Maine Bureau of Consumer Credit Protection

|

|

|

- Prudence Stone

- 8 years ago

- Views:

Transcription

1 1

2 Maine Bureau of Consumer Credit Protection Toll-free Maine Consumer Assistance (1-800-DEBT-LAW) TTY users call Maine relay 711 Maine Foreclosure Prevention Hotline NO-4-CLŌZ ( ) The Maine Bureau of Consumer Credit Protection was established in 1975 to enforce a wide variety of consumer financial protection laws, including: -Consumer Credit Code -Truth-in-Lending Act -Fair Credit Billing Act -Truth-in-Leasing Act -Fair Credit Reporting Act -Fair Debt Collection Practices Act - Plain Language Contract Law The Bureau conducts periodic examinations of creditors to determine compliance with these laws; responds to consumer complaints and inquiries; and operates the state s foreclosure prevention hotline and housing counselor referral program. The Bureau also conducts educational seminars and provides speakers to advise consumers and creditors of their legal rights and responsibilities. DOWNEASTER COMMON SENSE GUIDE: CREDIT REPORTS AND CREDIT SCORES By David Leach, MPA and Abigail Pratico Editing and Production Assistance by Steven Lemieux, MBA Cover Image by Edward Myslik & Steven Lemieux, MBA Copyright 2014 Bureau of Consumer Credit Protection, State of Maine The contents of this book may be reprinted, with attribution. Second Printing July 2015 William N. Lund Superintendent December 2014 Maine residents can obtain additional free copies of this booklet by contacting the Bureau of Consumer Credit Protection at or toll-free at Non-Maine residents may purchase the publication for $6 per copy, or at a volume discount of $4 per copy on orders of 50 or more. Shipping fees are included in the prices listed. 2

3 Dear Maine Consumers, This State of Maine publication presents must know information on consumer credit reports and credit scores. Creditors, insurance companies, banks, employers and landlords routinely use credit report information when they make decisions on loan approval or denial, insurance premium costs, hiring decisions and approval for housing. This guide describes the basic facts of credit bureau reports and credit scores: how they work, steps for obtaining copies of your reports, how you can challenge inaccurate items, and strategies to ensure that your credit report and score present the most accurate representation of your credit-worthiness. As authors of this guide, we hope to expand your knowledge of how credit reports and credit scores work, and to empower you to quickly and efficiently correct errors and omissions in your reports! David Leach, MPA Principal Consumer Credit Examiner Abigail Pratico Margaret Chase Smith Summer Intern,

4 Table of Contents Part 1: Credit Reports and Credit Scores 1 Credit Reporting Agencies Tradelines FICO Credit Score Part 2: Ordering and Reviewing Your Credit Report 6 Fair Credit Reporting Act Rights How to Order Your Credit Report Correcting Your Credit Reports Frivolous Requests Part 3: Scams and Identity Theft 10 Credit Repair Scams Identity Theft Credit Monitoring Glossary and Resources 12 Glossary of Common Terms Found on Credit Reports Sample Forms (File Freeze and Free Annual Credit Report Request) Publications Consumer Resources 4

Publications Consumer Resources 4")

5 Credit Reports and Credit Scores A credit report is like an academic transcript;, but rather than listing course grades it lists a person s debts. Lenders believe the best indicator of future loan performance is past loan performance. Credit reports show a person s financial reliability. They allow potential creditors to assess the fiscal risk presented by doing business with a person. Credit reporting agencies (a.k.a. credit bureaus) for-profit companies that specialize in compiling data for use by creditors and other authorized users produce credit reports. There are three major credit bureaus in the United States: Experian, TransUnion and Equifax. The data collected on a credit report is voluntarily reported by a person s creditors. Credit bureaus compete with each other to compile the most comprehensive and accurate information possible. Businesses that need to see consumers credit reports (e.g., mortgage companies, landlords or auto dealers) pay credit bureaus for access to that information. Credit bureaus that consistently offer the most complete and accurate files to creditors attract more business. Because of this, a credit bureau rarely shares information with another credit bureau. As such, credit reports produced by different companies often contain slightly different information. Tradelines A credit report contains seven to ten years worth of information, presented in the form of tradelines records of a person s current and past monetary obligations. Individual tradelines may include the names of companies a consumer has (or had) account with, the dates accounts were opened, credit limits, types of accounts, balances owed and payment histories. Auto loans, credit cards and mortgages are all common types of tradelines. Your credit report will show most if not all your accounts open or closed. Most tradelines, positive or negative, remain on a person s credit report for up to seven years. Lenders like to see positive tradelines on credit reports tradelines showing consistent on-time repayment of debt. Many credit reports also include negative tradelines. Negative tradelines may make potential creditors hesitant to lend to you and may affect your ability to get a job or rent an apartment. Common negative tradelines include: Repossessions: Repossessions and deficiency balances are major negative tradeline items that can severely affect a person s credit history. If money is still owed to a creditor after a repossession has occurred, the remaining balance may be sent to collections. If so, a separate 1

6 collection account may appear on the borrower s credit report. Foreclosures: A foreclosure is one of the harshest trade lines that can appear in a credit report. Foreclosure-related tradelines may cause a consumer s credit score to drop by as much as 300 points. Bankruptcies: Filing for bankruptcy can help consumers to discharge overwhelming unsecured debt, but can also make it difficult to establish new credit. Bankruptcies can remain on a credit report for up to 10 years. Tradelines affected by a bankruptcy will remain on your credit report with a status of included in bankruptcy. Tax Liens: A tax lien occurs when the local, county, state, or federal government claims ownership interest in a person s property (e.g., land or other possessions), salary or tax refund to secure money for unpaid debts. If left unpaid, tax liens may threaten ownership of your property. The three big credit bureaus state they will remove unpaid tax liens 15 years after their filing date. Removal of unpaid tax liens is not required by law. As such, unpaid tax liens could (potentially) remain on a credit report forever. which you can get for free once each year, credit bureaus will charge you a fee for access to your credit score. A credit score is a numerical representation of a person s financial responsibility, calculated using the information on their credit report. The most widespread credit scoring model was developed by Fair Isaac Corporation ( FICO ). FICO scores range from 300 to 850. The higher the score, the greater a borrower s presumed creditworthiness. The FICO model takes several different factors into consideration when calculating a person s credit score, each of which is weighted differently for different groups of people (i.e., an established homeowner s information is weighted differently than that of a recent high school graduate). For most people: 35% of their FICO score represents payment history. 30% represents amounts owed. 15% represents length of credit history. 10% represents new credit. 10% represents the types of credit used. Credit Scores Credit reports and credit scores are closely related. Your credit score is an important tool for understanding your financial obligations. It also enhances your ability to borrow at the best rates and terms available. Unlike credit reports, 2

7 Credit scores are a reliable way for lenders to determine the risk of a borrower defaulting or becoming delinquent. The lower the credit score, the higher the risk to the lender (and the higher the interest rate charged). Students entering the workforce often begin adulthood relatively low credit scores. Over time the addition of positive trade lines raises their scores, allowing easier access to financing. Credit accounts usually feature a grace period during which most creditors will not report a borrower to the major credit reporting agencies as being late on their payments. To improve your credit score: Pay your loans on or before their due date set up payment reminders or automatic payments to stay current; Keep your credit card balances at no more than 1/3 rd of the credit limit amount, 10% or less if you can manage; Limit yourself to three or fewer credit cards; Try to maintain your oldest credit card accounts if the terms (e.g., APRs, annual fees) of those accounts are favorable; Reduce debt (credit balances) on other loans as much as possible; and Check your credit report at least annually for any signs of identity theft, errors or omissions Co-signing Consumers unable to qualify for loans on their own are often told that they must find a cosigner to act as a guarantor. Co-signers undergo the same underwriting review process as applicants, including a hard pull on their credit report. If you are considering co-signing on a loan, be cautious. If the primary borrower fails to make payments, the creditor will hold you responsible for the loan. The delinquency will appear on your credit report, negatively affecting your ability to get new credit. Authorized Users An authorized user is a someone who has been given permission to use a credit card. An authorized user holds a credit card with theirs name on it, but is not legally responsible for repaying the card s balance. Not all creditors report authorized user accounts to credit bureaus. If a creditor does report these accounts, it can affect the user s credit score. Since authorized users are not legally responsible for an account, credit bureaus generally remove these tradelines if the account becomes delinquent. If an authorized user account is not automatically removed from your credit report following a delinquency, contact the lender or file a dispute with the credit bureau (see Correcting Your Credit Reports, pg. 7). 3

8 Too Many Tradelines? Some time ago, a recent college grad reported she was denied a loan for a car. She had good credit and had earned an advanced degree from a prestigious university. The woman opened eight credit card accounts, assuming the more accounts she had the better her chances for loan approval. The cards were active, but had not been used. The lender that reviewed her application noticed the woman s lines of credit amounted to more than $70,000 in potential debt. If she maxed out her cards, the debt could equal a medium-sized mortgage! The Bureau advised the woman to close out all but two or three of the oldest credit card accounts, and to reduce the limits on the remaining cards to around $2,000. She was also advised to contact the lender before doing so to see if closing the accounts would make a difference in approving her application. A week later, the auto loan was approved! Too many people spend money they haven t earned, to buy things they don t want, to impress people they don t like Will Rogers Opting Out: Stop or Reduce Pre-Approved Credit Offers Under the Fair Credit Reporting Act ( FCRA ), you have the right to opt out of receiving prescreened and preapproved credit and insurance offers permanently, or for five years. Opting out will remove your name from lists supplied by the major consumer reporting agencies to businesses that may perform soft pulls on your credit (see pg. 8). To opt out of preapproved credit offer, visit or call OPT- OUT ( ). Be prepared to provide personal information, including your full name, Social Security number, date of birth, and address. If you choose to opt out permanently, you will need to confirm your request in writing by submitting a signed permanent opt out form, which will be provided after submitting your online request. 4

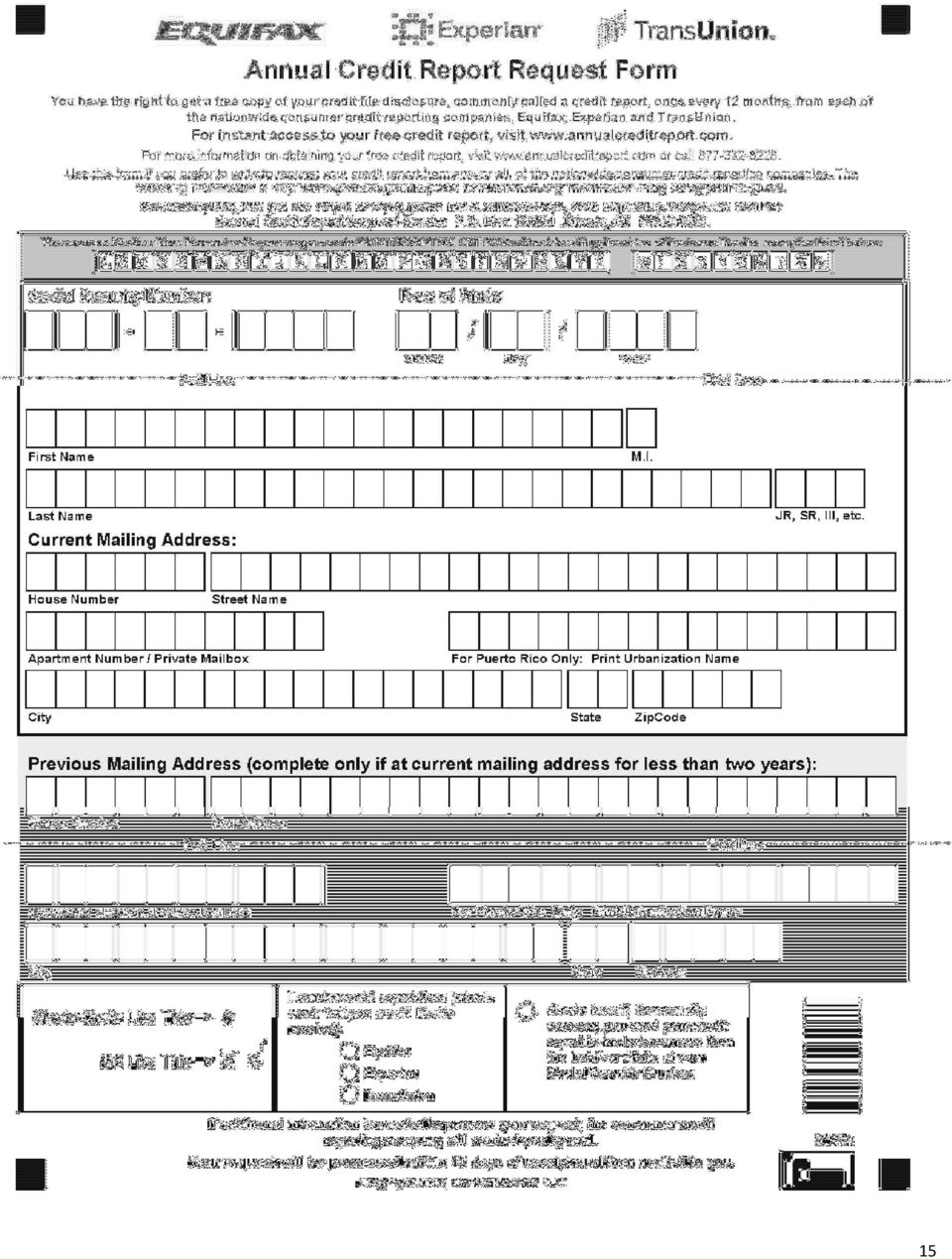

9 Ordering and Reviewing Your Credit Report Under the Fair Credit Reporting Act (FCRA), you can request one free credit report from each of the three major credit bureaus every 12 months. Consumers denied credit also have the opportunity to order a copy of the credit report utilized by the lender, for free, if the lender based part of their decision on the information contained in that report. To access your free credit reports, you will need to provide personal identification, including your name, Social Security number, date of birth and address. Our agency recommends that you order a single credit report from Experian, Equifax or TransUnion once every four months, switching credit bureaus each time. This interval will allow you to keep a close eye on your credit reports and tradelines, letting you catch errors, omissions or other issues quickly, since major tradeline errors or omissions will likely appear on credit reports from all three companies. Order by Phone: To order your free annual credit report: Order by Mail: Annual Credit Report Request Service P.O. Box Atlanta, GA (see pg. 17 for a request form) Reviewing Your Credit Report A credit report does not make for easy reading; they are technical by nature and include codes that require interpretation to be understood. A key code is typically located on the first page of your report, as well as a brief description of the type of information contained in each field. Refer to this key if you become confused while examining your credit report. Credit bureaus use similar codes, however the credit reports supplied by each credit bureau are formatted differently. Some of the first information you will encounter while looking over your credit report is your personal information. Personal information is used to identify and differentiate you from other people who may share your name. This information includes your name, address, Social Security number, date of birth and other information reported by creditors and employers. You may also find a Order Online: 5

10 confirmation number or report number on the first page of your credit report. Take special note of it; you may need that number to correct any errors you find on your report. As you delve further into your credit report you will begin to encounter tradelines - entries supplied by a creditor to your report describing your account status, payment history and other details specific to the account. Tradelines are usually arranged by lender, in alphabetical order. Beneath the current information about your account will be a summary of that tradeline s historical information - a record of your payments (or lack thereof) dating back up to seven years. Pay close attention to the information recorded for each tradeline. According to the Federal Trade Commission (FTC), one in four consumers has an error on their credit report that may affect their credit score. After the final tradeline, there will be a list of inquiries - requests by persons or companies who have recently checked your credit. Some, but not all, inquiries have an effect on your credit score. Hard inquiries ( hard pulls ) can only occur after you authorize them in writing such as when you apply for credit by filling out an application or authorization form. Hard inquiries also occur if a business reviews your credit, with your authorization, as part of a transaction that may affect your finances, such as renting an apartment or leasing a vehicle. Each individual hard inquiry that occurs without the extension of credit may lower your credit score between one and five points. Multiple hard pulls can occur if you shop around for rates and terms on consumer loans (e.g., auto loan) or mortgages. If credit is extended within 30 days for a consumer loan or 45 days for a mortgage loan, these hard pulls Your Fair Credit Reporting Act Rights You have the right to be notified if information in your file has been used to increase cost to you, or deny you a benefit. You have the right to know what s in your file You have the right to dispute incorrect or incomplete file information You can opt out of pre-screened offers (see pg. 5) Consumer reporting agencies must correct or delete inaccurate information upon request Consumer agencies must not report outdated, negative information Access to your file is limited to authorized users to whom you have given permission You must give consent for reports to be provided to employers You may seek damages from violators of your FCRA rights 6

dating back up to seven years.")

11 will count as a single inquiry on your credit report. If credit is not extended, your credit score could be damaged. The algorithms used to create credit scores treat each individual credit inquiry without the extension of credit as a declination by the lender. Some consumers report having credit scores drop by 30 or more points if credit is not extended after their loan applications have been shotgunned (sent out to several potential lenders at once). Soft inquiries ( soft pulls ) are not considered to be complete reviews of your credit, but rather a peek at your credit score and your personal profile. They may be initiated by marketing companies that have an existing relationship with a creditor with which you have accounts, or businesses trying to find potential customers for goods and services (e.g., preapproved credit cards or insurance). Soft pulls do not have a negative impact on your credit score. Correcting Your Credit Reports About one-quarter of all credit reports contain at least one error. If you find errors on your credit report, there are steps you can take to resolve the issues. The Bureau of Consumer Credit Protection enforces the federal and Maine Fair Credit Reporting Act (FCRA) in the state of Maine. The FCRA allows Frivolous FCRA Requests consumers to challenge errors or omissions on their credit reports, empowering consumers to petition the major credit reporting agencies to investigate claims of misreported tradelines, failure to report credit accounts and other issues. To have a credit bureau begin an investigation into errors on your credit report, you must file a written request with the company. In addition to noting the disputed or missing tradelines you wish to have investigated, you must include information needed to identify yourself (full name, date of birth, Social Security number, copy of your driver s license, and a copy of a utility bill containing your street address). Be sure to sign your name before submitting your request to the credit bureau. Within five days of receiving your request, the credit bureau must send a notice to the company whose tradelines you are disputing. The credit bureau must investigate your claim within 30 days, although it can extend the investigation for up to 15 days beyond the initial 30 if the investigation is ongoing. Upon completion of its investigation, the credit bureau will provide the results of the investigation to you, as well as free copy of your amended credit report (if the investigation led to an update). At your request, the credit Some consumers have items on their credit reports which require investigation. The FCRA does not allow you the right to challenge every trade line on your credit report as being inaccurate for the purpose of overwhelming the credit bureau, causing the credit bureaus to miss their mandated correction deadline. The exception to this frivolous rule is when identity theft occurs and there may be dozens of incorrect fraud-related items, all of which must be investigated. 7

are not considered to be complete reviews of your credit, but rather a peek at your credit score and your personal profile.")

12 bureau must send notices of credit report corrections to anyone who received your report in the last 6 months. If your request for correction is a result of a recent credit application where the error was discovered, provide the creditor with a copy of your amended credit report. That creditor may then re-access your credit to validate the change. their FCRA rights themselves, at least initially, by attempting to correct errors in their credit reports. Our agency can also help Maine consumers challenge any remaining items that are in dispute, without cost. Telling Your Side of the Story The results of an investigation into tradelines on a credit report do not always change the reporting of the items in question. The FCRA allows a consumer to write up to a one hundred-word explanation for a trade line that remains in dispute, which will be attached to the credit report. This provision provides consumers the ability to explain the dispute, in writing, in their own words. While you can challenge items on your credit report yourself for free, there are businesses that will perform this service for a fee. The Bureau recommends that consumers exercise I ve always advocated doing everything possible to pay off credit card balances. It s good financial management, and the ticket to a strong credit score Suze Orman Non-Public Information Every year, financial institutions send their clients written notices allowing consumers to opt out of sharing consumers non-public information (NPI) with non-affiliated third parties who may seek to purchase this information. NPI consists of data about that is not freely available to the public. This information can be quite specific, including your full name, date of birth, Social Security number, income level, account numbers, credit and debit card purchases or payment history on loans. The Gramm-Leach-Bliley Act, enacted November 1999, mandates that all financial institutions send this notice each year. Alternatively, some financial institutions may post privacy notices online, so long as they include information on where to find the notice in regular communications (e.g., billing statements), along with information on how to request a paper copy of the notice. 8

13 Part 3: Scams and Identity Theft Unfortunately, the Internet is full of scammers posing as legitimate credit repair organizations, with two intentions: to steal the victim s identity through disclosure of personal financial information and to take consumers money without providing any services. Victims of debt relief and credit repair scams often lose hundreds or thousands of dollars before seeking help from authorities. There are a number of credit repair agencies licensed by the Bureau of Consumer Credit Protection to work with Maine consumers to amend their credit reports. If you need assistance finding a legitimate credit repair agency, contact the Bureau at Identity Theft The FBI estimates that 13.1 million U.S. residents have their identities stolen every year, for a combined annual loss of over $24 billion. That means every year each of us has roughly a How to Spot a Credit Repair Scam 1 in 24 chance of having our identity stolen. Don t take chances! If you believe your identity has been stolen: Contact your financial institution(s) and freeze, place a fraud alert or request closure on any accounts that may be affected. If you disclosed banking information to an unknown caller, act immediately every second counts! File a report with law enforcement (local police department, county sheriff, or the Maine State Police). Be sure to keep a copy of the police report it s important for correcting your credit report and for stopping debt collectors calling about debts you don t owe. Place a fraud alert on your credit reports to tip off anyone who requests your credit history that you may be a victim of fraud. The Credit Repair Organization Act (CROA) prohibits upfront or advance fees for credit repair services. Legitimate licensed credit repair agencies will never ask for upfront or advance fees before starting their services. Scammers, however, often demand immediate wire transfers, electronic access to consumers bank accounts or bank or postal money orders to get things started. They will also try to get consumers to disclose Social Security number, date of birth, full name, street address, and bank account number and transit and routing number. Trust your instincts. If something feels wrong, it probably is. If you think you ve encountered an unlicensed or scam credit repair company, contact the Bureau of Consumer Credit Protection at

14 The three major credit reporting agencies (Equifax, Trans Union, Experian) have divisions that investigate allegations of identity theft and fraud. Equifax Information Services P.O. Box Atlanta, GA CreditInvestigation Experian P.O. Box 4500 Allen, TX TransUnion LLC P.O. Box 2000 Chester, PA fraud.transunion.com Place file freezes on your credit reports. A file freeze locks down your credit report, preventing consumer reporting agencies from releasing your information to a third party without your authorization. As of October 15, 2015, Maine consumers have the right to place a free file freeze on their credit reports at each of the three major credit reporting agencies. See pg. 15 for a file freeze form (or contact the Maine Bureau of Consumer Credit Protection at ). Contact the Federal Trade Commission s Identity Theft Hotline at (dial 0 to reach a live customer service representative). For more information on identity theft and financial scams, order a free copy of the Downeaster Common Sense Guide: Gone Phishing Identifying and Avoiding Consumer Scams by contacting the Bureau at , or ordering though our website at publications.htm. Identity Theft Protection and Credit Monitoring Services Many businesses offer identity theft protection and credit monitoring services. If you chose to have a business monitor your credit, you will be notified of irregularities in your accounts and, in some cases, be provided with continual credit report access, identity theft insurance coverage and/or other services for a fee. When making your decision, remember that FCRA allows you free access to your reports from each of the major credit reporting agencies (Experian, Equifax, Trans Union) once every 12 months (see pg. 6), allowing you to monitor your credit at no cost. Additionally, the Truth in Lending Act limits your liability on credit card loss or theft to $50 per card, and most card issuers will charge you nothing for unauthorized charges if you are the victim of loss or theft due to fraud, identity theft, or most other criminal acts. If you suspect that there are unauthorized charges on your credit card, notify your credit card issuer immediately. 10

15 Maine s New File Freeze Law As of October 15, 2015, Maine consumers have the right to place free file freezes on their credit reports with each of the three major credit reporting agencies: Equifax, Experian and TransUnion. A file freeze may be placed by telephone, through the credit reporting agencies secure websites, or in writing. If you try to place a file freeze online or by phone, be prepared to provide personal information. The credit reporting agency will need it to confirm your identity. When writing, ask the agency to freeze your file under Maine s new file freeze law. Make sure to provide the credit reporting agency with your Social Security number, your date of birth, and your mailing and street addresses. Don't forget to sign the letter! The credit reporting agency will mail you a personal identification number ( PIN ). The credit reporting agency will provide instructions for lifting the security freeze with your PIN. Save your PIN - you will need it to remove the file freeze. Your file freeze will remain active until you tell the credit reporting agency to lift it. Under Maine law, there is no fee for freezing or unfreezing your credit file. To place your free file freeze, contact: Equifax PO Box Atlanta, GA Experian PO Box 4500 Allen, TX TransUnion PO Box 2000 Chester, PA No Man s Credit is ever as good as his money. -E.W. Howe 11

16 Glossary of Common Terms Found on Credit Reports Account Closed by Consumer: Frequently associated with credit card accounts, reflects an action taken by the consumer cardholder to pay off then close their credit card account. Account in Good Standing: The trade line/ credit account is active and is being paid as agreed or current / on-time. Account Number: The account number as reported by the creditor. Actual Payment Amount: The amount the consumer last paid on this trade line account. Amount Past Due: The delinquent amount, expressed in dollars, as of the last date of reporting. Balance Amount: The total amount owed on that trade line account at the date of the last reporting period. Bankruptcy: A legal status of a person who has applied to federal court to discharge debts they cannot pay. Charge-off: Frequently associated with credit card accounts, the original lender/creditor has given up trying to collect this debt, and has taken a loss by charging this account off their books. Charge-off amounts are still owed, and are frequently sold to debt buyers or debt collectors. Civil Action: A court action against a consumer. Collection Account: Loans, utility bills, or medical bills that have been written/charged off by the original creditor or company, and referred to a third-party debt collector. Credit Limit: Typically associated with a credit card or home equity line of credit, the highest balance allowed by the creditor. Creditor Class: The type of company (bank, credit union, IRS, etc.) reporting the trade line account. Current (Account) Status: Whether the trade line/credit account is open, closed, in collection, or in charge-off status. Date of First Delinquency: The date this account was first reporting as being delinquent. Date of Major Delinquency: The first date this account reported a major delinquency (60 or more days late) Date Opened/Closed: The date the credit account was established or terminated. Default: A loan or mortgage is in default when a consumer has failed to make payments when due, but the account has not yet been sent to collections. 12

17 Deferred Payment Date: When a lender agrees to let the consumer make a payment (mortgage, auto, credit card) after the standard payment deadline date. Deficiency Balance: After a vehicle or other collateral is repossessed and sold, the negative balance which exists if the sale price of the collateral (at auction) is not sufficiently large enough to pay off the loan s balance, plus all the repossession fees (towing, storage, and auctioneer s fees). Discharge: Often associated with bankruptcy, a court action excusing a consumer from additional payments on a debt. Dismissed: When the federal courts do not allow the consumer to continue with his or her bankruptcy petition. Foreclosure: The legal process required for the lender to take ownership of a home pledged as collateral on a residential mortgage loan. Generation Identifier: Jr., Sr., II, III, etc. High Credit: The highest amount charged or borrowed. Inquiry (Hard Pull): When an authorized creditor (e.g., after you sign on a loan application) accesses your credit history. Each hard pull results in an approximate 2-point deduction of your credit score for a limited period of time. Inquiry (Soft Pull): When a creditor reviews your credit history in order to offer you a prescreened offer (credit card / instant loan check) that you have not ordered. Soft pull inquiries have no positive or negative effect on your credit scores. Installment Loan: Unlike revolving loans, an installment loan (mortgage or auto loan, for example) has a fixed term (12, 24, 36, 48 months or more) and (if the interest rate is fixed, not variable) a fixed monthly payment. Judgment: A court decision against a debtor. Last Reported: The last month or year the creditor on a trade line/account sent data to the credit reporting agency. Lien: A legal claim filed against a property owned by a consumer for failure to repay a loan or tax obligation. After judgment in court, some credit card lenders place liens on consumers homes or vehicles requiring moneys from the sale of a home or car be applied to the outstanding debt before the new owner of the home or vehicle can assume legal title or ownership of that item. Liens also commonly result from an unpaid federal, state, or municipal tax obligations. Months Reviewed: The time period an account/trade line has been reported to a credit bureau agency. Original amount: The original balance of the credit extension. Generally associated with installment loans (auto, home, or personal). Paid as Agreed : The borrower made (or is 13

18 making) all their loan payments on or before the due dates. Paid Less Than Full Amount : A formerly over-due loan account (credit card, car loan) whose final balance was settled for less than the full amount owed. Potential lenders who find these items on a credit report consider this to be a negative factor. Paid in Full : The trade line/loan account has a $0 balance. Payment Status: How the trade line or loan account is being paid back on time, or late. REPO: Repossession (voluntary you turn in the vehicle, or involuntary the lender or repossession agent acquires it). A repo trade line remains on a consumer s credit history for up to 7 years. Reported Since: The original date the account started reporting to the credit bureau/credit reporting agency. Revolving: An open-end loan (revolving) plan such as a credit card or a home equity line of credit. The consumer draws down on a line amount, and makes open-end (noninstallment) payments on the amount outstanding, plus finance charges. Revolving loans have no end date. Satisfied: A court ordered payment on a debt which has been paid off by the consumer in an amount that is deemed to be acceptable. Security Alert: Consumers, who believe their identities may have been stolen due to a recent scam or file-breach, may initiate a security or fraud alert with the major credit reporting agencies. This notation will appear on their file. Status: The repayment condition of the account. Term Duration: The total number of payments on an installment loan. Utilization Rate: The percentage of a credit available to a consumer that he or she has used. Utilization rate is an important factor in a person s credit score. An ideal utilization rate for most consumers is generally 10% or lower. Vacated: A civil court judgment that is voided. Wage Garnishment: A court action directing the consumer debtor s employer to set aside a percentage of his or her wages to satisfy a judgment on a delinquent debt. Writ of Replevin: Court ordered repossession of an item offered by the borrower as security on a loan. It is thrifty to prepare today for the wants of tomorrow -Aesop Scheduled Payment Amount: The minimum amount last requested for payment. 14

19 15

20 Publications Be sure to check out other free booklets from the Bureau of Consumer Credit Protection: Downeaster Common Sense Guide: Debt Collection If you are past due on your credit card, mortgage loan, auto loan or student loan, this is the FREE booklet for you! Learn about your rights in a consumer debt collection action, and how to deal with collectors. This booklet also provides guidance in spotting prevalent debt collection scams and contains ample cease contact and debt validation letters. Downeaster Common Sense Guide: Automobile Buying and Financing From calculating how much vehicle you can afford, to vehicle research, shopping for the best APR and deciding on the best loan term for your needs, this booklet is a comprehensive guide to purchasing and financing a vehicle. Downeaster Common Sense Guide: Gone Phishing Identifying and Avoiding Consumer Scams This guide is all about helping consumers defend themselves against being scammed. It details tactics and hooks used by scammers, offers advice to consumers so they can protect themselves, and explains how to report the scams to authorities. Downeaster Common Sense Guide: Credit Reports and Credit Scores Learn the basics of credit, gain insight into how credit reporting and scoring work, and discover the impact your credit has on your ability to borrow with this publication from the Bureau of Consumer Credit Protection. Downeaster Common Sense Guide Finding, Buying and Keeping Your Maine Home This guide is a resource for first time homebuyers, and provides an overview of the mortgage lending process, types of mortgage lenders and loans, and other related topics. Downeaster Common Sense Guide to Student Loans A comprehensive guide 16

21 for the prospective college student on the world of educational loans. This book covers loan types, the FAFSA process, how to apply for scholarships and grants, and the rights of a student debtor in the repayment/collection process. Downeaster Guide to Elder Financial Protection This booklet arms seniors with information to protect their finances in the 21 st Century. It includes tips on spotting and stopping elder financial abuse and exploitation, in addition to information on registering for the Do-No-Call List, the Do-Not-Mail List and the credit card (mailing) Opt-Out List. The Downeaster Guide to Elder Financial Protection also features a resource page containing contact information for must know consumer protection agencies in both Maine State and federal government. These guides are free to Maine residents. Out-of-state orders are $6.00 each, or at a volume discount of $4.00/copy on orders of 50 or more (shipping included). To order, call (in-state) or (outside of Maine). 17

22 Consumer Protection Resources Maine Bureau of Consumer Credit Protection TTY Maine Relay 711 Maine Bureau of Insurance Maine Bureau of Financial Institutions Maine Office of Aging and Disability Services Maine Office of the Attorney General (Consumer Hotline) Maine Office of Professional and Occupational Regulation Maine Office of Securities Maine Public Utilities Commission (Consumer Assistance Division) Maine Real Estate Commission Consumer Financial Protection Bureau (CFPB) (Federal) TTY Maine Relay TTY Maine Relay TTY Maine Relay TTY TTY Maine Relay TTY Maine Relay TTY TTY Maine Relay TTY Federal Reserve Consumer Hotline Federal Trade Commission Consumer Response Center Federal Trade Commission ID Theft Hotline (after dialing, press 0 to reach a live operator) Internet Crime Complaint Center (IC 3 ) National Credit Union Administration (NCUA) U.S. Postal Inspection Office (Ask for the Portland, Maine Field Office)

23 NOTES This book is not intended to be a complete discussion of all statutes applicable to consumer credit. If you require further information, consider contacting our agency or an attorney for additional help. 3rd Printing 2016 Copyright 2015 The State of Maine Bureau of Consumer Credit Protection 19

24 20 Bureau of Consumer Credit Protection 35 State House Station Augusta, ME

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

How To Check Your Credit Report For Not Credit History

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit reports and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit reports and the three little digits that make up your credit score probably influence your life in many ways.

BalanceTrack. The World of Credit Reports

BalanceTrack The World of Credit Reports Credit reports and credit scores influence our lives in many ways. Your history of credit management can affect the cost of the credit you receive, your ability

BalanceTrack The World of Credit Reports Credit reports and credit scores influence our lives in many ways. Your history of credit management can affect the cost of the credit you receive, your ability

Understanding Your Credit Report

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

All About Credit Reports from A to Z

All About Credit Reports from A to Z Adverse Action Notice A notice that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should

All About Credit Reports from A to Z Adverse Action Notice A notice that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should

Building a CREDIT REPORT. Federal Trade Commission consumer.ftc.gov

Building a CREDIT REPORT Federal Trade Commission consumer.ftc.gov Shopping for a car? Applying for a job? Looking for a home? Getting your financial house in order? It s time to check your credit report.

Building a CREDIT REPORT Federal Trade Commission consumer.ftc.gov Shopping for a car? Applying for a job? Looking for a home? Getting your financial house in order? It s time to check your credit report.

Credit Scores. www.howtogainwealth.com. Copyright 2009 How to Gain Wealth. All rights reserved.

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Your Credit Report. Trade lines. The bulk of a credit report is dedicated to your history of handling credit. It includes:

Your Credit Report The three major credit bureaus in the United States are Experian, TransUnion, and Equifax. These companies acquire data from banks, credit unions, mortgage lenders, and retail establishments.

Your Credit Report The three major credit bureaus in the United States are Experian, TransUnion, and Equifax. These companies acquire data from banks, credit unions, mortgage lenders, and retail establishments.

Reviewing C Your Credit Report

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

How to Use Credit. Latino Community Credit Union & Latino Community Development Center

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

INTRODUCTION. Identity Theft Crime Victim Assistance Kit

Identity Theft Crime Victim Assistance Kit INTRODUCTION In the course of a busy day, you may write a check at the grocery store, charge tickets to a ball game, rent a car, mail your tax returns, change

Identity Theft Crime Victim Assistance Kit INTRODUCTION In the course of a busy day, you may write a check at the grocery store, charge tickets to a ball game, rent a car, mail your tax returns, change

Improving a Credit Profile

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Improving a Credit Profile Steps to improving a credit profile STEP 1. Order your credit Report STEP 2. Evaluate & develop a plan STEP 3. Is the personal information accurate? STEP 4. Are the tradelines

Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better

300 to 850 the higher, the better") What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor

By Bill Taylor") UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

UNDERSTANDING Your CREDIT REPORT & SCORES

UNDERSTANDING Your CREDIT REPORT & SCORES www.credit.org Promoting Financial Literacy About Springboard Springboard is a non-profit organization founded in 1974. We offer personal financial education and

UNDERSTANDING Your CREDIT REPORT & SCORES www.credit.org Promoting Financial Literacy About Springboard Springboard is a non-profit organization founded in 1974. We offer personal financial education and

TABLE OF CONTENTS. CHAPTER 1: Credit Report.. Page 1. CHAPTER 2: Credit Score...Page 3. CHAPTER 3: Credit Reporting Agencies.

TABLE OF CONTENTS CHAPTER 1: Credit Report.. Page 1 CHAPTER 2: Credit Score.....Page 3 CHAPTER 3: Credit Reporting Agencies.Page 6 CHAPTER 4: How to get a FREE Credit Report Page 8 CHAPTER 5: The 4 th

TABLE OF CONTENTS CHAPTER 1: Credit Report.. Page 1 CHAPTER 2: Credit Score.....Page 3 CHAPTER 3: Credit Reporting Agencies.Page 6 CHAPTER 4: How to get a FREE Credit Report Page 8 CHAPTER 5: The 4 th

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

What We Need to Know About. Credit Management & Credit Repair for Entrepreneurs What is Credit? When someone lends you money, and you pay them back with interest, they have extended you credit. Credit

Facts On Credit Bureaus

Facts On Credit Bureaus The following information relates to the understanding and use of a credit score. Listed are details regarding the determination of a credit score, how you can find out what your

Facts On Credit Bureaus The following information relates to the understanding and use of a credit score. Listed are details regarding the determination of a credit score, how you can find out what your

Understanding, managing, and rebuilding your credit

Understanding, managing, and rebuilding your credit Objective Bank of America is committed to providing information that will help you understand the effect credit can have on lending, and what you can

Understanding, managing, and rebuilding your credit Objective Bank of America is committed to providing information that will help you understand the effect credit can have on lending, and what you can

Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT

CREDIT What You Should Know About... Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT YourMoneyCounts Understanding what your credit history is what s in it, what s not in it

CREDIT What You Should Know About... Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT YourMoneyCounts Understanding what your credit history is what s in it, what s not in it

The company does not tell you your rights and what you can do for yourself for free.

Credit repair Save your time and money by knowing the signs of a scam You see credit repair service offerings in newspapers, mail flyers, on TV or the Internet, and hear them on the radio or phone calls.

Credit repair Save your time and money by knowing the signs of a scam You see credit repair service offerings in newspapers, mail flyers, on TV or the Internet, and hear them on the radio or phone calls.

Welcome. 1. Agenda. 2. Ground Rules. 3. Introductions. To Your Credit 2

To Your Credit Welcome 1. Agenda 2. Ground Rules 3. Introductions To Your Credit 2 Objectives Define credit Explain why credit is important Describe the purpose of a credit report and how it is used Order

To Your Credit Welcome 1. Agenda 2. Ground Rules 3. Introductions To Your Credit 2 Objectives Define credit Explain why credit is important Describe the purpose of a credit report and how it is used Order

How To Get A Credit Report From A Credit Card To A Credit Rating Card

Credit Report Info Packet Information in this Packet What Is a Credit Report?.....................3 What Is a Credit Score?..................... 4 Who Can See Your Credit Report?.............. 5 Ordering

Credit Report Info Packet Information in this Packet What Is a Credit Report?.....................3 What Is a Credit Score?..................... 4 Who Can See Your Credit Report?.............. 5 Ordering

Familiarize yourself with laws that authorize and regulate vehicle dealership financing and leasing.

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

12 common questions. About consumer credit and direct marketing

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

12 common questions About consumer credit and direct marketing Most of us don t think about credit until a specific event sparks our interest. Maybe we want to buy a car or home. Or perhaps we receive

FTC Facts. For Consumers Federal Trade Commission. Maybe you never opened that account, but. Identity Crisis... What to Do If Your Identity is Stolen

FTC Facts For Consumers Federal Trade Commission For The Consumer August 2005 Identity Crisis... What to Do If Your Identity is Stolen Maybe you never opened that account, but someone else did...someone

FTC Facts For Consumers Federal Trade Commission For The Consumer August 2005 Identity Crisis... What to Do If Your Identity is Stolen Maybe you never opened that account, but someone else did...someone

The West Virginia State Treasurer s Office. A free publication provided by

YOUR CREDIT SCORE A free publication provided by The West Virginia State Treasurer s Office Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue

YOUR CREDIT SCORE A free publication provided by The West Virginia State Treasurer s Office Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue

Credit Reports. published by AAA Fair Credit Foundation

Credit Reports published by AAA Fair Credit Foundation Credit Reports 1. What is a Credit Report?..........................................................2 2. What Your Credit Report Reveals About You...................................4

Credit Reports published by AAA Fair Credit Foundation Credit Reports 1. What is a Credit Report?..........................................................2 2. What Your Credit Report Reveals About You...................................4

Consumer Guides to Credit Reporting and Credit Scores (Appropriate for General Distribution)

") Appendix L Consumer Guides to Credit Reporting and Credit Scores (Appropriate for General Distribution) This appendix contains two consumer guides on credit reports and credit scores. The first guide summarizes

Appendix L Consumer Guides to Credit Reporting and Credit Scores (Appropriate for General Distribution) This appendix contains two consumer guides on credit reports and credit scores. The first guide summarizes

For Consumers Federal Trade Commission. Need Credit or Insurance? Your Credit Score Helps Determine What You ll Pay

FTC Facts For Consumers Federal Trade Commission For The Consumer July 2007 www.ftc.gov 1-877-ftc-help Need Credit or Insurance? Your Credit Score Helps Determine What You ll Pay Ever wonder how a lender

FTC Facts For Consumers Federal Trade Commission For The Consumer July 2007 www.ftc.gov 1-877-ftc-help Need Credit or Insurance? Your Credit Score Helps Determine What You ll Pay Ever wonder how a lender

Understanding Credit. The Three C s of Credit. What is a Credit Bureau?

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Solving The Mystery of Credit Reports

Solving The Mystery of Credit Reports 800.456.4828 www.tinkerfcu.org Credit reports and credit scores are increasingly important to our lives. They affect the cost of credit we receive, where we live,

Solving The Mystery of Credit Reports 800.456.4828 www.tinkerfcu.org Credit reports and credit scores are increasingly important to our lives. They affect the cost of credit we receive, where we live,

ALERTS NOTIFICATION USER GUIDE

Page 1 of 10 ABOUT EQUIFAX ALERTS NOTIFICATION USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust.

Page 1 of 10 ABOUT EQUIFAX ALERTS NOTIFICATION USER GUIDE Equifax Canada Inc. Box 190 Jean Talon Station Montreal, Quebec H1S 2Z2 Equifax empowers businesses and consumers with information they can trust.

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D S T A T E B A R O F T E X A S I D E N T I T Y T H E F T G U I D E

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D S T A T E B A R O F T E X A S I D E N T I T Y T H E F T G U I D E A I D E N T I T Y T H E F T G U I D E Prepared and distributed as a Public

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D S T A T E B A R O F T E X A S I D E N T I T Y T H E F T G U I D E A I D E N T I T Y T H E F T G U I D E Prepared and distributed as a Public

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

Why Credit is Important

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Credit Repair: Self-Help May Be Best

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 www.ftc.gov 1-877-ftc-help Credit Repair: Self-Help May Be Best You see the advertisements in newspapers, on TV, and on the

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 www.ftc.gov 1-877-ftc-help Credit Repair: Self-Help May Be Best You see the advertisements in newspapers, on TV, and on the

Chapter 06. What is Consumer Credit? Chapter 6 Learning Objectives. Introduction to Consumer Credit

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Disputing Errors on Credit Reports

Disputing Errors on Credit Reports Federal Trade Commission consumer.ftc.gov Your credit report contains information about where you live, how you pay your bills, and whether you ve been sued or arrested,

Disputing Errors on Credit Reports Federal Trade Commission consumer.ftc.gov Your credit report contains information about where you live, how you pay your bills, and whether you ve been sued or arrested,

Credit arrangements can be formal or informal. The three most common types of credit used by consumers are described below.

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

1-888-842-6328 For toll-free numbers when overseas, visit Collect internationally 1-703-255-8837 TDD for hearing impaired 1-888-869-5863 Credit Wise Credit: a Useful Tool Most of us use consumer credit

CREDIT SCORE USER GUIDE

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Page 1 of 11 ABOUT EQUIFAX Equifax empowers businesses and consumers with information they can trust. A global leader in information solutions, we leverage one of the largest sources of consumer and commercial

Credit Repair How to Help Yourself

Credit Repair How to Help Yourself Federal Trade Commission consumer.ftc.gov You see the ads in newspapers, on TV, and online. You hear them on the radio. You get fliers in the mail, email messages, and

Credit Repair How to Help Yourself Federal Trade Commission consumer.ftc.gov You see the ads in newspapers, on TV, and online. You hear them on the radio. You get fliers in the mail, email messages, and

For Consumers Federal Trade Commission. Credit Repair: Self-Help May Be Best. n companies that want you to pay for credit repair

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 www.ftc.gov 1-877-ftc-help Credit Repair: Self-Help May Be Best You see the advertisements in newspapers, on TV, and on the

FTC Facts For Consumers Federal Trade Commission For The Consumer December 2005 www.ftc.gov 1-877-ftc-help Credit Repair: Self-Help May Be Best You see the advertisements in newspapers, on TV, and on the

Understanding Your FICO Score

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Understanding Credit Cards

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Understanding Credit Cards INTRODUCTION This brochure can help you understand how credit cards work, become familiar with common terms offered with a credit card, and avoid the dangers of using credit

Personal Digital Security

The following is an excerpt from: Personal Digital Security Protecting Yourself from Online Crime 2016 Revision by Michael Bazzell More information can be found at ComputerCrimeInfo.com Over the past ten

The following is an excerpt from: Personal Digital Security Protecting Yourself from Online Crime 2016 Revision by Michael Bazzell More information can be found at ComputerCrimeInfo.com Over the past ten

Citi Identity Theft Solutions

Identity Theft what you need to know Citi Identity Theft Solutions At Citi, we want to keep you informed about all of the issues that can affect your financial life. We re bringing you helpful information

Identity Theft what you need to know Citi Identity Theft Solutions At Citi, we want to keep you informed about all of the issues that can affect your financial life. We re bringing you helpful information

Credit ~ The Basics Participant s Guide

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

1 Credit ~ The Basics Participant s Guide Table of Contents Welcome Pre-Test What is Credit & Why is it Important? Types of Loans The Cost of Credit The Four C s of Credit Credit Reports Credit Scores

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

How To Know Your Credit Risk

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Use and Misuse of Credit. Chapter 6. Advantages of Credit. What is Consumer Credit?

Chapter 6 Use and Misuse of Credit Introduction to Consumer Credit Before you use credit for a major purchase, ask yourself some questions. Do I have the cash for the down payment? Do I want to use my

Chapter 6 Use and Misuse of Credit Introduction to Consumer Credit Before you use credit for a major purchase, ask yourself some questions. Do I have the cash for the down payment? Do I want to use my

Credit Repair ebook. You don t have to pay money to repair your credit Our ebook will teach you: MagnifyMoney

MagnifyMoney Credit Repair ebook You don t have to pay money to repair your credit Our ebook will teach you: How to get your credit report, for free How to dispute incorrect information for free How to

MagnifyMoney Credit Repair ebook You don t have to pay money to repair your credit Our ebook will teach you: How to get your credit report, for free How to dispute incorrect information for free How to

A summary of your financial reliability

A summary of your financial reliability Used by banks and other financial institutions, landlords, utility companies and insurance companies 3 major credit bureaus: Transunion, Equifax, Experian 1. Identifying

A summary of your financial reliability Used by banks and other financial institutions, landlords, utility companies and insurance companies 3 major credit bureaus: Transunion, Equifax, Experian 1. Identifying

Free Credit Reports CREDIT

Free Credit Reports CREDIT Federal Trade Commission ftc.gov The Fair Credit Reporting Act (FCRA) requires each of the nationwide credit reporting companies Equifax, Experian, and TransUnion to provide

Free Credit Reports CREDIT Federal Trade Commission ftc.gov The Fair Credit Reporting Act (FCRA) requires each of the nationwide credit reporting companies Equifax, Experian, and TransUnion to provide

SECURITY FREEZE INFORMATION FOR KENTUCKY RESIDENTS

SECURITY FREEZE INFORMATION FOR KENTUCKY RESIDENTS If you live in Kentucky, you have the right as of July 12, 2006, to put a Asecurity freeze@ on your credit report with each credit reporting agency. A

SECURITY FREEZE INFORMATION FOR KENTUCKY RESIDENTS If you live in Kentucky, you have the right as of July 12, 2006, to put a Asecurity freeze@ on your credit report with each credit reporting agency. A

You see the advertisements in newspapers, on

October 2008 Credit Repair: How To Help Yourself You see the advertisements in newspapers, on TV, and on the Internet. You hear them on the radio. You get fliers in the mail, and maybe even calls offering

October 2008 Credit Repair: How To Help Yourself You see the advertisements in newspapers, on TV, and on the Internet. You hear them on the radio. You get fliers in the mail, and maybe even calls offering

How to Dispute Credit Report Errors Y

September 2008 How to Dispute Credit Report Errors Y our credit report contains information about where you live, how you pay your bills, and whether you ve been sued or arrested, or have filed for bankruptcy.

September 2008 How to Dispute Credit Report Errors Y our credit report contains information about where you live, how you pay your bills, and whether you ve been sued or arrested, or have filed for bankruptcy.

The AFI Resource Center is pleased to provide this presentation about credit reports.

The AFI Resource Center is pleased to provide this presentation about credit reports. This is one of several presentations developed for AFI grantees on a variety of financial education topics, including

The AFI Resource Center is pleased to provide this presentation about credit reports. This is one of several presentations developed for AFI grantees on a variety of financial education topics, including

CITY OF ROCHESTER, MINNESOTA POLICE DEPARTMENT

CITY OF ROCHESTER, MINNESOTA POLICE DEPARTMENT 101 4 TH Street Southeast Rochester, Minnesota 55904-3761 507-328-6800 Fax 507-328-6975 To: From: Subject: Identity Theft and Internet Crime Victims Rochester

CITY OF ROCHESTER, MINNESOTA POLICE DEPARTMENT 101 4 TH Street Southeast Rochester, Minnesota 55904-3761 507-328-6800 Fax 507-328-6975 To: From: Subject: Identity Theft and Internet Crime Victims Rochester

How to Dispute Credit Report Errors

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 www.ftc.gov 1-877-ftc-help How to Dispute Credit Report Errors Y our credit report contains information about where you live,

FTC Facts For Consumers Federal Trade Commission For The Consumer May 2006 www.ftc.gov 1-877-ftc-help How to Dispute Credit Report Errors Y our credit report contains information about where you live,

Credit Reports and How to Dispute Credit Report Errors

Credit Reports and How to Dispute Credit Report Errors The County Clerk's Office preserves and makes available to the public, including credit reporting agencies, all records affecting the title to real

Credit Reports and How to Dispute Credit Report Errors The County Clerk's Office preserves and makes available to the public, including credit reporting agencies, all records affecting the title to real

Credit Histories & Credit Scores

Credit Histories & Credit Scores Credit Histories - Definition A continuing record of a borrower s debt commitments and how well they have been honored. (Similar to a transcript) Credit Score - Definition

Credit Histories & Credit Scores Credit Histories - Definition A continuing record of a borrower s debt commitments and how well they have been honored. (Similar to a transcript) Credit Score - Definition

Your Credit Report What It Says about You

Your Credit Report Your Credit Report What It Says about You Most people finance their homes with mortgages and pay for their cars with loans. Young people often obtain loans to pay for college. And, of

Your Credit Report Your Credit Report What It Says about You Most people finance their homes with mortgages and pay for their cars with loans. Young people often obtain loans to pay for college. And, of

FTC Facts. For Consumers Federal Trade Commission. The Fair Credit Reporting Act (FCRA) requires. Your Access to Free Credit Reports

requires. Your Access to Free Credit Reports") FTC Facts For Consumers Federal Trade Commission For The Consumer March 2008 Your Access to Free Credit Reports ftc.gov 1-877-ftc-help The Fair Credit Reporting Act (FCRA) requires each of the nationwide

FTC Facts For Consumers Federal Trade Commission For The Consumer March 2008 Your Access to Free Credit Reports ftc.gov 1-877-ftc-help The Fair Credit Reporting Act (FCRA) requires each of the nationwide

Office of Privacy Protection Safeguarding Information for Your Future

W I S C O N S I N Office of Privacy Protection Safeguarding Information for Your Future Credit report security freeze Wisconsin consumers have the right to place a security freeze on their credit reports.

W I S C O N S I N Office of Privacy Protection Safeguarding Information for Your Future Credit report security freeze Wisconsin consumers have the right to place a security freeze on their credit reports.

IDENTITY THEFT VICTIMS: IMMEDIATE STEPS

IDENTITY THEFT VICTIMS: IMMEDIATE STEPS If you are a victim of identity theft, take the following four steps as soon as possible, and keep a record with the details of your conversations and copies of

IDENTITY THEFT VICTIMS: IMMEDIATE STEPS If you are a victim of identity theft, take the following four steps as soon as possible, and keep a record with the details of your conversations and copies of

Earning Extra Credit. Understanding what it takes to maintain and manage good credit now and for your future

Credit 101 Why Credit is Important 3 Your Credit Score 5 FICO Scoring - From Good to Bad 7 Credit Bureaus 8 Credit-Worthy vs. Credit-Ready 9 Are you Drowning in Debt? 10 2 Why Credit is Important College

Credit 101 Why Credit is Important 3 Your Credit Score 5 FICO Scoring - From Good to Bad 7 Credit Bureaus 8 Credit-Worthy vs. Credit-Ready 9 Are you Drowning in Debt? 10 2 Why Credit is Important College

Credit Report The single most important document for protection against identity theft.

Understanding your Credit Report The single most important document for protection against identity theft. What to do if you spot errors A recent study shows that 79 percent of credit reports contained

Understanding your Credit Report The single most important document for protection against identity theft. What to do if you spot errors A recent study shows that 79 percent of credit reports contained

G&I Homes is a New York State Registered Mortgage Broker: NMLS# 20923

G&I Homes is a New York State Registered Mortgage Broker: NMLS# 20923 As a New York State registered mortgage broker, we have access to many lenders and many varied programs. In our capacity as a registered

G&I Homes is a New York State Registered Mortgage Broker: NMLS# 20923 As a New York State registered mortgage broker, we have access to many lenders and many varied programs. In our capacity as a registered

CREDIT BASICS PARTICIPANT S GUIDE

BASICS PARTICIPANT S GUIDE Developed for Justine Peterson By Foundation - Office of Financial Education March 2009 Module 1 ABC'S of Credit Activity 1: The Five C s of Credit Activity 2: When to Use Credit

BASICS PARTICIPANT S GUIDE Developed for Justine Peterson By Foundation - Office of Financial Education March 2009 Module 1 ABC'S of Credit Activity 1: The Five C s of Credit Activity 2: When to Use Credit

I know what is identity theft but how do I know if mine has been stolen?

What is identity theft? You might hear stories on the news about stolen identities, but what is identity theft? When someone uses the personal information that identifies you, like your name, credit card

What is identity theft? You might hear stories on the news about stolen identities, but what is identity theft? When someone uses the personal information that identifies you, like your name, credit card

CREDIT REPORTS WHAT EVERY CONSUMER SHOULD KNOW ABOUT MORTGAGE EQUITY P A R T N E R S

F WHAT EVERY CONSUMER SHOULD KNOW ABOUT CREDIT REPORTS MORTGAGE EQUITY P A R T N E R S Your Leaders in Lending B The information contained herein is for informational purposes only. The algorithymes and

F WHAT EVERY CONSUMER SHOULD KNOW ABOUT CREDIT REPORTS MORTGAGE EQUITY P A R T N E R S Your Leaders in Lending B The information contained herein is for informational purposes only. The algorithymes and

Identity Theft Victim s Packet

Identity Theft Victim s Packet In this packet: Information and Instructions Section 1, # of pages 6 Fair and Accurate Credit Transactions Act of 2003 Section 2, # of pages 3 ID Theft Affidavit Section

Identity Theft Victim s Packet In this packet: Information and Instructions Section 1, # of pages 6 Fair and Accurate Credit Transactions Act of 2003 Section 2, # of pages 3 ID Theft Affidavit Section

Improve Your Credit Put Bad Credit Behind You

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Dear Concerned Consumer,

Dear Concerned Consumer, Identity theft is a growing problem of the Information Age. You have already taken the first important step in combating the problem by contacting HomeStar Bank & Financial Services.

Dear Concerned Consumer, Identity theft is a growing problem of the Information Age. You have already taken the first important step in combating the problem by contacting HomeStar Bank & Financial Services.

Most frequently asked questions and the answers about free credit reports:

Free credit reports The Federal Fair Credit Reporting Act (FCRA) is enforced by the Federal Trade Commission (FTC) and requires each nationwide consumer reporting company to provide you with a free copy

Free credit reports The Federal Fair Credit Reporting Act (FCRA) is enforced by the Federal Trade Commission (FTC) and requires each nationwide consumer reporting company to provide you with a free copy

The Massachusetts Attorney General s. Guide to Consumer Credit

The Massachusetts Attorney General s Guide to Consumer Credit June 2014 Table of Contents A Note from the Attorney General 3 Truth In Lending 4 Billing Rights 7 Costs of Credit 9 Fair Credit Reporting

The Massachusetts Attorney General s Guide to Consumer Credit June 2014 Table of Contents A Note from the Attorney General 3 Truth In Lending 4 Billing Rights 7 Costs of Credit 9 Fair Credit Reporting

IDENTITY THEFT RESOURCE KIT

IDENTITY THEFT RESOURCE KIT TABLE OF CONTENTS Introduction 2 What To Do Now 3 Key Agencies to Contact 3 Other Important Contacts 4 Action Taken Form 6 Sample Letters 7 How Identity Theft Can Occur 9 What

IDENTITY THEFT RESOURCE KIT TABLE OF CONTENTS Introduction 2 What To Do Now 3 Key Agencies to Contact 3 Other Important Contacts 4 Action Taken Form 6 Sample Letters 7 How Identity Theft Can Occur 9 What

SCAM JAM 2011. ID Theft. Presented by: Lori Farris Office of the Attorney General Office of Consumer Protection

SCAM JAM 2011 ID Theft Presented by: Lori Farris Office of the Attorney General Office of Consumer Protection ID Theft The NAME GAME. Don t Get Played! Identity Theft: Learn the basics- What it is. How

SCAM JAM 2011 ID Theft Presented by: Lori Farris Office of the Attorney General Office of Consumer Protection ID Theft The NAME GAME. Don t Get Played! Identity Theft: Learn the basics- What it is. How

Understanding and managing your credit

Understanding and managing your credit Overview Understanding how credit works and how it affects your chances of getting approved for a loan is important. In this presentation, you ll learn helpful ways

Understanding and managing your credit Overview Understanding how credit works and how it affects your chances of getting approved for a loan is important. In this presentation, you ll learn helpful ways

Your Credit Repair Solution

Your Credit Repair Solution Introduction Your Credit Report Solution will help you understand that there is help available for fixing your credit. Even though you might feel as though you are alone and

Your Credit Repair Solution Introduction Your Credit Report Solution will help you understand that there is help available for fixing your credit. Even though you might feel as though you are alone and

Lake County Sheriff s Office Identity Theft/Fraud Packet

Gary S. Borders, Sheriff Lake County Sheriff s Office Identity Theft/Fraud Packet Information and Instructions The Information and Instructions portion of this packet is for you to keep and contains information