Measuring the Actuarial and Financial Effects on Life Settlements

|

|

|

- Terence Reed

- 8 years ago

- Views:

Transcription

1 Measuring the Actuarial and Financial Effects on Life Settlements David R. Lange, Auburn University Montgomery Joseph A. Newman, Auburn University Montgomery Introduction Life Settlements are the product of the life insurance secondary market, in which policies are sold to investors for insured s whose life expectancy has generally been reduced from 3 to 12 years (Ingraham & Salani, 2004). The investors become the new owners and beneficiaries and pay premiums until the death of the insured. The typical sale price is higher than the cash surrender value of the policy, but below the face value to account for the additional premiums until death of the insured, the time value of money, and the fact that policy proceeds paid to the investor after death are subject to income taxes to the extent of any profit made on the policy (Connolly, 2005; Cook, 2006; Deloitte Consulting, 2005; Katt, 2002). A traditional cash value life insurance policy contractually offer several options - surrender the policy for the cash value, convert the policy to paid-up insurance or extended term insurance, or continue making premium payments to keep the policy in-force (Black & Skipper, 2000). The four options above essentially represent two choices, take the cash or continue the policy in-force for the death benefits, until the death of the insured (Cook, 2006). Development of a secondary market for life insurance, Life Settlements, in which the policyholder may sell the life insurance policy to a third party investor for more than the cash surrender value has created an additional financial planning option (DeFrancesco & Salani, 2005). The policyholder s financial planning decision given the secondary market for life insurance is to evaluate the life settlement offer, assuming it is greater than the policy cash surrender value, versus continue making policy premium payments to receive the death benefits. Effectively, the latter option requires the policyholder to calculate the present value of the expected death benefits against the possibility of having to pay additional premium payments. This paper utilizes the Life Settlement Number Cruncher, a commercial program offered by Leimburg & LeClair, Inc., to illustrate the actuarial and financial effects on Life Settlements. The Life Settlement Number Cruncher provides valuations to counter the life settlement firm s life insurance pricing expertise, an advantage that civilians and their non-insurance pricing expert advisors can t match, Katt (2002). Policyholders benefit by estimating their expected 1

2 present value of the death benefits against the possibility of having to pay additional premium payments in evaluating the sale of their life insurance policy in the life settlement market. John Skar, MassMutual senior vice president and chief actuary, noted Policyholders are being convinced to sell their policies because they are being shown a comparison of cash surrender values and life settlement values and not being told about the greater values possible by holding a contract until death (Connolly, 2005). This paper is developed in four sections. The first section provides a background on the life settlement market, including a brief history, recent growth and development, and a brief review of life settlement controversial issues. The second section describes several actuarial and financial effects on life settlements. A third section includes several examples of life settlements and offers seven observations that may be made from the examples. The fourth section presents the Life Settlement Number Cruncher software estimated information for the policyholder and their financial planner in evaluating the life settlements. A final section offers conclusions. Life Settlements Development of the life settlement, secondary market for life insurance, during the late 1990 s stemmed from the 1980 s viatical settlement market in which investors purchased the life insurance polices of terminally ill policyholders (Bestwire, 2005). The life settlements market has been growing at approximately 20% per year since 1998 according to Conning Research and Consulting (DeFrancesco & Salani, 2005) In 2003 the life settlement market was approximately $2 billion and according to the Census Bureau, 35.9 million individuals aged 65 and over owned a life insurance policy (DeFrancesco & Salani, 2005). Coventry First purchased $1.9 billion of life insurance face value in 2004, in an estimated [no regulatory reported statistics] 2004 total life settlement market face value of life insurance of $6 billion (Bestwire, 2005). The estimated 2005 life settlement market face value of life insurance was between $10 and $15 billion, though still less than 0.2% of the in-force individual life insurance face amount of approximately $9 trillion (Cook, 2006). In 2005, life insurance auctions were available on the Web (Bell, 2005). The institutional interest in Life Settlements as an investment is clear as a block of polices has a relatively predictable life expectancy and can be quite profitable (Brecka & Virkler, 2004). 2

3 Overall, the life settlement is not a new concept as the sale of life insurance contracts has a long history of court litigation involving the issue of gambling versus legitimate investment (Kreitner, 2000). At first, life insurance itself was questioned as being an immoral gamble on death. After life insurance became more accepted, the gambling issue was addressed with the doctrine of "insurable interest" where it was found that legitimate insurance existed only when there was a significant relationship between the insured and the beneficiary. The purpose of this doctrine was both to limit gambling, and to limit the moral hazard that tempts the beneficiary to murder the insured. Complications resulted when insurance policies were assigned to others and the new owners, often unrelated to the insured, became the new beneficiaries. Before 1880, the only way policyholders could recoup premiums while still living was to assign their policies. This resulted in regulators putting pressure on insurance companies to buy back their policies, but early surrender values were low, and policyholders still sold policies to obtain a better price. The practice of assigning policies generated litigation, but the transactions, as long as not clearly found to be gambling on lives, were upheld. Assigning policies was upheld to protect the insured by viewing the policies as investments, and the assignments upheld to maintain their liquidity. Overall Kreitner (2000) shows that life insurance contracts have been assigned (sold) for value since the nineteenth century, have been controversial, but where the parties have acted in good faith the sales have been upheld, and even considered beneficial, by the courts. The predictable controversy arises from possible conflicting financial interests or impacts of life settlements on policyholders, investors, and insurance companies. The Life Insurance Settlement Association provides the following list of reasons to consider a life settlement (LISA, 2006), The policy is no longer needed or wanted. Opportunities to obtain a superior insurance policy. Premium payments have become unaffordable. Changes in estate planning needs. Rising healthcare costs or mounting financial concerns. Doherty and Singer (2003, pg. 453) offer a similar, but more specific listing. Essentially, the argument is selling a life insurance policy under the right circumstances could help your (financial planning) clients as much as purchasing one when they need the protection (DeFrancesco & Salani, 2005). Policyholders get a double benefit - they receive a lump sum 3

4 greater than the cash surrender value of the policy and do not have to continue making premium payments (DeFrancesco & Salani, 2005). In short, prior to the recent development of the secondary market for life insurance policies, life insurance companies were normally in a monopsony position, offering only the cash surrender value to the policyholders (Doherty and Singer, 2003). Overall, the life settlement market has increased policyholder welfare and made the life insurance market more efficient (Doherty and Singer, 2003). A study by Deloitte Consulting (2005, pg 13) however, finds that a policyholder with an impaired policy could maximize her estate value if other assets are liquidated and the life insurance policy is maintained until death. An analysis of life settlements from 2000 through 2003 showed life settlement payments averaging 20 cents per dollar of face amount of insurance (Deloitte, 2005). The primary point is, given the decline in health, the life insurance policy has become more valuable, which explains why investors are willing to purchase the policy in anticipation of higher after-tax returns even after relatively large transaction costs (Skar, 2004; Connolly, 2005). In sum, a life insurance policyholder may be better off keeping a policy than selling or surrendering it (Silverman, 2005, May 31). Another issue is the impact on the insurance company since life settlements assure the payment of death benefits on life insurance policies that may have otherwise been surrendered. Skar (2004) suggests this issue is small as anti-selection is already included in the mortality assumptions in life insurance policies. An alternative to life settlements is the insurer offering more than the contractual cash surrender value (Cook, 2006). A related concept is when investors fund the purchase of new life insurance policies (Silverman, 2005, May 26). Actuarial and Financial Effects The actuarial effect on life settlements may be represented by converting the CSO Mortality Tables, which list the number of deaths per 1000 insured s living at a given age, into a probability of premature death. Table 1: CSO Mortality Tables (% Format) includes the 1958, 1980 and 2001 CSO Tables, as well as 300% of the 2001 CSO Table. The interpretation of Table 1 is, according to the 1980 CSO Table, a Female age 70 had a 2.21% probability of suffering premature death before age 71. The three CSO tables with the 300 % of the 2001 Table provide several life settlement actuarial effects. First, policy cash values for most cash value life insurance policies included in 4

however, finds that a policyholder with an impaired policy could maximize her estate value if other assets are liquidated and the life insurance policy is")

5 life settlements are based on the 1958 and 1980 Tables, as the 2001 Table was not required to be used until recently. Second, tracing across the tables for any given age [1958 Table had a three year offset for Females, age 68 would be age 65], demonstrates the reduced probability of premature death experienced since the 1960 s. Finally, comparing the 300% column to the respective CSO Table based life insurance policy reflects the decision described above, in which the policyholder must calculate the present value of the expected death benefits including the possibility of having to pay additional premium payments. Traditional whole life insurance policies have a policy cash surrender value, reflecting the regulatory mandated policy reserves, determined according to the Commissioners Reserve Valuation Method (CRVM) or Full Preliminary Term Method (Black & Skipper, 2000). The determination of traditional whole life policy premiums and related cash values is based on a prospective approach (Bowers, et al. 1997, Jordan 1991). The financial logic of the prospective approach is relatively straightforward. At policy issue, the present value of the expected death benefits payable equals the present value of the expected premiums to be received, or Net Single Premium (Black & Skipper, 2000). As the policy matures the present value of the expected death benefits increases and the present value of the expected premium payments declines, since some premiums have already been paid. The increasing expected death benefit and decreasing number of expected premiums is funded by the policy cash value reserves (Black and Skipper, 2000). In a strictly financial context, the funding of life insurance could be thought of as a capital budgeting project in which the death benefits and premium payments both represent cash flows, the respective direction depending on the perspective of the insured or insurer (Jones and Lange, 2004). A complication in the net present value calculation arises when considering that both the death benefit and premium payments are a function of a mortality probability varying by age. Though once mortality probabilities are provided, the prospective approach may easily be demonstrated with a spreadsheet application, and the question of the life insurance premium and cash surrender value determination is simply a financial problem of converting two unequal series of cash flows into respective present values and an associated annuity premium (Jones and Lange, 2004). This mortality rate, essentially reflects a prior sample period mortality experience by age, and is used, as noted above, as a basis for determining life insurance premiums and cash values 5

6 for the standard average-health policyholder, or regulated base guaranteed policy values 1. However, were the policyholder to become ill, or otherwise experience a decline in health, the death benefits become more likely and the continued premiums payments equally less so. Given a health adjusted rated mortality probability, the expected cash value of the policy would increase. The expected cash value may be estimated, as done below, with the prospective spreadsheet provided by Jones & Lange (2004) by changing the mortality assumptions. Expected cash value also reflects the pricing advantage identified by Katt (2002) and the greater values possible by holding a contract until death, Connolly (2005). Using the simplified formula provided by Cook (2006) but substituting the present terminology, the life insurance policyholder evaluation becomes, Policy Surrender Value < Life Settlement Value < Expected Cash Value < Death Benefit Intrinsic Economic Value Economic Value of Impaired Policies Extra-Contractual Cash Value The estimate of the expected present value of the death benefit minus the expected present value of premium payments is referred to by Deloitte Consulting (2005) as the Intrinsic Economic Value (IEV), Economic Value of Impaired Policies by Doherty and Singer (2003), and Extra-Contractual Cash Value suggested by Cook (2006). The use of expected cash value is suggested as a less confusing term for policyholders than intrinsic, impaired or extra. Description of the value in a life insurance policy in financial, versus actuarial or economic terms follows the prior applied methods of Jones & Lange (2004) and Katt (2002). Additional financial spreadsheet applications of life insurance valuations are provided by Lange & Simkins (2001, 2003), and an example of the financial planning benefits in Himes, Jones & Lange (2004). Traditional Whole Life Assume at age 67, the policyholder, after a very wonderful life of food and fun, is in less than average health, obese, and has diabetes and heart problems. The less than average health status may indicate a 300% multiple of the standard CSO rates, a substandard rating according to 1 A complete description of the Prospective Approach to premium and cash surrender value determination is beyond the scope of this paper. Readers are may refer to Bowers et al (1997), Jordan (1991), or numerous insurance textbooks. 6

by changing the mortality assumptions.")

7 Table 1: CSO Mortality Tables (% Format). That is, if the policyholder had to apply for additional or replacement life insurance coverage, the policy would be issued on a Rated or substandard risk basis, requiring a higher premium to reflect the higher mortality probability. The premium on the existing policy was based on standard probabilities and associated rates at issue and is therefore locked in. Thus Rated refers to an increase in the individual policyholders mortality probability, not the concept of a Rated, higher premium policy. The policyholder has a choice of continuing the life insurance policy with the stated death benefit or surrendering the policy for the policy cash value. In a strictly objective financial context, the policyholder would consider the increased probability of receiving the death benefit, noted above, versus the decreased possibility of paying additional premium payments, or Expected = Present Value of _ Present Value of Cash Value Expected Death Benefits Expected Premium Payments The increase in the present value of the expected death benefit and reduction in likely additional premium payments with the rating of less than standard health status creates an additional financial value for the whole life policy over the mandated standard risk policy reserve formulas. It is this increased expected cash value 2 which supports the development of the secondary market in life insurance. That is, an investor may offer the policyholder more than the policy cash value to continue the policy in expectation of receiving the death benefit $500,000. Tax implications are presently excluded to simplify the discussion and show that the secondary market, while providing a new special option to the policyholder, provides a special incentive to sell the policy to an investor, which increases the likelihood that the insurance company will eventually pay out the death benefit. Another example may have the policyholder suffering a heart attack, diagnosis of cancer, or some other specific illness. The mortality probabilities for a specific disease may be significantly different than a simple multiple of the standard CSO rates. 2 Identified by Doherty and Singer 2003 as the Economic Value of Impaired Policies. The use of Expected Cash Value applies to all polices, not just impaired, permitting a broader discussion of policyholder decision making. 7

8 Convertible Term Convertible term insurance allows for the conversion of the policy into a cash value product, generally for a traditional whole life policy with a premium appropriate for the attained age of the insured (Black & Skipper, 2000). If the policyholder did not have the term conversion option, the term policy could be continued at increasing annual standard term premiums, or the policyholder could apply for an alternate level premium product. If a new policy were issued, it would be on a rated or substandard risk basis, requiring a higher premium to reflect the higher than normal mortality probability. The premium on the converted term policy though is based on standard rates for the attained age. Thus once again, rated refers to an increase in the individual policyholders mortality probability, not the concept of a rated, higher premium policy. Universal Life Universal Life provides a third and significantly different life settlement valuation. The policy cash value may range from more than the traditional whole life policy cash value for fully funded policies to almost zero policy cash values for underfunded or thinly funded policies, depending on prior premium payments and credited interest rates. For funded polices, no premium is required if the policy cash value is greater than current policy costs expenses, fees and cost of insurance (Black & Skipper, 2000). The current Universal Life policy cash value could be used to pay the policy costs first, thus the present value of expected premium Payments is reduced by the current cash value, increasing the expected cash value. If the policy cash value is close to zero, the minimum premium due is that amount that will cover the next periods current policy costs - expenses, fees and cost of insurance. In this case, the Universal Life policy is effectively a renewable term policy to maturity. Life Settlement Examples Table 2: Estimated Traditional Cash Values and Premiums presents advertised life settlement examples from CIGI Direct Insurance, Insurance Appraisal, US Life Settlements and AIM Life Settlements. Table 2 includes the policy holder gender and age, financial reasoning for the life settlement or health of the policyholder, life insurance policy type, policy face amount - death benefit, policy cash value, life settlement amount paid; and two calculated values, traditional cash value and premium. 8

9 Referring to Table 2, the first policyholder was a Female in very good health who sold a $750,000 Universal Life Insurance policy with a Policy Cash Value of $102,287 for $137,000. The second example is a Male age 68 with Bi-Pass History who sold a $200,000 convertible term policy for $40,500. The examples in Table 2 offer several general observations. 1) Policyholders tend to be 65 and older unless there is significant health impairment as with #8, Female age 44 with breast cancer. 2) The financial reasoning varies from the purchase of a new lower premium policy, obsolete key man policy, outlived beneficiary, to paying for long term care insurance or current medical bills. Health ranges from very good health, overweight, smoker, to heart attack. 3) The life insurance policy type tends to be Universal Life, Convertible Term or straight Term policies. 4) Face amounts are often large, $1,000,000 or more. 5) Life Settlement amount is larger than Policy Cash Value. Two additional observations may be made based on the calculated Traditional Cash Value and Premium columns. The Traditional Cash Value is the surrender cash value that would be available in a standard whole life insurance policy based on the Commissioners Reserve Valuation Method (CRVM) (Black & Skipper, 2000), calculated using the financial spreadsheet application shown in Lange & Simkins (2003) and Jones & Lange (2004). The Traditional Cash Value represents the cash value needed to fully fund the policy to maturity. Comparison of the policy cash value with the Traditional Cash Value shows the degree to which the Universal Life Insurance policies were underfunded. Example #22 Male age 73 Universal policy had a Policy Cash Value of $1,507 and a Traditional Cash Value under actuarial assumptions of $60,000. As such, this Universal policy was about to lapse unless a premium sufficient to pay the cost of insurance and policy expenses was paid essentially a term policy. Premium is the premium required to maintain the life insurance policy in-force as calculated by the financial spreadsheet application in Lange & Simkins (2001). The Premium calculation is necessary as the policyholder determines the cost of maintaining the policy and receiving the death benefit versus accepting the life settlement offer 3. 3 Accumulated premiums were set equal to the Life Settlement Value to avoid tax consequences. 9

The financial reasoning varies from the purchase of a new lower premium policy, obsolete key man policy, outlived beneficiary, to paying for long term care insurance or current medical bills.")

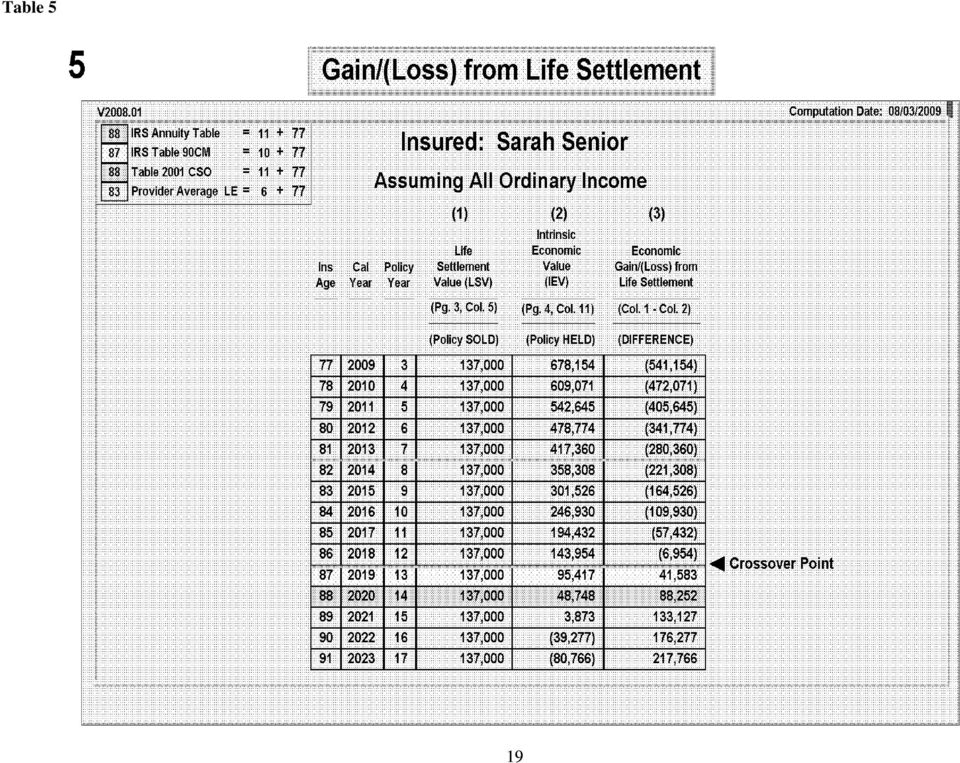

10 The two additions observations based on the above are, 6) Policy Cash Values on the Universal policies are generally much lower than that required to maintain the policy in-force as represented by the Traditional Cash Value. And, 7) the Premium required to maintain the underfunded Universal life, Convertible Term and straight Term polices given the larger face value death benefit and cost of insurance at an advanced age are in many cases quite substantial. Life Settlement Number Cruncher The Life Settlement Number Cruncher (Leimburg & LeClair, 2008) is a commercial software program designed to assist the financial planner in evaluating life settlement offers 4. The primary function of the Life Settlement Number Cruncher is to estimate the financial (economic) gain or loss of the life settlement offer, where; Financial Gain/Loss = Life Settlement Offer Expected Cash Value (Intrinsic Economic Value) And, Expected Cash Value = Present Value of - Present Value of (Intrinsic Economic Value) Expected Death Benefits Expected Premium Payments The Financial Gain or Loss supports the policyholder s decision of continuing the life insurance policy with the stated death benefit and paying premiums or selling the policy for the life settlement offer. Table 3: Estimated Intrinsic Economic Values includes the insured, policy information and calculated Traditional Cash Value and Premium columns from Table 2, and adds Intrinsic Economic Value and Financial Gain/Loss at the time of the Life Settlement (LS) and at Life Expectancy (LE). For example #1, the Female age 77, the Intrinsic Economic Value at the time of the Life Settlement equals the present value of the $750,000 death benefit discounted at 4% minus the premium payment of $43,000, or $678,154. Had death occurred in the first year and the policy been sold for the Life Settlement amount of $137,000, the Financial Loss would be $541,154 [$137,000 - $678,154]. Assuming death occurs at Life Expectancy, 11 years, subtracting the Intrinsic Economic Value of $48,748 from the Life Settlement of $137,000 results in a Financial Gain of $88, The Life Settlement Number Cruncher was removed from sale in 2009 given insufficient sales volume. 10

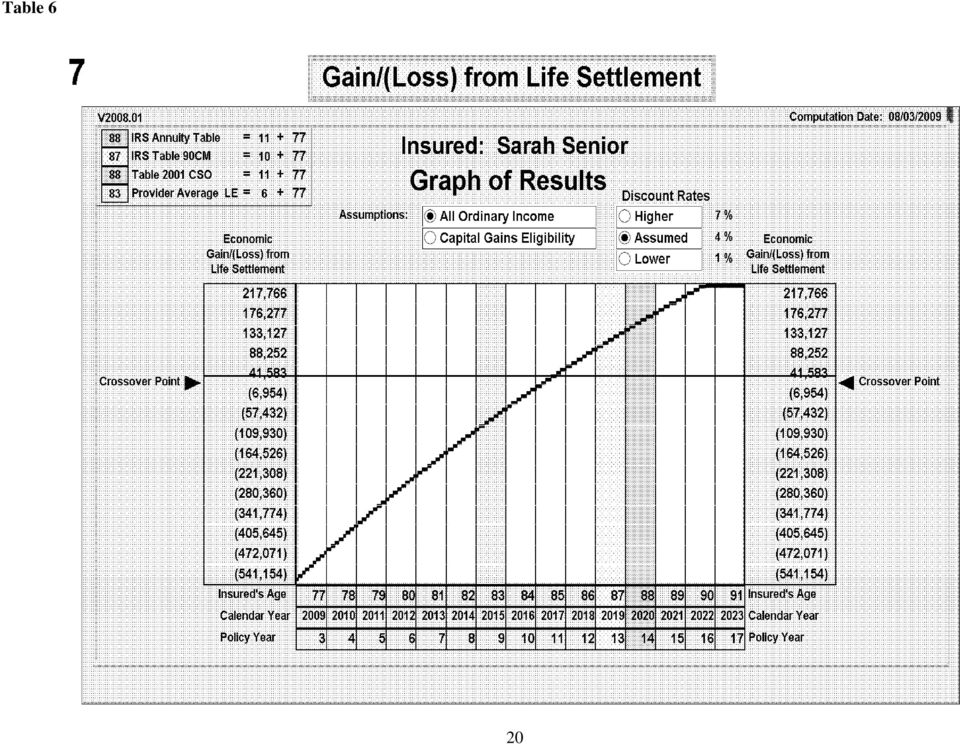

11 There two very important points with this analysis. First, all values are in terms of Present Values. The $88,252 Financial Gain is in today s dollars, as is traditionally done in capital budgeting applications. It may be necessary to explain to insured that $750,000 would be received as death benefits after 11 years, but they would have had to pay $473,000 (11 years * $43,000/year) in premiums. Second, the Life Expectancy of 11 years is based on a standard risk and the 2001 CSO Table. Generally speaking, life settlements are tailored to those with a reduced life expectancy, and even if standard, are more likely to reflect the 1980 CSO mortality probabilities at the advanced ages. Referring to Table 3, Life Settlements will always involve a Financial Loss in the year of the policy sale, and likely several years there-after, as the present value of the Death Benefits will exceed the Life Settlement cash value. However, as required premiums must be paid, it is possible for the Life Settlement to provide a Financial Gain as noted in the last column of Table 3, Financial However, recall form above, the Life Expectancy may be overstated. Perhaps the primary benefit of the Life Settlement Number Cruncher is annual values are provided for a range of up to 15 years. As shown in Table 4: Intrinsic Economic Value, the last column provides the IEV out to age 91 for the example #1 Female age 77. There is even a point at which present value of the premiums will exceed the present value of the death benefit, age 90 in Table 4. This occurs because insurance policy premiums are an annuity due and the death benefit is a single sum future value. An additional contributing factor is the advanced age of the policyholder which requires higher premiums based on greater mortality probabilities, especially for underfunded universal life, convertible term and straight term policies [see Table 1]. Table 5: Gain (Loss) from Life Settlement includes the Life Settlement Value, and annual Intrinsic Economic Value and Economic (Financial) Gain (Loss) from Life Settlement. The same information is graphically depicted in Table 6: Gain (Loss) from Life Settlement. The benefit of Table 5 and Table 6, is the policyholder can see the annual present value of the life settlement decision and associate an adjusted life expectancy to assist in making a more informed decision. Table 7: Intrinsic Economic Value and Table 8: Gain / (Loss) form Life Settlement provides similar information for example #22, Male age 73. Tables 9 and 10: Gain (Loss) from 11

12 Life Settlement offers the graphical demonstration of the final financial effect, changing the discount rate from 4% to 7%. Comparing Tables 9 & 10, the net effect is a reduction in the Economic Loss and an increase in the Economic Gain. The explanation is the same as above, the higher interest rate impacts the present value of the death benefit more since insurance policy premiums are an annuity due and the death benefit is a single sum future value. Conclusion Development of a secondary market for life insurance - a life settlement, in which the policyholder sells their life insurance policy to a third party investor for more than the cash surrender value has created an additional financial planning option. The financial planning decision for the policyholder in a secondary market for life insurance is to evaluate the life settlement offer which is greater than the policy cash surrender value versus continue making policy premium payments to receive the death benefits. The latter option requires the policyholder to further evaluate the present value of the expected death benefits against the possibility of having to pay additional premium payments. The Life Settlement Number Cruncher (Leimburg & LeClair, 2008) estimate the financial (economic) gain or loss of the life settlement offer, where; Financial Gain/Loss = Life Settlement Offer Expected Cash Value (Intrinsic Economic Value) And, Expected Cash Value = Present Value of - Present Value of (Intrinsic Economic Value) Expected Death Benefits Expected Premium Payments The Financial Gain or Loss supports the policyholder s decision of continuing the life insurance policy with the stated death benefit and paying premiums or selling the policy for the life settlement offer. This is important information for the policyholder or their financial planner in evaluating the life settlement question, leading to a better, more informed decision. 12

13 References Bell, Allison, Life Settlements Hit The Web; A new development in what is becoming a major market, National Underwriter - Life & Health/Financial Services Edition, September 19, pg. 12 BestWire, Growth in Life Settlements has Life Insurers Concerned, Say Industry Experts, - A.M. Best Company, Inc, February 22, 2005 Best s Policy Reports, Term Insurance, AM Best, June, 2000 Black, Kenneth and Harold D. Skipper, Life & Health Insurance, Prentice Hall, 2000 Bowers, Newton L., Hans U. Gerber, James C. Hickman, Donald A. Jones and Cecil J. Nesbitt. Actuarial Mathematics (Schaumburg, 1997), Society of Actuaries. Brecka, Gary and Tom Virkler, Life Settlements: A Second Look at a Secondary Market, Journal of Financial Service Professionals, March 2004, 58 (2), pp Connolly, Jim, Study Spurs Clash On Settlements, National Underwriter - Life & Health/Financial Services Edition, May 30, 2005, pg. 10 Cook, David, How Insurers Might Compete With The Secondary Market, National Underwriter -Life & Health/Financial Services Edition, September 18, 2006, pg. 14 DeFrancesco, Roccy and Sergio Salani, A Hidden Asset: How clients can turn life insurance into cold, hard cash while they're still alive, Financial Planning, June 1, 2005 Deloitte Consulting LLP and the University of Connecticut, The Life Settlements Market: An Actuarial Perspective on Consumer Economic Value, 2005 Doherty, Neil A. and Hal J. Singer, The Benefits of a Secondary Market for Life Insurance Policies, Real Property, Probate and Trust Journal, Fall 2003, pp Gutner, Toddi, Wanted: Your Life Insurance: Investors are Keen to Offer life settlements. Seller Beware, Business Week online, October 31, Hamwi, Iskandar S. and Durwood Ruegger, Past and Present Changes in Living Policy Values, Journal of the American Society of CLU & ChFC, November 1994, 48 (6) pp Himes, Ken G., Steven T. Jones and David R. Lange, In-Force Policy Illustrations A Financial Planning Tool, Journal of Financial Planning, July 2003, pp Ingraham, Harold G. and Sergio S. Salani, Life Settlements as a Viable Option, Journal of Financial Service Professionals, September 2004, 58 (5), pp

, Society of Actuaries.")

14 Jones, Steven T. and David R. Lange Incorporating Life Insurance into the Finance Curriculum: A Prospective Spreadsheet Approach, Journal of the Academy of Business Education, Volume 5, pp , Fall 2004 Jordan, Chester Wallace Jr. Society of Actuaries Textbook on Life Contingencies The Society of Actuaries. Schaumburg, 1991 Katt, Peter C., Assessing Clients Life Settlement Offers, Journal of Financial Planning, July 2002 Kreitner, Roy. "Speculations of Contract, or How Contract Law Stopped Worrying and Learned to Love Risk," Columbia Law Review, Vol. 100, No. 4, May, 2000, pp Lange, David R, and Joseph A. Newman, The Secondary Market for Life Insurance: An Evaluation of Life Settlements, Academy of Financial Services Proceedings CD Session E2, October 2006 Lange, David R. and Betty J. Simkins, The Retrospective Life Insurance Method: A Pedagogic Spreadsheet Application Advances in Financial Education, Volume.1, Fall 2003, pp Lange, David R. and Betty J. Simkins, Calculating Funding Premiums for Universal Life Insurance, Calvin Cherry, April 2000, North American Actuarial Journal, Volume 5, # 3, July 2001, pp Learn Life Settlements, CIGI Direct Insurance Services, Inc., (learnlifesettlements.com). Life Settlement Number Cruncher, Leimburg & LeClair, Inc., Havertown, PA, 2008 LISA, Cashing in on Unneeded Life Insurance Policies: How Seniors are Benefiting from Life Settlements, Life Insurance Settlement Association - White Paper, August 22, 2006 (lisassociation.org) Office of Cancer Survivorship Fact Sheet, May 2006, (survivorship.cancer.gov). Silverman, Rachel Emma, Recognizing Life Insurance s Value: Study Says Keeping a Policy May Mean a Bigger Payoff than Selling to an Investor, The Wall Street Journal, May 31, pg. D.2 Silverman, Rachel Emma, Letting an Investor Bet on When You ll Die; New Insurance Deals Aimed at Wealthy Raise Concerns; Surviving the Two-Year Window, The Wall Street Journal, May 26, 2005, pg. D.1. Skar, John, A Question of Life Settlements, Contingencies, March/April 2004, pp The Economist, New Lease on Life: The Secondary Market in Life-Insurance Policies is Good for Consumers, May 17,

15 Table 1: CSO Mortality Tables (% Format) 300% 300% 1958 CSO 1980 CSO 1980 CSO 2001 CSO 2001 CSO 1980 CSO 1980 CSO Male Male Female Male Female Male Female Age Female % 2.54% 1.46% 1.77% 1.23% 7.63% 4.38% % 2.79% 1.60% 1.93% 1.34% 8.36% 4.80% % 3.04% 1.74% 2.10% 1.45% 9.13% 5.23% % 3.32% 1.88% 2.27% 1.57% 9.96% 5.65% % 3.62% 2.04% 2.47% 1.71% 10.85% 6.11% % 3.95% 2.21% 2.69% 1.86% 11.85% 6.63% % 4.33% 2.42% 2.97% 2.04% 12.99% 7.27% % 4.77% 2.69% 3.29% 2.23% 14.30% 8.06% % 5.26% 3.01% 3.63% 2.44% 15.79% 9.03% % 5.82% 3.39% 4.00% 2.67% 17.46% 10.18% % 6.42% 3.82% 4.40% 2.92% 19.26% 11.47% % 7.06% 4.30% 4.84% 3.20% 21.19% 12.89% % 7.71% 4.80% 5.37% 3.50% 23.14% 14.41% % 8.39% 5.35% 5.97% 3.83% 25.17% 16.04% % 9.11% 5.94% 6.65% 4.19% 27.32% 17.81% % 9.88% 6.60% 7.40% 4.64% 29.65% 19.80% % 10.75% 7.36% 8.22% 5.20% 32.24% 22.08% % 11.73% 8.24% 9.08% 5.78% 35.18% 24.72% % 12.83% 9.25% 10.02% 6.39% 38.48% 27.76% % 14.03% 10.38% 11.07% 7.07% 42.08% 31.14% % 15.30% 11.61% 12.24% 7.76% 45.89% 34.83% % 16.61% 12.93% 13.52% 8.57% 49.83% 38.79% % 17.96% 14.33% 14.90% 9.57% 53.87% 43.00% % 19.33% 15.82% 16.37% 10.63% 57.98% 47.45% % 20.73% 17.39% 17.90% 11.67% 62.19% 52.18% % 22.18% 19.08% 19.43% 12.42% 66.53% 57.23% % 23.70% 20.89% 20.93% 13.15% 71.09% 62.66% % 25.35% 22.88% 22.49% 14.37% 76.04% 68.64% % 27.21% 25.15% 24.15% 16.02% 81.63% 75.45% % 29.59% 27.93% 25.89% 18.09% 88.77% 83.79% % 33.00% 31.73% 27.61% 20.35% 98.99% 95.20% % 38.46% 37.57% 29.30% 22.57% % 48.02% 47.50% 31.09% 24.01% % 65.80% 65.59% 33.00% 24.78% % % % 35.03% 26.40% 15

16 Table 2: Estimated Traditional Cash Values and Premiums # Gender Age Financial Reasoning / Health Life Policy Type Policy Face Amount Policy Cash Value Life Settlement Traditional Cash Value Premium Learn Life Settlements, CIGI Direct Insurance Services, Inc. (learnlifesettlements.com) 1 Female 77 Very Good Health Universal $750,000 $102,287 $137,000 $321,568 $43,000 2 Male 68 Bi-Pass History Convertible Term $200,000 $0 $40,500 $0 $15,000 3 Male 56 Prostate Cancer History Convertible Term $1,500,000 $0 $360,000 $0 $55,000 4 Male 66 Very Good Health Convertible Term $1,000,000 $0 $24,650 $0 $66,000 5 Male 66 Smoker. Fair Health Universal $1,500,000 $76,537 $265,000 $480,000 $63,000 6 Male 86 Fair Health Universal $1,000,000 $150,565 $570,000 $590,000 $120,000 7 Male 65 Overweight Convertible Term $150,000 $0 $5,000 $0 $9,300 8 Female 44 Breast Cancer Term $300,000 $0 $225,000 $0 $400 Insurance Appraisal.com, consumer advocate Website ( 9 Male 73 NA Variable Universal $1,500,000 $2,631 $348,000 $ $97, Male 86 Purchase lower premium policy. Universal $500,000 $62,317 $255,000 $300,000 $60, Female 83 Purchase lower premium policy. Universal $5,500,000 $481,321 $2,350,000 $3,230,000 $600,000 US Life Settlements ( 12 Male 86 Obsolete estate plan. Term $3,000,000 $0 $1,175,000 $0 $405, Female 85 Policy performance with drop in Universal $600,000 $160,000 $245,000 $350,000 $45,000 interest rates. Purchased annuity. 14 Female 75 Purchase less expensive, more Universal $7,000,000 $1,250,000 $2,900,000 $3,250,000 $375,000 suitable survivorship policy. 15 Female 69 Purchase Long Term Care Term $600,000 $0 $94,280 $0 $6, Male 75 Pay for Guaranteed Death Policy Universal $4,100,000 $280,000 $975,000 $1,900,000 $290, Male 81 Obsolete Key Man Policy Term $6,000,000 $0 $661,000 $0 $800, Male 76 Outlived Beneficiary Universal $7,000,000 $659,000 $1,900,000 $3,400,000 $450, Female 79 Premium expense vs. Cash Term $1,500,000 $0 $300,000 $0 $120, Male 76 Obsolete Estate, No Legacy Universal $10,000,000 $449,000 $2,700,000 $4,900,000 $735,000 AIM Life Settlements ( 21 Female 71 Premium Expense, Medical Bills Term $250,000 $0 $35,000 $0 $7, Male 73 Heart Attack, Long Term Care Universal $350,000 $1,507 $60,000 $150,000 $26, Male 69 Obsolete Key Man Policy Key Man $2,000,000 $271,000 $473,000 $640,000 $84,000 16

17 Table 3: Estimated Intrinsic Economic Values # Gender Age Policy Face Amount Policy Cash Value Life Settlement Traditional Cash Value Premium Intrinsic Economic Financial Gain (Loss)@LS Intrinsic Economic Financial Gain (Loss)@LE Learn Life Settlements, CIGI Direct Insurance Services, Inc. (learnlifesettlements.com) 1 Female 77 $750,000 $102,287 $137,000 $321,568 $43,000 $678,154 ($541,154) $48,748 $88,252 2 Male 68 $200,000 $0 $40,500 $0 $15,000 $177,308 ($ ) ($62,394) $102,894 3 Male 56 $1,500,000 $0 $360,000 $0 $55,000 $1,387,308 ($1,027,308) $196,925 $163,075 4 Male 66 $1,000,000 $0 $24,650 $0 $66,000 $895,538 ($870,888) ($207,901) $232,551 5 Male 66 $1,500,000 $76,537 $265,000 $480,000 $63,000 $1,379,308 ($1,114,308) $104,420 $160,580 6 Male 86 $1,000,000 $150,565 $570,000 $590,000 $120,000 $841,538 ($271,538) ($336,676) $1,013,726 7 Male 65 $150,000 $0 $5,000 $0 $9,300 $139,231 ($134,231) $25,474 ($20,474) 8 Female 44 $300,000 $0 $225,000 $0 $400 $288,062 ($63,062) $161,954 $63,046 Insurance Appraisal.com, consumer advocate Website ( 9 Male 73 $1,500,000 $2,631 $348,000 $ $97,000 $1,345,308 ($997,308) ($288,726) $636, Male 86 $500,000 $62,317 $255,000 $300,000 $60,000 $420,769 ($165,769) $5,431 $249, Female 83 $5,500,000 $481,321 $2,350,000 $3,230,000 $600,000 $4,688,462 ($2,338,462) ($182,437) $2,532, Male 86 $3,000,000 $0 $1,175,000 $0 $405,000 $2,479,615 ($1,304,615) ($248,312) $1,423,312 US Life Settlements ( 13 Female 85 $600,000 $160,000 $245,000 $350,000 $45,000 $531,923 ($286,923) $123,322 $121, Female 75 $7,000,000 $1,250,000 $2,900,000 $3,250,000 $375,000 $6,355,769 ($3, ) $309,616 $2,590, Female 69 $600,000 $0 $94,280 $0 $6,000 $570,923 ($476,643) $263,780 ($169,500) 16 Male 75 $4,100,000 $280,000 $975,000 $1,900,000 $290,000 $3,652,308 ($2,677,308) ($1,076,722) $2,051, Male 81 $6,000,000 $0 $661,000 $0 $800,000 $4,969,231 ($4,308,231) ($1,970,676) $2,631, Male 76 $7,000,000 $659,000 $1,900,000 $3,400,000 $450,000 $6,280,769 ($4,380,769) ($20,036) $1,920, Female 79 $1,500,000 $0 $300,000 $0 $120,000 $1,322,308 ($1,022,308) ($118,936) $418, Male 76 $10,000,000 $449,000 $2,700,000 $4,900,000 $735,000 $8,880,385 ($6,180,385) ($200,699) $2,900,699 AIM Life Settlements ( 21 Female 71 $250,000 $0 $35,000 $0 $7,000 $233,385 ($198,385) $57,874 ($22,874) 22 Male 73 $350,000 $1,507 $60,000 $150,000 $26,000 $310,538 ($250,538) ($83,511) $143, Male 69 $2,000,000 $271,000 $473,000 $640,000 $84,000 $1,839,077 ($1,366,077) $139,227 $333,773 17

($62,394) $102,894 3 Male 56 $1,500,000 $0 $360,000 $0 $55,000 $1,387,308 ($1,027,308) $196,925 $163,075 4 Male 66 $1,000,000 $0 $24,650 $0 $66,000 $895,538 ($870,888) ($207,901) $232,551 5 Male")

18 Table 4 18

19 Table 5 19

20 Table 6 20

21 Table 7 21

22 Table 8 22

23 Table 9 23

24 Table 10 24

The Financial Basis for No Lapse Universal Life Insurance

The Financial Basis for No Lapse Universal Life Insurance Lise Graham Professor of Finance University of Wisconsin La Crosse 406B W. Carl Wimberly Hall 1725 State St. La Crosse, WI 54601 graham.lise@uwlax.edu

The Financial Basis for No Lapse Universal Life Insurance Lise Graham Professor of Finance University of Wisconsin La Crosse 406B W. Carl Wimberly Hall 1725 State St. La Crosse, WI 54601 graham.lise@uwlax.edu

Universal Life Insurance Duration Measures

Universal Life Insurance Duration Measures Peter Alonzi Professor of Economics and Finance Brennan School of Business Dominican University 7900 W. Division Fine Arts 220-C River Forest, Illinois 60305

Universal Life Insurance Duration Measures Peter Alonzi Professor of Economics and Finance Brennan School of Business Dominican University 7900 W. Division Fine Arts 220-C River Forest, Illinois 60305

Until recent years, the disposition of life insurance

Reprinted with permission from the Society of Financial Service Professionals. Reproduction prohibited without publisher's written permission. Life Settlements by Harold G. Ingraham, Jr., FSA, MAAA, CLU

Reprinted with permission from the Society of Financial Service Professionals. Reproduction prohibited without publisher's written permission. Life Settlements by Harold G. Ingraham, Jr., FSA, MAAA, CLU

AQUARIUS LIFE Page 1 of 8 SOLUTIONS

AQUARIUS LIFE Page 1 of 8 LIFE SETTLEMENTS - UNDERSTANDING THE FACTS AND MYTHS OF THIS SECONDARY INSURANCE PRODUCT What is a life settlement? Simply put, a life settlement is the sale of an unwanted, no

AQUARIUS LIFE Page 1 of 8 LIFE SETTLEMENTS - UNDERSTANDING THE FACTS AND MYTHS OF THIS SECONDARY INSURANCE PRODUCT What is a life settlement? Simply put, a life settlement is the sale of an unwanted, no

VERMONT DEPARTMENT OF BANKING AND INSURANCE REVISED REGULATION 77-2 VERMONT LIFE INSURANCE SOLICITATION REGULATION

VERMONT DEPARTMENT OF BANKING AND INSURANCE REVISED REGULATION 77-2 VERMONT LIFE INSURANCE SOLICITATION REGULATION Section 1. AUTHORITY This rule is adopted and promulgated by the Commissioner of Banking

VERMONT DEPARTMENT OF BANKING AND INSURANCE REVISED REGULATION 77-2 VERMONT LIFE INSURANCE SOLICITATION REGULATION Section 1. AUTHORITY This rule is adopted and promulgated by the Commissioner of Banking

LIFE SETTLEMENT INFO KIT

How You Can Use A Life Insurance Policy To Fund Assisted Living And Senior Care Costs. LIFE SETTLEMENT INFO KIT Peace of Mind for You & Your Loved Ones Getting older should mean more time spent with your

How You Can Use A Life Insurance Policy To Fund Assisted Living And Senior Care Costs. LIFE SETTLEMENT INFO KIT Peace of Mind for You & Your Loved Ones Getting older should mean more time spent with your

Introduction to Life Settlements and Ethical Guidance for Advisors*

Introduction to Life Settlements and Ethical Guidance for Advisors* By Richard M. Weber and E. Randolph Whitelaw Introduction An active and rapidly growing secondary market for life insurance emerged less

Introduction to Life Settlements and Ethical Guidance for Advisors* By Richard M. Weber and E. Randolph Whitelaw Introduction An active and rapidly growing secondary market for life insurance emerged less

LEVELING THE NET SINGLE PREMIUM. - Review the assumptions used in calculating the net single premium.

LEVELING THE NET SINGLE PREMIUM CHAPTER OBJECTIVES - Review the assumptions used in calculating the net single premium. - Describe what is meant by the present value of future benefits. - Explain the mathematics

LEVELING THE NET SINGLE PREMIUM CHAPTER OBJECTIVES - Review the assumptions used in calculating the net single premium. - Describe what is meant by the present value of future benefits. - Explain the mathematics

MassMutual Whole Life Insurance

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

Life Settlements Product Overview

Life Settlements Product Overview Leveraging Life Settlements in Writing New Business Contents What is a Life Settlement? Case study Options for unwanted policies Who buys these policies? How does it work?

Life Settlements Product Overview Leveraging Life Settlements in Writing New Business Contents What is a Life Settlement? Case study Options for unwanted policies Who buys these policies? How does it work?

The Life Settlements Market

Consulting The Life Settlements Market An Actuarial Perspective on Consumer Economic Value By Deloitte Consulting LLP and The University of Connecticut Audit. Tax. Consulting. Financial Advisory. Table

Consulting The Life Settlements Market An Actuarial Perspective on Consumer Economic Value By Deloitte Consulting LLP and The University of Connecticut Audit. Tax. Consulting. Financial Advisory. Table

THE MATHEMATICS OF LIFE INSURANCE THE NET SINGLE PREMIUM. - Investigate the component parts of the life insurance premium.

THE MATHEMATICS OF LIFE INSURANCE THE NET SINGLE PREMIUM CHAPTER OBJECTIVES - Discuss the importance of life insurance mathematics. - Investigate the component parts of the life insurance premium. - Demonstrate

THE MATHEMATICS OF LIFE INSURANCE THE NET SINGLE PREMIUM CHAPTER OBJECTIVES - Discuss the importance of life insurance mathematics. - Investigate the component parts of the life insurance premium. - Demonstrate

Life Insurance Professional Analysis and Review

NATIONAL ASSOCIATION OF INSURANCE AND FINANCIAL ADVISORS FLORIDA 1836 Hermitage Blvd, Suite 200, Tallahassee, FL 32308 Contact: Paul S. Brawner (850) 422-1701 brawner@faifa.org This self study course is

NATIONAL ASSOCIATION OF INSURANCE AND FINANCIAL ADVISORS FLORIDA 1836 Hermitage Blvd, Suite 200, Tallahassee, FL 32308 Contact: Paul S. Brawner (850) 422-1701 brawner@faifa.org This self study course is

The secondary market for life insurance is changing the face. of financial services. Clearly, the secondary market s central

The market is open. Opportunity. The secondary market for life insurance is changing the face of financial services. Clearly, the secondary market s central premise that the value of life insurance is

The market is open. Opportunity. The secondary market for life insurance is changing the face of financial services. Clearly, the secondary market s central premise that the value of life insurance is

Life Settlements 101 Introduction to the Secondary Market in Life Insurance

Life Settlements 101 Introduction to the Secondary Market in Life Insurance Anita A Sathe, FSA, FCAS, MAAA Donald Solow, FSA, MAAA Michael Taht, FSA, FCIA, MAAA October 15, 2007 Presentation Outline History

Life Settlements 101 Introduction to the Secondary Market in Life Insurance Anita A Sathe, FSA, FCAS, MAAA Donald Solow, FSA, MAAA Michael Taht, FSA, FCIA, MAAA October 15, 2007 Presentation Outline History

Chapter 11. Agenda 2/12/2015. Premature Death. Life Insurance

Chapter 11 Life Insurance Agenda 2 Premature Death Financial Impact of Premature Death on Different Types of Families Amount of Life Insurance to Own Types of Life Insurance Premature Death 3 The death

Chapter 11 Life Insurance Agenda 2 Premature Death Financial Impact of Premature Death on Different Types of Families Amount of Life Insurance to Own Types of Life Insurance Premature Death 3 The death

FINANCIAL ANALYSIS ****** UPDATED FOR 55% BENEFIT ****** ****** FOR ALL SURVIVORS ******

FINANCIAL ANALYSIS ****** UPDATED FOR 55% BENEFIT ****** ****** FOR ALL SURVIVORS ****** This fact sheet is designed to supplement the Department of Defense brochure: SBP SURVIVOR BENEFIT PLAN FOR THE

FINANCIAL ANALYSIS ****** UPDATED FOR 55% BENEFIT ****** ****** FOR ALL SURVIVORS ****** This fact sheet is designed to supplement the Department of Defense brochure: SBP SURVIVOR BENEFIT PLAN FOR THE

Life Settlements 2012: the Secondary Market for Life Insurance Policies

Life Settlements 2012: the Secondary Market for Life Insurance Policies Executive Summary A Life Settlement is the sale of a life insurance policy to third party investors for an amount greater than the

Life Settlements 2012: the Secondary Market for Life Insurance Policies Executive Summary A Life Settlement is the sale of a life insurance policy to third party investors for an amount greater than the

Introduction to life insurance

1 Introduction to life insurance 1.1 Summary Actuaries apply scientific principles and techniques from a range of other disciplines to problems involving risk, uncertainty and finance. In this chapter

1 Introduction to life insurance 1.1 Summary Actuaries apply scientific principles and techniques from a range of other disciplines to problems involving risk, uncertainty and finance. In this chapter

The Potential Impact of Life Settlements on Life Insurance Companies

Sanghani 1 The Potential Impact of Life Settlements on Life Insurance Companies by Alpesh K. Sanghani An honors thesis submitted in partial fulfillment of the requirements for the degree of Bachelor of

Sanghani 1 The Potential Impact of Life Settlements on Life Insurance Companies by Alpesh K. Sanghani An honors thesis submitted in partial fulfillment of the requirements for the degree of Bachelor of

Heriot-Watt University. BSc in Actuarial Mathematics and Statistics. Life Insurance Mathematics I. Extra Problems: Multiple Choice

Heriot-Watt University BSc in Actuarial Mathematics and Statistics Life Insurance Mathematics I Extra Problems: Multiple Choice These problems have been taken from Faculty and Institute of Actuaries exams.

Heriot-Watt University BSc in Actuarial Mathematics and Statistics Life Insurance Mathematics I Extra Problems: Multiple Choice These problems have been taken from Faculty and Institute of Actuaries exams.

The secondary market for life insurance is changing the face. of financial services. Clearly, the secondary market s central

The market is open. Opportunity. The secondary market for life insurance is changing the face of financial services. Clearly, the secondary market s central premise that the value of life insurance is

The market is open. Opportunity. The secondary market for life insurance is changing the face of financial services. Clearly, the secondary market s central premise that the value of life insurance is

THE CONSTRUCTION OF A SURVIVORSHIP LIFE INSURANCE POLICY

THE CONSTRUCTION OF A SURVIVORSHIP LIFE INSURANCE POLICY PERTINENT INFORMATION Mr. and Mrs. Kugler are considering $1,000,000 of life insurance to provide estate liquidity at the survivor s death to cover

THE CONSTRUCTION OF A SURVIVORSHIP LIFE INSURANCE POLICY PERTINENT INFORMATION Mr. and Mrs. Kugler are considering $1,000,000 of life insurance to provide estate liquidity at the survivor s death to cover

CHAPTER 5 LIFE INSURANCE POLICY OPTIONS AND RIDERS

CHAPTER 5 LIFE INSURANCE POLICY OPTIONS AND RIDERS There are a number of policy options and riders that the purchasers of insurance need to understand. Obviously, life and disability agents need to have

CHAPTER 5 LIFE INSURANCE POLICY OPTIONS AND RIDERS There are a number of policy options and riders that the purchasers of insurance need to understand. Obviously, life and disability agents need to have

The Life Settlement Market, An Actuarial Perspective on Consumer Economic Value A Response

Life Settlement Consulting & Management, LLC The Life Settlement Market, An Actuarial Perspective on Consumer Economic Value A Response By: Darwin M. Bayston, CFA A study entitled, The Life Settlement

Life Settlement Consulting & Management, LLC The Life Settlement Market, An Actuarial Perspective on Consumer Economic Value A Response By: Darwin M. Bayston, CFA A study entitled, The Life Settlement

Life Settlements. Life Settlements Presentation

Life Settlements Brian Forman Actuaries Club of the Southwest June 10, 2010 Life Settlements Presentation History Sale of Policies Mathematics of Life Settlements Pricing of Life Settlements Current Marketplace

Life Settlements Brian Forman Actuaries Club of the Southwest June 10, 2010 Life Settlements Presentation History Sale of Policies Mathematics of Life Settlements Pricing of Life Settlements Current Marketplace

2) You must then determine how much of the risk you are willing to assume.

You must then determine how much of the risk you are willing to assume.") CHAPTER 4 Life Insurance Structure, Concepts, and Planning Strategies Where can you make a Simpler living as a needs financial planner? 1) Wealthy clients have a much higher profit margin. The challenge

CHAPTER 4 Life Insurance Structure, Concepts, and Planning Strategies Where can you make a Simpler living as a needs financial planner? 1) Wealthy clients have a much higher profit margin. The challenge

ETHICAL CONSIDERATIONS IN THE SECONDARY LIFE INSURANCE MARKETPLACE

ETHICAL CONSIDERATIONS IN THE SECONDARY LIFE INSURANCE MARKETPLACE Thomas L Virkler, JD CLU Partners Life Marketing Group THOMAS L. VIRKLER, JD CLU - Chief Marketing Officer, Partners Life Marketing Group

ETHICAL CONSIDERATIONS IN THE SECONDARY LIFE INSURANCE MARKETPLACE Thomas L Virkler, JD CLU Partners Life Marketing Group THOMAS L. VIRKLER, JD CLU - Chief Marketing Officer, Partners Life Marketing Group

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR Participate in your brighter future with Sun Life Financial. Participating life insurance is a powerful tool that protects

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR Participate in your brighter future with Sun Life Financial. Participating life insurance is a powerful tool that protects

LIFE INSURANCE KEY FACTS

GENERAL INSURANCE CONCEPTS LIFE INSURANCE KEY FACTS A condition that could result in a loss is known as an EXPOSURE. An insurer is responsible for all acts of their agents as long as the agent operates

GENERAL INSURANCE CONCEPTS LIFE INSURANCE KEY FACTS A condition that could result in a loss is known as an EXPOSURE. An insurer is responsible for all acts of their agents as long as the agent operates

Understanding Life Insurance

Understanding Life Insurance A Lesson in Traditional and Indexed Life Insurance 2012 VSA, LP Valid only if used prior to January 1, 2013. The information, general principles and conclusions presented in

Understanding Life Insurance A Lesson in Traditional and Indexed Life Insurance 2012 VSA, LP Valid only if used prior to January 1, 2013. The information, general principles and conclusions presented in

The Basics of Life Settlements

The Basics of Life Settlements AN EDUCATIONAL GUIDE FOR CONSUMERS THE VOICE OF THE INDUSTRY THE BASICS OF LIFE SETTLEMENTS The Basics of Life Settlements 1 The Concept of Life Settlements 4 Free Market

The Basics of Life Settlements AN EDUCATIONAL GUIDE FOR CONSUMERS THE VOICE OF THE INDUSTRY THE BASICS OF LIFE SETTLEMENTS The Basics of Life Settlements 1 The Concept of Life Settlements 4 Free Market

INSURANCE DICTIONARY

INSURANCE DICTIONARY Actuary An actuary is a professional who uses statistical data to assess risk and calculate dividends, financial reserves, and insurance premiums for a business or insurer. Agent An

INSURANCE DICTIONARY Actuary An actuary is a professional who uses statistical data to assess risk and calculate dividends, financial reserves, and insurance premiums for a business or insurer. Agent An

WHAT YOU SHOULD KNOW. About Buying Life Insurance. Life insurance is financial protection. It provides the

Life insurance is financial protection. It provides the resources your family may need to pay immediate and continuing expenses after you die. WHAT YOU SHOULD KNOW About Buying Life Insurance There are

Life insurance is financial protection. It provides the resources your family may need to pay immediate and continuing expenses after you die. WHAT YOU SHOULD KNOW About Buying Life Insurance There are

RULES OF THE DEPARTMENT OF INSURANCE DIVISION OF INSURANCE CHAPTER 0780-1-40 RELATING TO LIFE INSURANCE SOLICITATION TABLE OF CONTENTS

RULES OF THE DEPARTMENT OF INSURANCE DIVISION OF INSURANCE CHAPTER 0780-1-40 RELATING TO LIFE INSURANCE SOLICITATION TABLE OF CONTENTS 0780-1-40-.01 Purpose 0780-1-40-.05 General Rules 0780-1-40-.02 Scope

RULES OF THE DEPARTMENT OF INSURANCE DIVISION OF INSURANCE CHAPTER 0780-1-40 RELATING TO LIFE INSURANCE SOLICITATION TABLE OF CONTENTS 0780-1-40-.01 Purpose 0780-1-40-.05 General Rules 0780-1-40-.02 Scope

universal life wealth planner

universal life wealth planner 1 3 4 5 6 7 9 10 Your success and prestigious status can be demonstrated not only by possessing great fortune but also by wisely protecting, growing and passing on your

universal life wealth planner 1 3 4 5 6 7 9 10 Your success and prestigious status can be demonstrated not only by possessing great fortune but also by wisely protecting, growing and passing on your

Why Consider Life Settlement Options?

Why Consider Life Settlement Options? SITUATION Many people purchase life insurance initially for the right reasons. Life insurance is customarily purchased for planning needs that may span a time horizon

Why Consider Life Settlement Options? SITUATION Many people purchase life insurance initially for the right reasons. Life insurance is customarily purchased for planning needs that may span a time horizon

Do You Have the Right Life Insurance?

Do You Have the Right Life Insurance? Having adequate life insurance should be an important part of your financial planning. The type(s) you choose will depend on your needs and goals. Life insurance was

Do You Have the Right Life Insurance? Having adequate life insurance should be an important part of your financial planning. The type(s) you choose will depend on your needs and goals. Life insurance was

Custom Guarantee. Universal Life Insurance with a Death Benefit Guarantee 1. Marketing Guide

Custom Guarantee Universal Life Insurance with a Death Benefit Guarantee 1 Marketing Guide Marketing Custom Guarantee Uncertainty in life is guaranteed. No one can predict what changes may occur in his

Custom Guarantee Universal Life Insurance with a Death Benefit Guarantee 1 Marketing Guide Marketing Custom Guarantee Uncertainty in life is guaranteed. No one can predict what changes may occur in his

What You should Know. About Buying Life Insurance. Life insurance protects your financial future. It provides

Life insurance protects your financial future. It provides the resources your family or business may need to pay immediate and continuing expenses when you die. What You should Know About Buying Life Insurance

Life insurance protects your financial future. It provides the resources your family or business may need to pay immediate and continuing expenses when you die. What You should Know About Buying Life Insurance

Commissions and Fair Value

Plybon & Associates, Inc. 6518 Airport Center Drive Greensboro, NC 27409 336.292.9050 336.292.4618 Fax www.plybon.com Prepared and Researched by March 2014 Commissions are rarely discussed and frequently

Plybon & Associates, Inc. 6518 Airport Center Drive Greensboro, NC 27409 336.292.9050 336.292.4618 Fax www.plybon.com Prepared and Researched by March 2014 Commissions are rarely discussed and frequently

Simply put, a life settlement is the sale of an

LIFE SETTLEMENTS Understanding the Facts and Myths of This Secondary Insurance Product by Michael L. Frank Simply put, a life settlement is the sale of an unwanted, no longer effective life insurance policy.

LIFE SETTLEMENTS Understanding the Facts and Myths of This Secondary Insurance Product by Michael L. Frank Simply put, a life settlement is the sale of an unwanted, no longer effective life insurance policy.

CHAPTER 10 ANNUITIES

CHAPTER 10 ANNUITIES are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives of two or

CHAPTER 10 ANNUITIES are contracts sold by life insurance companies that pay monthly, quarterly, semiannual, or annual income benefits for the life of a person (the annuitant), for the lives of two or

Chapter 12. Life Insurance: An Introduction. Chapter 12 Learning Objectives. Life Insurance

Chapter 12 Life Insurance McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 12-1 Chapter 12 Learning Objectives 1. Define Life insurance and describe its purpose

Chapter 12 Life Insurance McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 12-1 Chapter 12 Learning Objectives 1. Define Life insurance and describe its purpose

LIFE INSURANCE. and INVESTMENT

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC GLOSSARY OF LIFE INSURANCE and INVESTMENT TERMS 2 Accident Benefit A benefit payable should death occur as the result of an accident. It may be a stand-alone

INVESTMENT SAVINGS & INSURANCE ASSOCIATION OF NZ INC GLOSSARY OF LIFE INSURANCE and INVESTMENT TERMS 2 Accident Benefit A benefit payable should death occur as the result of an accident. It may be a stand-alone

Discount Rates and Life Tables: A Review

Discount Rates and Life Tables: A Review Hugh Sarjeant is a consulting actuary and Paul Thomson is an actuarial analyst at Cumpston Sarjeant Pty Ltd Phone: 03 9642 2242 Email: Hugh_Sarjeant@cumsar.com.au

Discount Rates and Life Tables: A Review Hugh Sarjeant is a consulting actuary and Paul Thomson is an actuarial analyst at Cumpston Sarjeant Pty Ltd Phone: 03 9642 2242 Email: Hugh_Sarjeant@cumsar.com.au

Chapter 16 Fundamentals of Life Insurance

Chapter 16 Fundamentals of Life Insurance Overview This chapter begins a block of material on several important personal risks: premature death, poor health, and excessive longevity. This chapter examines

Chapter 16 Fundamentals of Life Insurance Overview This chapter begins a block of material on several important personal risks: premature death, poor health, and excessive longevity. This chapter examines

Life Insurance and Annuity Buyer s Guide Introduction

Life Insurance and Annuity Buyer s Guide Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as an aid to assist you in determining your insurance

Life Insurance and Annuity Buyer s Guide Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as an aid to assist you in determining your insurance

Life Insurance Buyer s Guide

Life Insurance Buyer s Guide This guide can show you how to save money when you shop for life insurance. It helps you to: - Decide how much life insurance you should buy, - Decide what kind of life insurance

Life Insurance Buyer s Guide This guide can show you how to save money when you shop for life insurance. It helps you to: - Decide how much life insurance you should buy, - Decide what kind of life insurance

A Consumer s Guide to Annuities

Insurance Facts for Pennsylvania Consumers A Consumer s Guide to Annuities 1-877-881-6388 Toll-free Automated Consumer Line www.insurance.pa.gov Pennsylvania Insurance Department Web site Accumulation

Insurance Facts for Pennsylvania Consumers A Consumer s Guide to Annuities 1-877-881-6388 Toll-free Automated Consumer Line www.insurance.pa.gov Pennsylvania Insurance Department Web site Accumulation

The Truth About INSURANCE

INSURANCE The Truth About Annuities are one of the least known, least understood and most underutilized financial instruments. Yet as Paul Goldstein explains, in certain circumstances annuities should

INSURANCE The Truth About Annuities are one of the least known, least understood and most underutilized financial instruments. Yet as Paul Goldstein explains, in certain circumstances annuities should

Viatical Settlements of Life Insurance in the United States

Viatical Settlements of Life Insurance in the United States Presentation at Universitaet Ulm May 2006 Dr. Krzysztof Ostaszewski, FSA, CFA, MAAA Actuarial Program Director Illinois State University Viatical

Viatical Settlements of Life Insurance in the United States Presentation at Universitaet Ulm May 2006 Dr. Krzysztof Ostaszewski, FSA, CFA, MAAA Actuarial Program Director Illinois State University Viatical

B1.03: TERM ASSURANCE

B1.03: TERM ASSURANCE SYLLABUS Term assurance Increasing term assurance Decreasing term assurance Mortgage protection Renewable and convertible term assurance Pension term assurance Tax treatment Family

B1.03: TERM ASSURANCE SYLLABUS Term assurance Increasing term assurance Decreasing term assurance Mortgage protection Renewable and convertible term assurance Pension term assurance Tax treatment Family

Life Insurance Tutorial & Calculation Worksheet

Life Insurance Tutorial & Calculation Worksheet Provided By NAVY MUTUAL AID ASSOCIATION Henderson Hall, 29 Carpenter Road, Arlington, VA 22212 Telephone 800-628-6011-703-614-1638 - FAX 703-945-1441 E-mail:

Life Insurance Tutorial & Calculation Worksheet Provided By NAVY MUTUAL AID ASSOCIATION Henderson Hall, 29 Carpenter Road, Arlington, VA 22212 Telephone 800-628-6011-703-614-1638 - FAX 703-945-1441 E-mail:

Article from: Reinsurance News. February 2010 Issue 67

Article from: Reinsurance News February 2010 Issue 67 Life Settlements A Window Of Opportunity For The Life Insurance Industry? By Michael Shumrak Michael Shumrak, FSA, MAAA, FCA, is president of Shumrak

Article from: Reinsurance News February 2010 Issue 67 Life Settlements A Window Of Opportunity For The Life Insurance Industry? By Michael Shumrak Michael Shumrak, FSA, MAAA, FCA, is president of Shumrak

Life Insurance Review

Life Insurance Review A thorough evaluation of your life insurance portfolio RELATIONSHIP MANAGEMENT EXPERIENCE PARTNERSHIPS CLIENTSOLUTIONS Purpose Our goal is to provide an objective life insurance policy

Life Insurance Review A thorough evaluation of your life insurance portfolio RELATIONSHIP MANAGEMENT EXPERIENCE PARTNERSHIPS CLIENTSOLUTIONS Purpose Our goal is to provide an objective life insurance policy

Frequently Asked Questions Individual Life Insurance

Illinois Insurance Facts Illinois Department of Insurance Frequently Asked Questions Individual Life Insurance Updated January 2010 Note: This information was developed to provide consumers with general

Illinois Insurance Facts Illinois Department of Insurance Frequently Asked Questions Individual Life Insurance Updated January 2010 Note: This information was developed to provide consumers with general

Whole Life Legacy 10 Pay Basic Life Insurance Illustration

Whole Life Legacy 10 Pay Basic Prepared for: d Client Male, Age 5 Presented by: Michael Fliegelman CLU, ChFC, AEP, RFC Independent Insurance And Financial Consulting 5 Harborfields Ct Greenlawn, NY 11740

Whole Life Legacy 10 Pay Basic Prepared for: d Client Male, Age 5 Presented by: Michael Fliegelman CLU, ChFC, AEP, RFC Independent Insurance And Financial Consulting 5 Harborfields Ct Greenlawn, NY 11740

Life Insurance Technical Manual

Life Insurance Technical Manual Technical issues surrounding one of the biggest assets owned by successful clients life insurance. Presented by: Daniel Tasciotti, CLU, ChFC, CFP, AEP, MBA There are worse

Life Insurance Technical Manual Technical issues surrounding one of the biggest assets owned by successful clients life insurance. Presented by: Daniel Tasciotti, CLU, ChFC, CFP, AEP, MBA There are worse

20 Ways to Reduce and Effectively Use Insurance Premiums

Free Review: Compliments of YourBusinessLibrary.com For Your Individual Use Only The Business Library Resource Report #41 20 Ways to Reduce and Effectively Use Insurance Premiums Getting the Most Bang

Free Review: Compliments of YourBusinessLibrary.com For Your Individual Use Only The Business Library Resource Report #41 20 Ways to Reduce and Effectively Use Insurance Premiums Getting the Most Bang

Life Insurance and Annuity Buyer s Guide

Life Insurance and Annuity Buyer s Guide Published by the Kentucky Office of Insurance Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as

Life Insurance and Annuity Buyer s Guide Published by the Kentucky Office of Insurance Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life Insurance: A Lesson in Life Insurance If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Insurance Questions

Understanding Life Insurance: A Lesson in Life Insurance If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Insurance Questions

Life insurance provides

ADVISOR USE ONLY 1 Impact of 217 tax changes on life insurance THE DETAILS Life insurance provides protection, but some policies also allow clients to accumulate savings on a tax-preferred basis. The Income

ADVISOR USE ONLY 1 Impact of 217 tax changes on life insurance THE DETAILS Life insurance provides protection, but some policies also allow clients to accumulate savings on a tax-preferred basis. The Income

Insured Annuities: Beyond the Basics

Insured Annuities: Beyond the Basics Achieving a great after-tax return on fixed-income assets John M. Nicola, CLU, CHFC, CFP Table of Contents Introduction.................................. 3 Insured

Insured Annuities: Beyond the Basics Achieving a great after-tax return on fixed-income assets John M. Nicola, CLU, CHFC, CFP Table of Contents Introduction.................................. 3 Insured

Life Settlements: Discover Your Client's Unknown Asset

Life Settlements: Discover Your Client's Unknown Asset MODERATOR Darwin Bayston, CFA President and CEO Life Insurance Settlement Association PANELISTS Michael Freedman President GWG Life Dan Young Vice

Life Settlements: Discover Your Client's Unknown Asset MODERATOR Darwin Bayston, CFA President and CEO Life Insurance Settlement Association PANELISTS Michael Freedman President GWG Life Dan Young Vice

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

FINANCIAL REVIEW. 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

The Problem and the Appropriate State Response. Why is STOLI a problem?

STOLI: The Problem and the Appropriate State Response AALU, NAIFA, and ACLI believe that stranger-originated life insurance ( STOLI ) represents a threat to both consumers and the life insurance industry.

STOLI: The Problem and the Appropriate State Response AALU, NAIFA, and ACLI believe that stranger-originated life insurance ( STOLI ) represents a threat to both consumers and the life insurance industry.

Life Insurance as an Asset Class: A Predictable Asset for Unpredictable Times

Life Insurance as an Asset Class: A Predictable Asset for Unpredictable Times This material is not intended to be used to avoid tax penalties. It was prepared to support the promotion or marketing of the

Life Insurance as an Asset Class: A Predictable Asset for Unpredictable Times This material is not intended to be used to avoid tax penalties. It was prepared to support the promotion or marketing of the

Life Settlements Can be a Life Saver

Life Settlements Can be a Life Saver For many advisors the concept of selling an existing life insurance policy is new. Just asking the question sounds strange. Why would a client want to sell a life insurance

Life Settlements Can be a Life Saver For many advisors the concept of selling an existing life insurance policy is new. Just asking the question sounds strange. Why would a client want to sell a life insurance

$2,000 (premium) multiplied by 6 months (period remaining), divided by 12 months (number of months premium covers), or

multiplied by 6 months (period remaining), divided by 12 months (number of months premium covers), or") client who has a personally owned life insurance policy comes to you. You convince her to either sell or gift the policy to an irrevocable life insurance trust (ILIT). You need to get the value of the

client who has a personally owned life insurance policy comes to you. You convince her to either sell or gift the policy to an irrevocable life insurance trust (ILIT). You need to get the value of the

Foresters Advantage Plus Producer Guide

Foresters Advantage Plus Producer Guide Whole Life Insurance This guide is for information purposes only and is intended to answer your questions and provide ideas to help you sell Foresters Advantage

Foresters Advantage Plus Producer Guide Whole Life Insurance This guide is for information purposes only and is intended to answer your questions and provide ideas to help you sell Foresters Advantage

3158 Des Plaines Avenue, Suite 209 Voice: (847) 296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG

296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG") SSCG Actuarial Solutions & Software Innovations 3158 Des Plaines Avenue, Suite 209 Voice: (847) 296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG Doris J. Bloom, FLMI web

SSCG Actuarial Solutions & Software Innovations 3158 Des Plaines Avenue, Suite 209 Voice: (847) 296-8890 Des Plaines, IL 60018-4222 Fax: (847) 296-8871 Toll Free: (888) 658-SSCG Doris J. Bloom, FLMI web

VALUATION OF LIFE INSURANCE POLICIES MODEL REGULATION (Including the Introduction and Use of New Select Mortality Factors)

") Table of Contents Model Regulation Service October 2009 VALUATION OF LIFE INSURANCE POLICIES MODEL REGULATION (Including the Introduction and Use of New Select Mortality Factors) Section 1. Section 2.

Table of Contents Model Regulation Service October 2009 VALUATION OF LIFE INSURANCE POLICIES MODEL REGULATION (Including the Introduction and Use of New Select Mortality Factors) Section 1. Section 2.

Life Insurance Buyer's Guide

United of Omaha Life Insurance Company Life Insurance Buyer s Guide Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

United of Omaha Life Insurance Company Life Insurance Buyer s Guide Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

Finance 160:163 Sample Exam Questions Spring 2003

Finance 160:163 Sample Exam Questions Spring 2003 These questions are designed to test your understanding of insurance operations within the context of life and health insurance. Each question is given

Finance 160:163 Sample Exam Questions Spring 2003 These questions are designed to test your understanding of insurance operations within the context of life and health insurance. Each question is given

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

WHAT IS LIFE INSURANCE?

UNDERSTANDING LIFE INSURANCE Presented by The Kansas Insurance Department WHAT IS LIFE INSURANCE? a. Insurance Contract issued by an Insurance Company. b. Premiums paid under the contract provide for a

UNDERSTANDING LIFE INSURANCE Presented by The Kansas Insurance Department WHAT IS LIFE INSURANCE? a. Insurance Contract issued by an Insurance Company. b. Premiums paid under the contract provide for a

FREE LIFE INSURANCE PRACTICE EXAM

FREE LIFE INSURANCE PRACTICE EXAM We offer an online video L&H exam prep course that includes over 10 hours of instruction. Our full pdf study manual and over 600 questions are also included. Please go

FREE LIFE INSURANCE PRACTICE EXAM We offer an online video L&H exam prep course that includes over 10 hours of instruction. Our full pdf study manual and over 600 questions are also included. Please go

Life Settlements THE LIFE SETTLEMENT AUTHORITY

Life Settlements THE LIFE SETTLEMENT AUTHORITY Experience. Authority. That Settles It. It takes more than volume and experience to be the market authority; it takes a commitment to the constant improvement