NYSE:JCP)

") VALUATION JC PENNEY (NYSE:JCP) Prepared for Dr. K.C. Chen California State University, Fresno Prepared by Sicilia Sendjaja Finance 129-Student Investment Funds December 15 th, 2009 California State University,

VALUATION JC PENNEY (NYSE:JCP) Prepared for Dr. K.C. Chen California State University, Fresno Prepared by Sicilia Sendjaja Finance 129-Student Investment Funds December 15 th, 2009 California State University,

Wealth Creation Planning

Wealth Creation Planning A better way to own Life Insurance! Life insurance is the most effective way to protect against the financial risk and strain of a premature death. However, large or long term

Wealth Creation Planning A better way to own Life Insurance! Life insurance is the most effective way to protect against the financial risk and strain of a premature death. However, large or long term

Succession Planning. Succession Planning. James F. Weber, CPA, CGMA Managing Member

James F. Weber, CPA, CGMA Managing Member This session is eligible for 1 Continuing Education Hour and 1 Contact Hour. To earn these hours you must: Have your badge scanned at the door Attend 90% of this

James F. Weber, CPA, CGMA Managing Member This session is eligible for 1 Continuing Education Hour and 1 Contact Hour. To earn these hours you must: Have your badge scanned at the door Attend 90% of this

Moss Adams Introduction to ESOPs

Moss Adams Introduction to ESOPs Looking for an exit strategy Have you considered an ESOP? Since 1984, we have performed over 2,000 Employee Stock Ownership Plan (ESOP) valuations for companies with as

Moss Adams Introduction to ESOPs Looking for an exit strategy Have you considered an ESOP? Since 1984, we have performed over 2,000 Employee Stock Ownership Plan (ESOP) valuations for companies with as

How To Value An Asset

Business Valuation: How to Make the Most of Your Business Pooja Gardemal, CPA/ABV Vice President Business Valuation & Economic Analysis 1 About is a global consulting firm with offices in the U.S. and

Business Valuation: How to Make the Most of Your Business Pooja Gardemal, CPA/ABV Vice President Business Valuation & Economic Analysis 1 About is a global consulting firm with offices in the U.S. and

The Master Statement of Investment Policies and Objectives of The Lower Colorado River Authority Retirement Plan and Trust. Amended June 16, 2015

The Master Statement of Investment Policies and Objectives of The Lower Colorado River Authority Retirement Plan and Trust Amended June 16, 2015 Introduction The Lower Colorado River Authority ( LCRA )

The Master Statement of Investment Policies and Objectives of The Lower Colorado River Authority Retirement Plan and Trust Amended June 16, 2015 Introduction The Lower Colorado River Authority ( LCRA )

International Glossary of Business Valuation Terms*

40 Statement on Standards for Valuation Services No. 1 APPENDIX B International Glossary of Business Valuation Terms* To enhance and sustain the quality of business valuations for the benefit of the profession

40 Statement on Standards for Valuation Services No. 1 APPENDIX B International Glossary of Business Valuation Terms* To enhance and sustain the quality of business valuations for the benefit of the profession

Manning & Napier Earnings Release Supplement. For the period ended September 30, 2015

Manning & Napier Earnings Release Supplement For the period ended September 30, 2015 Forward Looking Statements This presentation contains forward-looking statements. Such statements can be identified

Manning & Napier Earnings Release Supplement For the period ended September 30, 2015 Forward Looking Statements This presentation contains forward-looking statements. Such statements can be identified

A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157)

") A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157) By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions May 2010 201 Edgewater

A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157) By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions May 2010 201 Edgewater

onetravel@aol.com 954-540-3697

onetravel@aol.com 954-540-3697 Valuation Principles Good Afternoon! I want to thank all of you who have attended our round table discussion in regards to valuations. Having an independent valuation can

onetravel@aol.com 954-540-3697 Valuation Principles Good Afternoon! I want to thank all of you who have attended our round table discussion in regards to valuations. Having an independent valuation can

10/22/2014. Over the next decade, an estimated 12,000 to 16,000 of the nation s 315,000 advisors are projected to retire each year.

1. Financial Advisor and Acquisition Statistics 2. The Essentials of a Practice Acquisition 3. Seller s Guidelines and Checklist 4. Practice Valuations and Acquisition Structures 5. Succession and Continuity

1. Financial Advisor and Acquisition Statistics 2. The Essentials of a Practice Acquisition 3. Seller s Guidelines and Checklist 4. Practice Valuations and Acquisition Structures 5. Succession and Continuity

The cost of capital. A reading prepared by Pamela Peterson Drake. 1. Introduction

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

The cost of capital A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction... 1 2. Determining the proportions of each source of capital that will be raised... 3 3. Estimating the marginal

American Society of Appraisers. ASA Business Valuation Standards

American Society of Appraisers ASA Business Valuation Standards This release of the approved of the American Society of Appraisers contains all standards approved through November 2009, and is to be used

American Society of Appraisers ASA Business Valuation Standards This release of the approved of the American Society of Appraisers contains all standards approved through November 2009, and is to be used

Davis New York Venture Fund

Davis New York Venture Fund Price Is What You Pay, Value Is What You Get Over 40 Years of Reliable Investing Price Is What You Pay, Value Is What You Get Over 60 years investing in the equity markets has

Davis New York Venture Fund Price Is What You Pay, Value Is What You Get Over 40 Years of Reliable Investing Price Is What You Pay, Value Is What You Get Over 60 years investing in the equity markets has

--- FOR IMMEDIATE RELEASE ---

--- FOR IMMEDIATE RELEASE --- TIBURON RELEASES UPDATED RESEARCH REPORT ON TRENDS IN SUCCESSION PLANNING, FIRM VALUATIONS, & THE GROWING ACQUISITION MARKET FOR FINANCIAL ADVISORS -- Report addresses the

--- FOR IMMEDIATE RELEASE --- TIBURON RELEASES UPDATED RESEARCH REPORT ON TRENDS IN SUCCESSION PLANNING, FIRM VALUATIONS, & THE GROWING ACQUISITION MARKET FOR FINANCIAL ADVISORS -- Report addresses the

Halter Ferguson Financial, Inc. 7702 Woodland Drive Indianapolis, Indiana 46278. Suite 150 317-875-0202. http://www.hffinancial.com.

Halter Ferguson Financial, Inc. 7702 Woodland Drive Indianapolis, Indiana 46278 Suite 150 317-875-0202 http://www.hffinancial.com March 14, 2011 This brochure provides information about the qualifications

Halter Ferguson Financial, Inc. 7702 Woodland Drive Indianapolis, Indiana 46278 Suite 150 317-875-0202 http://www.hffinancial.com March 14, 2011 This brochure provides information about the qualifications

AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT REFERENCE FOR PRIVATE INVESTORS

AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT REFERENCE FOR PRIVATE INVESTORS Phil Thompson Business Lawyer, Corporate Counsel www.thompsonlaw.ca Rules of thumb and financial analysis

AN INTRODUCTION TO REAL ESTATE INVESTMENT ANALYSIS: A TOOL KIT REFERENCE FOR PRIVATE INVESTORS Phil Thompson Business Lawyer, Corporate Counsel www.thompsonlaw.ca Rules of thumb and financial analysis

Business Valuation Report

Certified Business Appraisals, LLC Business Valuation Report Prepared for: John Doe Client Business, Inc. 1 Market Way Your Town, CA January 1, 2016 1 Market Street Suite 100 Anytown, CA 95401 Web: www.yourdomain.com

Certified Business Appraisals, LLC Business Valuation Report Prepared for: John Doe Client Business, Inc. 1 Market Way Your Town, CA January 1, 2016 1 Market Street Suite 100 Anytown, CA 95401 Web: www.yourdomain.com

Practice Bulletin No. 2

Practice Bulletin No. 2 INTERNATIONAL GLOSSARY OF BUSINESS VALUATION TERMS To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified

Practice Bulletin No. 2 INTERNATIONAL GLOSSARY OF BUSINESS VALUATION TERMS To enhance and sustain the quality of business valuations for the benefit of the profession and its clientele, the below identified

INTERVIEWS - FINANCIAL MODELING

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

420 W. 118th Street, Room 420 New York, NY 10027 P: 212-854-4613 F: 212-854-6190 www.sipa.columbia.edu/ocs INTERVIEWS - FINANCIAL MODELING Basic valuation concepts are among the most popular technical

L2: Alternative Asset Management and Performance Evaluation

L2: Alternative Asset Management and Performance Evaluation Overview of asset management from ch 6 (ST) Performance Evaluation of Investment Portfolios from ch24 (BKM) 1 Asset Management Asset Management

L2: Alternative Asset Management and Performance Evaluation Overview of asset management from ch 6 (ST) Performance Evaluation of Investment Portfolios from ch24 (BKM) 1 Asset Management Asset Management

Impairment Testing Procedures and Pitfalls

Audio Conference Dial-in Number: 877.691.9300; Access Code: 4321206 Impairment Testing Procedures and Pitfalls November 3, 2009 Presenters: Cory J. Thompson, CFA, CIRA Ryan A. Gandre, CFA Moderator: Jay

Audio Conference Dial-in Number: 877.691.9300; Access Code: 4321206 Impairment Testing Procedures and Pitfalls November 3, 2009 Presenters: Cory J. Thompson, CFA, CIRA Ryan A. Gandre, CFA Moderator: Jay

Valuing the Business

Valuing the Business 1. Introduction After deciding to buy or sell a business, the subject of "how much" becomes important. Determining the value of a business is one of the most difficult aspects of any

Valuing the Business 1. Introduction After deciding to buy or sell a business, the subject of "how much" becomes important. Determining the value of a business is one of the most difficult aspects of any

for Analysing Listed Private Equity Companies

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

Solving for Perpetuation Financing: The Next Generation ESOP

Solving for Perpetuation Financing: The Next Generation ESOP Seven times eight times nine times or more times As the largest brokers have returned to the M&A market with a vengeance, we have witnessed

Solving for Perpetuation Financing: The Next Generation ESOP Seven times eight times nine times or more times As the largest brokers have returned to the M&A market with a vengeance, we have witnessed

)WILEY A John Wiley &. Sons, Ltd., Publication

WILEY A John Wiley &. Sons, Ltd., Publication") Mastering Illiquidity Risk Management for Portfolios of Limited Partnership Funds Peter Cornelius Christian Diller Didier Guennoc Thomas Meyer )WILEY A John Wiley &. Sons, Ltd., Publication Foreword Acknowledgements

Mastering Illiquidity Risk Management for Portfolios of Limited Partnership Funds Peter Cornelius Christian Diller Didier Guennoc Thomas Meyer )WILEY A John Wiley &. Sons, Ltd., Publication Foreword Acknowledgements

Advanced Strategies for Managing Volatility

Advanced Strategies for Managing Volatility Description: Investment portfolios are generally exposed to volatility through company-specific risk and through market risk. Long-term investors can reduce

Advanced Strategies for Managing Volatility Description: Investment portfolios are generally exposed to volatility through company-specific risk and through market risk. Long-term investors can reduce

Introduction to Financial Models for Management and Planning

CHAPMAN &HALL/CRC FINANCE SERIES Introduction to Financial Models for Management and Planning James R. Morris University of Colorado, Denver U. S. A. John P. Daley University of Colorado, Denver U. S.

CHAPMAN &HALL/CRC FINANCE SERIES Introduction to Financial Models for Management and Planning James R. Morris University of Colorado, Denver U. S. A. John P. Daley University of Colorado, Denver U. S.

3/22/2011. Financing an ESOP Transaction. Table of Contents. I. The Leveraged ESOP Transaction. John L. Miscione Managing Director

Presented by John L. Miscione Managing Director Table of Contents I. The Leveraged ESOP Transaction II. ESOP Tax Benefits III. Debt Capacity IV. Financing Markets and Terms V. The Lender s Perspective

Presented by John L. Miscione Managing Director Table of Contents I. The Leveraged ESOP Transaction II. ESOP Tax Benefits III. Debt Capacity IV. Financing Markets and Terms V. The Lender s Perspective

Master Limited Partnerships (MLPs):

:") Master Limited Partnerships (MLPs): Frequently Asked Questions Yorkville Capital Management LLC www.yorkvillecapital.com 950 Third Avenue, 23 rd Floor New York, NY 10022 (212) 755-1970 Table of Contents

Master Limited Partnerships (MLPs): Frequently Asked Questions Yorkville Capital Management LLC www.yorkvillecapital.com 950 Third Avenue, 23 rd Floor New York, NY 10022 (212) 755-1970 Table of Contents

Business Valuation Discounts and Premiums

Business Valuation Discounts and Premiums Second Edition SHANNON P. PRATT WILEY John Wiley & Sons, Inc. Contents List of Exhibits xv About the Author xix About the Contributing Authors xxi Foreword Preface

Business Valuation Discounts and Premiums Second Edition SHANNON P. PRATT WILEY John Wiley & Sons, Inc. Contents List of Exhibits xv About the Author xix About the Contributing Authors xxi Foreword Preface

Measuring performance Update to Insurance Key Performance Indicators

Measuring performance Update to Insurance Key Performance Indicators John Hele Member of Executive Board and CFO of ING Group Madrid 19 September 2008 www.ing.com Agenda Performance Indicators: Background

Measuring performance Update to Insurance Key Performance Indicators John Hele Member of Executive Board and CFO of ING Group Madrid 19 September 2008 www.ing.com Agenda Performance Indicators: Background

Clients per professional. Over $1B 45 $750MM $1B 48 $500MM $750MM 45 $250MM $500MM 47. Over $1B 38 $750MM $1B 38 $500MM $750MM 35

The power of the independent advice business $123 $750MM $1B $91 model AUM per (millions) $500MM $750MM $75 Clients per 45 $750MM $1B 48 $500MM $750MM 45 $250MM $500MM $72 $250MM $500MM 47 More than one-third

The power of the independent advice business $123 $750MM $1B $91 model AUM per (millions) $500MM $750MM $75 Clients per 45 $750MM $1B 48 $500MM $750MM 45 $250MM $500MM $72 $250MM $500MM 47 More than one-third

Copyright 2015, American Institute of Certified Public Accountants, Inc. All Rights Re... Page 1 of 59 STATEMENTS ON STANDARDS FOR VALUATION SERVICES

Copyright 2015, American Institute of Certified Public Accountants, Inc. All Rights Re... Page 1 of 59 Valuation Services VS Section STATEMENTS ON STANDARDS FOR VALUATION SERVICES VS Section 100 Valuation

Copyright 2015, American Institute of Certified Public Accountants, Inc. All Rights Re... Page 1 of 59 Valuation Services VS Section STATEMENTS ON STANDARDS FOR VALUATION SERVICES VS Section 100 Valuation

Equity Market Risk Premium Research Summary. 12 April 2016

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

Equity Market Risk Premium Research Summary 12 April 2016 Introduction welcome If you are reading this, it is likely that you are in regular contact with KPMG on the topic of valuations. The goal of this

INVESTMENT POLICY. The Committee will meet regularly to review performance, policy, procedures and legislation.

INVESTMENT POLICY I. AUTHORITY The Constitution and Laws of the State of Missouri authorize the Missouri State Treasurer to have custody of all state monies and to invest said monies not needed for the

INVESTMENT POLICY I. AUTHORITY The Constitution and Laws of the State of Missouri authorize the Missouri State Treasurer to have custody of all state monies and to invest said monies not needed for the

ETF Total Cost Analysis in Action

Morningstar ETF Research ETF Total Cost Analysis in Action Authors: Paul Justice, CFA, Director of ETF Research, North America Michael Rawson, CFA, ETF Analyst 2 ETF Total Cost Analysis in Action Exchange

Morningstar ETF Research ETF Total Cost Analysis in Action Authors: Paul Justice, CFA, Director of ETF Research, North America Michael Rawson, CFA, ETF Analyst 2 ETF Total Cost Analysis in Action Exchange

Compensation: How RIA firms are attracting and retaining top-tier talent

Compensation: How RIA firms are attracting and retaining top-tier talent Results from the 2014 RIA Benchmarking Study from Charles Schwab As the RIA industry has grown and matured, individual advisory

Compensation: How RIA firms are attracting and retaining top-tier talent Results from the 2014 RIA Benchmarking Study from Charles Schwab As the RIA industry has grown and matured, individual advisory

FAQ. (Continued on page 2) An Investment Advisory Firm

An Investment Advisory Firm") FAQ An Investment Advisory Firm What is QASH Flow Advantage? It is a time-tested model that includes three strategic components: A portfolio of carefully selected Exchange-Traded Funds (ETFs) for diversification

FAQ An Investment Advisory Firm What is QASH Flow Advantage? It is a time-tested model that includes three strategic components: A portfolio of carefully selected Exchange-Traded Funds (ETFs) for diversification

INTERACTIVE DATA REPORTS FOURTH-QUARTER AND FULL- YEAR 2014 RESULTS

Press Release INTERACTIVE DATA REPORTS FOURTH-QUARTER AND FULL- YEAR 2014 RESULTS New York February 12, 2015 Interactive Data Corporation today reported its financial results for the fourth quarter and

Press Release INTERACTIVE DATA REPORTS FOURTH-QUARTER AND FULL- YEAR 2014 RESULTS New York February 12, 2015 Interactive Data Corporation today reported its financial results for the fourth quarter and

BASKET A collection of securities. The underlying securities within an ETF are often collectively referred to as a basket

Glossary: The ETF Portfolio Challenge Glossary is designed to help familiarize our participants with concepts and terminology closely associated with Exchange- Traded Products. For more educational offerings,

Glossary: The ETF Portfolio Challenge Glossary is designed to help familiarize our participants with concepts and terminology closely associated with Exchange- Traded Products. For more educational offerings,

What is the fair market

3 Construction Company Valuation Primer Fred Shelton, Jr., CPA, MBA, CVA EXECUTIVE SUMMARY This article explores the methods and techniques used in construction company valuation. Using an illustrative

3 Construction Company Valuation Primer Fred Shelton, Jr., CPA, MBA, CVA EXECUTIVE SUMMARY This article explores the methods and techniques used in construction company valuation. Using an illustrative

Common Denominator Relationships: Aligning the Franchisor and Franchisee Objectives.

Common Denominator Relationships: Aligning the Franchisor and Franchisee Objectives. Prepared by: Joe Fahey, CFA, Senior Director of Planning, Business Advisory Services, Wells Fargo Bank. In this white

Common Denominator Relationships: Aligning the Franchisor and Franchisee Objectives. Prepared by: Joe Fahey, CFA, Senior Director of Planning, Business Advisory Services, Wells Fargo Bank. In this white

SPDR Wells Fargo Preferred Stock ETF

SPDR Wells Fargo Preferred Stock ETF Summary Prospectus-October 31, 2015 PSK (NYSE Ticker) Before you invest in the SPDR Wells Fargo Preferred Stock ETF (the Fund ), you may want to review the Fund's prospectus

SPDR Wells Fargo Preferred Stock ETF Summary Prospectus-October 31, 2015 PSK (NYSE Ticker) Before you invest in the SPDR Wells Fargo Preferred Stock ETF (the Fund ), you may want to review the Fund's prospectus

MBA (3rd Sem) 2013-14 MBA/29/FM-302/T/ODD/13-14

2013-14 MBA/29/FM-302/T/ODD/13-14") Full Marks : 70 MBA/29/FM-302/T/ODD/13-14 2013-14 MBA (3rd Sem) Paper Name : Corporate Finance Paper Code : FM-302 Time : 3 Hours The figures in the right-hand margin indicate marks. Candidates are required

Full Marks : 70 MBA/29/FM-302/T/ODD/13-14 2013-14 MBA (3rd Sem) Paper Name : Corporate Finance Paper Code : FM-302 Time : 3 Hours The figures in the right-hand margin indicate marks. Candidates are required

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

NorthCoast Investment Advisory Team 203.532.7000 info@northcoastam.com NORTHCOAST ASSET MANAGEMENT An established leader in the field of tactical investment management, specializing in quantitative research

DEPOSITION QUESTIONS FOR STEVEN GARCIA

DEPOSITION QUESTIONS FOR STEVEN GARCIA When you see a box, it means that I am telling you either the direction that I want to go in or what I expect his answer to be. BACKGROUND AND QUALIFICATIONS (BIOGRAPHICAL

DEPOSITION QUESTIONS FOR STEVEN GARCIA When you see a box, it means that I am telling you either the direction that I want to go in or what I expect his answer to be. BACKGROUND AND QUALIFICATIONS (BIOGRAPHICAL

The buying and selling of a financial planning business

The buying and selling of a financial planning business Gavin Jordan, Partner, Ernst & Young LLP 10 September 2010 Disclaimer This publication contains information in summary form and is therefore intended

The buying and selling of a financial planning business Gavin Jordan, Partner, Ernst & Young LLP 10 September 2010 Disclaimer This publication contains information in summary form and is therefore intended

BRANDES. Brandes Core Plus Fixed Income Fund Class A BCPAX Class E BCPEX Class I BCPIX. Brandes Credit Focus Yield Fund Class A BCFAX Class I BCFIX

BRANDES Brandes Core Plus Fixed Income Fund Class A BCPAX Class E BCPEX Class I BCPIX Brandes Credit Focus Yield Fund Class A BCFAX Class I BCFIX Prospectus January 30, 2015 The U.S. Securities and Exchange

BRANDES Brandes Core Plus Fixed Income Fund Class A BCPAX Class E BCPEX Class I BCPIX Brandes Credit Focus Yield Fund Class A BCFAX Class I BCFIX Prospectus January 30, 2015 The U.S. Securities and Exchange

Purpose of Selling Stocks Short JANUARY 2007 NUMBER 5

An Overview of Short Stock Selling An effective short stock selling strategy provides an important hedge to a long portfolio and allows hedge fund managers to reduce sector and portfolio beta. Short selling

An Overview of Short Stock Selling An effective short stock selling strategy provides an important hedge to a long portfolio and allows hedge fund managers to reduce sector and portfolio beta. Short selling

Market Linked Certificates of Deposit

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

Market Linked Certificates of Deposit This material was prepared by Wells Fargo Securities, LLC, a registered brokerdealer and separate non-bank affiliate of Wells Fargo & Company. This material is not

Appendix B Weighted Average Cost of Capital

Appendix B Weighted Average Cost of Capital The inclusion of cost of money within cash flow analyses in engineering economics and life-cycle costing is a very important (and in many cases dominate) contributing

Appendix B Weighted Average Cost of Capital The inclusion of cost of money within cash flow analyses in engineering economics and life-cycle costing is a very important (and in many cases dominate) contributing

Overview of Business Valuations

Overview of Business Valuations By CA Niketa Agarwal Last few years have not been encouraging for the global economy due to crisis and slow recovery in several large and developed countries. India experienced

Overview of Business Valuations By CA Niketa Agarwal Last few years have not been encouraging for the global economy due to crisis and slow recovery in several large and developed countries. India experienced

Cheap Stock: Final Draft of the AICPA Practice Aid

Cheap Stock: Final Draft of the AICPA Practice Aid Ryan A. Gandre, CFA rgandre@srr.com Introduction n n n Stock options and other forms of stock-based compensation are frequently issued to company officers

Cheap Stock: Final Draft of the AICPA Practice Aid Ryan A. Gandre, CFA rgandre@srr.com Introduction n n n Stock options and other forms of stock-based compensation are frequently issued to company officers

Financial & Valuation Modeling Boot Camp

TARGET AUDIENCE Overview 3-day intensive training program where trainees learn financial & valuation modeling in Excel using in a hands-on, case-study approach. The modeling methodologies covered include:

TARGET AUDIENCE Overview 3-day intensive training program where trainees learn financial & valuation modeling in Excel using in a hands-on, case-study approach. The modeling methodologies covered include:

Nine Questions Every ETF Investor Should Ask Before Investing

Nine Questions Every ETF Investor Should Ask Before Investing UnderstandETFs.org Copyright 2012 by the Investment Company Institute. All rights reserved. ICI permits use of this publication in any way,

Nine Questions Every ETF Investor Should Ask Before Investing UnderstandETFs.org Copyright 2012 by the Investment Company Institute. All rights reserved. ICI permits use of this publication in any way,

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

RevenueShares ETF Trust

RevenueShares ETF Trust SUMMARY PROSPECTUS NOVEMBER 3, 2015 RevenueShares Global Growth Fund This summary prospectus is designed to provide investors with key fund information in a clear and concise format.

RevenueShares ETF Trust SUMMARY PROSPECTUS NOVEMBER 3, 2015 RevenueShares Global Growth Fund This summary prospectus is designed to provide investors with key fund information in a clear and concise format.

Understanding Leveraged Exchange Traded Funds AN EXPLORATION OF THE RISKS & BENEFITS

Understanding Leveraged Exchange Traded Funds AN EXPLORATION OF THE RISKS & BENEFITS Direxion Shares Leveraged Exchange-Traded Funds (ETFs) are daily funds that provide 200% or 300% leverage and the ability

Understanding Leveraged Exchange Traded Funds AN EXPLORATION OF THE RISKS & BENEFITS Direxion Shares Leveraged Exchange-Traded Funds (ETFs) are daily funds that provide 200% or 300% leverage and the ability

Mutual Fund Investing Exam Study Guide

Mutual Fund Investing Exam Study Guide This document contains the questions that will be included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

Mutual Fund Investing Exam Study Guide This document contains the questions that will be included in the final exam, in the order that they will be asked. When you have studied the course materials, reviewed

Evaluating Target Date Funds. 2003 2013 Multnomah Group, Inc. All Rights Reserved.

2003 2013 Multnomah Group, Inc. All Rights Reserved. Scott Cameron, CFA Scott is the Chief Investment Officer for the Multnomah Group and a Founding Principal of the firm. In that role, Scott leads Multnomah

2003 2013 Multnomah Group, Inc. All Rights Reserved. Scott Cameron, CFA Scott is the Chief Investment Officer for the Multnomah Group and a Founding Principal of the firm. In that role, Scott leads Multnomah

Your Guide to Profit Guard

Dear Profit Master, Congratulations for taking the next step in improving the profitability and efficiency of your company! Profit Guard will provide you with comparative statistical and graphical measurements

Dear Profit Master, Congratulations for taking the next step in improving the profitability and efficiency of your company! Profit Guard will provide you with comparative statistical and graphical measurements

Brown Advisory Strategic Bond Fund Class/Ticker: Institutional Shares / (Not Available for Sale)

") Summary Prospectus October 30, 2015 Brown Advisory Strategic Bond Fund Class/Ticker: Institutional Shares / (Not Available for Sale) Before you invest, you may want to review the Fund s Prospectus, which

Summary Prospectus October 30, 2015 Brown Advisory Strategic Bond Fund Class/Ticker: Institutional Shares / (Not Available for Sale) Before you invest, you may want to review the Fund s Prospectus, which

3 BUSINESS ACCOUNTING STANDARD,,INCOME STATEMENT I. GENERAL PROVISIONS

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 3 BUSINESS ACCOUNTING STANDARD,,INCOME STATEMENT

APPROVED by Resolution No. 1 of 18 December 2003 of the Standards Board of the Public Establishment the Institute of Accounting of the Republic of Lithuania 3 BUSINESS ACCOUNTING STANDARD,,INCOME STATEMENT

Financial Markets and Institutions Abridged 10 th Edition

Financial Markets and Institutions Abridged 10 th Edition by Jeff Madura 1 23 Mutual Fund Operations Chapter Objectives provide a background on mutual funds describe the various types of stock and bond

Financial Markets and Institutions Abridged 10 th Edition by Jeff Madura 1 23 Mutual Fund Operations Chapter Objectives provide a background on mutual funds describe the various types of stock and bond

PureFunds ISE Cyber Security ETF (the Fund ) June 18, 2015. Supplement to the Summary Prospectus dated November 7, 2014

June 18, 2015. Supplement to the Summary Prospectus dated November 7, 2014") PureFunds ISE Cyber Security ETF (the Fund ) June 18, 2015 Supplement to the Summary Prospectus dated November 7, 2014 Effective immediately, Ernesto Tong, CFA, Managing Director of Penserra Capital Management,

PureFunds ISE Cyber Security ETF (the Fund ) June 18, 2015 Supplement to the Summary Prospectus dated November 7, 2014 Effective immediately, Ernesto Tong, CFA, Managing Director of Penserra Capital Management,

CONTACTS: PRESS RELATIONS BETSY CASTENIR (212) 339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS

339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS") FOR IMMEDIATE RELEASE CONTACTS: PRESS RELATIONS BETSY CASTENIR (212) 339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS NET INCOME $84 Million in Q1 04 (+28%

FOR IMMEDIATE RELEASE CONTACTS: PRESS RELATIONS BETSY CASTENIR (212) 339-3424 INVESTOR RELATIONS ROBERT TUCKER (212) 339-0861 FSA HOLDINGS FIRST QUARTER 2004 RESULTS NET INCOME $84 Million in Q1 04 (+28%

METHODS OF VALUATION FOR MERGERS AND ACQUISITIONS

Graduate School of Business Administration University of Virginia METHODS OF VALUATION FOR MERGERS AND ACQUISITIONS This note addresses the methods used to value companies in a merger and acquisitions

Graduate School of Business Administration University of Virginia METHODS OF VALUATION FOR MERGERS AND ACQUISITIONS This note addresses the methods used to value companies in a merger and acquisitions

DCF and WACC calculation: Theory meets practice

www.pwc.com DCF and WACC calculation: Theory meets practice Table of contents Section 1. Fair value and company valuation page 3 Section 2. The DCF model: Basic assumptions and the expected cash flows

www.pwc.com DCF and WACC calculation: Theory meets practice Table of contents Section 1. Fair value and company valuation page 3 Section 2. The DCF model: Basic assumptions and the expected cash flows

9 Questions Every ETF Investor Should Ask Before Investing

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment products like mutual funds, closed-end funds,

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? 2. What kinds of ETFs are available? 3. How do ETFs differ from other investment products like mutual funds, closed-end funds,

The right bond at the right price: Understanding bond pricing. Smart bond buying could save you thousands.

The right bond at the right price: Understanding bond pricing. Smart bond buying could save you thousands. Executive summary Compared with stock market investing, it s not always easy to know what is

The right bond at the right price: Understanding bond pricing. Smart bond buying could save you thousands. Executive summary Compared with stock market investing, it s not always easy to know what is

California State University, Fresno Foundation INVESTMENT POLICY STATEMENT

INVESTMENT POLICY STATEMENT 1. Purposes of the Investment Policy Statement The purposes of this Investment Policy Statement for the management of the Foundation funds under management authority of the

INVESTMENT POLICY STATEMENT 1. Purposes of the Investment Policy Statement The purposes of this Investment Policy Statement for the management of the Foundation funds under management authority of the

Class / Ticker Symbol Fund Name Class A Class C Class C1 Class I

Mutual Funds Prospectus August 31, 2011 Nuveen Municipal Bond Funds Dependable, tax-free income because it s not what you earn, it s what you keep. Class / Ticker Symbol Fund Name Class A Class C Class

Mutual Funds Prospectus August 31, 2011 Nuveen Municipal Bond Funds Dependable, tax-free income because it s not what you earn, it s what you keep. Class / Ticker Symbol Fund Name Class A Class C Class

Allianz Malaysia Berhad (12428-W) Financial Results 4Q 2015. Analyst Briefing 29 February 2016

Financial Results 4Q 2015. Analyst Briefing 29 February 2016") Allianz Malaysia Berhad (12428-W) Financial Results 4Q 2015 Analyst Briefing 29 February 2016 1 AMB Group Results Allianz Malaysia Berhad (12428-W) Resilient Growth Operating revenue Group operating revenue

Allianz Malaysia Berhad (12428-W) Financial Results 4Q 2015 Analyst Briefing 29 February 2016 1 AMB Group Results Allianz Malaysia Berhad (12428-W) Resilient Growth Operating revenue Group operating revenue

About Our Private Investment Benchmarks

1. What is a benchmark? FREQUENTLY ASKED QUESTIONS A benchmark is a standard of measurement for investment performance. One of the more common types of benchmarks is an index which, in this case, measures

1. What is a benchmark? FREQUENTLY ASKED QUESTIONS A benchmark is a standard of measurement for investment performance. One of the more common types of benchmarks is an index which, in this case, measures

Publicly traded private equity vehicles: A different kind of model By Adam Goldman, Red Rocks Capital LLC. Accessing private equity: an overview

Publicly traded private equity vehicles: A different kind of model By Adam Goldman, Red Rocks Capital LLC Accessing private equity: an overview Over the past several decades, investors in private equity

Publicly traded private equity vehicles: A different kind of model By Adam Goldman, Red Rocks Capital LLC Accessing private equity: an overview Over the past several decades, investors in private equity

Seix Total Return Bond Fund

Summary Prospectus Seix Total Return Bond Fund AUGUST 1, 2015 (AS REVISED FEBRUARY 1, 2016) Class / Ticker Symbol A / CBPSX R / SCBLX I / SAMFX IS / SAMZX Before you invest, you may want to review the

Summary Prospectus Seix Total Return Bond Fund AUGUST 1, 2015 (AS REVISED FEBRUARY 1, 2016) Class / Ticker Symbol A / CBPSX R / SCBLX I / SAMFX IS / SAMZX Before you invest, you may want to review the

Investing in Bond Funds:

: What s in YOUR bond fund? By: Bruce A. Hyde and Steven Saunders Summary Investors who rely primarily on duration in choosing a bond fund may inadvertently introduce extension risk to their bond portfolio.

: What s in YOUR bond fund? By: Bruce A. Hyde and Steven Saunders Summary Investors who rely primarily on duration in choosing a bond fund may inadvertently introduce extension risk to their bond portfolio.

Chapter 4: Liquor Store Business Valuation

Chapter 4: Liquor Store Business Valuation In this section, we will utilize three approaches to valuing a liquor store. These approaches are the: (1) cost (asset based), (2) market, and (3) income approach.

Chapter 4: Liquor Store Business Valuation In this section, we will utilize three approaches to valuing a liquor store. These approaches are the: (1) cost (asset based), (2) market, and (3) income approach.

How to Evaluate An Investment Advisor

Key Questions to Ask an Investment Advisor Specially Prepared for Continental Airlines Pilots Nearing Retirement You have built a substantial retirement nest egg over the years. Soon, you can relax and

Key Questions to Ask an Investment Advisor Specially Prepared for Continental Airlines Pilots Nearing Retirement You have built a substantial retirement nest egg over the years. Soon, you can relax and

Impact of rising interest rates on preferred securities

Impact of rising interest rates on preferred securities This report looks at the risks preferred investors may face in a rising-interest-rate environment. We are currently in a period of historically low

Impact of rising interest rates on preferred securities This report looks at the risks preferred investors may face in a rising-interest-rate environment. We are currently in a period of historically low

PowerShares Smart Beta Income Portfolio 2016-1 PowerShares Smart Beta Growth & Income Portfolio 2016-1 PowerShares Smart Beta Growth Portfolio 2016-1

PowerShares Smart Beta Income Portfolio 2016-1 PowerShares Smart Beta Growth & Income Portfolio 2016-1 PowerShares Smart Beta Growth Portfolio 2016-1 The unit investment trusts named above (the Portfolios

PowerShares Smart Beta Income Portfolio 2016-1 PowerShares Smart Beta Growth & Income Portfolio 2016-1 PowerShares Smart Beta Growth Portfolio 2016-1 The unit investment trusts named above (the Portfolios

Projecting the 3 Statements & 3-Statement Modeling Quiz Questions

Projecting the 3 Statements & 3-Statement Modeling Quiz Questions 1. Let s say that we re creating 3-statement projections for a company, and in its historical filings Depreciation & Amortization and Stock-Based

Projecting the 3 Statements & 3-Statement Modeling Quiz Questions 1. Let s say that we re creating 3-statement projections for a company, and in its historical filings Depreciation & Amortization and Stock-Based