Understanding Commissions Motivated Advice: Evidence from Indian Life Insurance

|

|

|

- Sabina Liliana Martin

- 8 years ago

- Views:

Transcription

1 Understanding Commissions Motivated Advice: Evidence from Indian Life Insurance Santosh Anagol (Wharton), Shawn Cole (Harvard Business School), Shayak Sarkar (Harvard) Wharton, February, 2012

, Shayak Sarkar (Harvard) Wharton,")

2 Introduction Many financial products difficult to value, particularly for those with limited financial experience (mortgages, life insurance) Little learning for long-horizon products May limit usefulness of brokers to build reputations for providing the right products Research Agenda: How do consumers make decisions about these complicated financial products? Research Questions Today: What is the quality of advice that commissions motivated agents provide? Under what conditions does advice improve? Many other inputs into consumers decisions: Press? Friends? Regulations? Government campaigns?

3 Motivation: Why Life Insurance in India? Why India? Increasing incomes in China, India other fast developing countries will greatly increase capacity to invest in formal financial products How will these consumers make informed decisions? What role should government play? Important question in the U.S. as well (creation of Consumer Financial Protection Bureau) Why Life Insurance? 20 % of Indian household financial savings in life insurance products Easiest product to identify potentially bad decisions Approximately 2.4 million life insurance agents in India (approx 434,000 in the US)

Why Life Insurance?")

4 Focus on Term vs. Whole Most popular products Easy for us to compare/evaluate Term : pay P T for N years, receive payout C T at death during that period, or nothing if survive N years. Whole: pay P w per year for N years, receive P w N + B at min (year of death, max(40 years after purchase, age 80)) Surrender value: 30% of premiums paid if paid > 3 years How are bonuses (B) determined? Discretion of life insurance company A percentage (typically 3%-5%) of sum assured (P w N) Importantly, not compounded Whole type products have estimated 60-80% market share

) Surrender value: 30% of")

5 Replicating Portfolio Consider Rs. 500,000 (ca. $10,000) coverage for 34 year-old male Whole life policy costs Rs. 13,574 per year, paying 3% bonus Term policy for equivalent coverage (Rs. 500,000) and save remainder 2,507 per year + 11,067 savings deposit (earning 8%) for 25 years (until 2035) Savings contribution 13,574 from 2035 until 2056 Clear violation of law of one price If you die before 2056: almost surely better off with term + savings (savings are liquid) If you survive until 2056 Whole redemption value: Rs. 1,205,000 Savings balance: Rs. 5,563,378 Note: no risk of future premium increases for term product (Cochrane (1995)) Rajagopalan (2010) has similar findings

If you survive until 2056 Whole redemption value:")

6 Why Would Anyone Choose Whole? Agent receives commission of 35% on whole, 5% on term Paper presents model where a dominated product with high commissions can exist in competitive equilibrium Buyer cannot calculate effective cost Term is throwing money away if you survive until the end of the policy, it s worth nothing People don t appreciate importance of compounding (Zinman and Stango (2009)) Whole policies pay 3%-5% bonus per year not compounded! Commitment to save Why does commitment to save have to bundled with insurance? Public provident fund is a commitment savings product paying compound better returns

) Whole policies pay 3%-5% bonus per year not compounded!")

7 Audit Study Hire 10 auditors, making a total of 1,026 visits to insurance agents over 12 months Field experiment conducted in two major cities in India Audit process developed by a former life insurance salesman from major bank Agents found on publicly available yellow pages type websites Week-long training, practice audits Each auditor has personalized (true) script ( I am a married man with two kids... ) Certain features disguised My salary? Let s say I earn Rs. 10,000 per month

script ( I am a married man with two kids... ) Certain features disguised My salary? Let s say I earn Rs.")

8 Channels of Life Insurance Sales Distribution Channel (1) Individual Agents 79.6 Banks 10.6 Other Corporate Agents 4.30 Brokers 1.38 Direct Selling 4.13 Source: IRDA Annual Report,

9 Pilot Script Introduce self, express need for life insurance Not looking for investment product Seeking maximum risk cover at minimum cost If need to save, prefer to save in a bank What policy do you recommend?

10 Pilot Script: Proportion of Term Recommendations Recommendation Risk Coverage Script (1) Only Term Policy Recommended.09 Any Term Policy Recommended.16 Only Whole Type Policies Recommended.31 Any Whole Type Policy Recommended.64 Any Other Policy Type.18 Observations 60

11 Agents Talk Down Term Insurance You want term: Are you planning on killing yourself? Term is throwing money away Term is not for: Women Middle class Term is only for: businessmen government employees Offered endowment policy, calling it a term policy Only one instance of explicit debiasing Don t buy whole, it s a rip-off

12 Quality of Advice: Multiple Recommendations Most term recommendations come as a part of multiple recommendations (a package)

13 Quality of Advice: Suitability and Catering Do agents provide advice based on client s actual need, or client s beliefs about what is the right product? Important question in context where clients are unlikely to understand differences in products Vary need: Whole: I want to save and invest money for the future, and I also want to make sure my wife and children will be taken care of if I die. I do not have the discipline to save on my own Term: I am worried that if I die early, my wife and kids will not be able to live comfortably or meet our financial obligations. I want to cover that risk at an affordable cost. Vary beliefs: I have heard that whole insurance is a really good product. I think it may be suitable for me. Maybe we can explore that further? I have heard that term insurance is a really good product. I think it may be suitable for me. Maybe we can explore that further?

14 Quality of Advice: Responding to Needs & Beliefs Overall low rate of recommending term insurance - even when auditor says they want risk coverage and have heard term is a good product But needing risk coverage does cause about 12% higher probability of receiving term recommendation Even when customer initially believes whole may be better for them At least some agents know that term insurance is better for risk coverage

15 Catering vs. Quality Advice: Term Insurance Dependent Variable Any Term Only Term (1) (2) Belief Term 0.10*** 0.02* [0.03] [0.02] Need Term 0.12*** [0.04] [0.01] Belief Term * Need Term * [.059] [.031] Government Underwriter -0.12*** -.01 [.041] [.02] Constant [0.05] [0.01] Auditor FE YES YES Observations Adjusted R-squared Mean of Dep Var Agents do cater advice to both customer preferences and need for risk coverage Not just whole recommending machines But catering mainly by adding on a term policy on top of a whole policy Following the path of least resistance Government underwriters less likely to mention term plans overall

![01] Auditor FE YES YES Observations 511 511 Adjusted R-squared 0.10 0.034 Mean of Dep Var 0.13 0.](/docs-images/54/10338382/images/page_15.jpg "03 Agents do cater advice to both customer preferences and need for risk coverage Not just whole recommending machines But catering mainly by adding on a term policy on")

16 Wide Range of Risk Coverages Recommended Belief & Need = Term Risk Cover (U.S.D) Premium (U.S.D) Whole Life Type Policies 12, Term Type Policies 44, Only 10% of auditors get a term recommendation But the amount of risk coverage they get recommended is approx 4 times larger Possible theory: agents cater to premium amount that can be paid

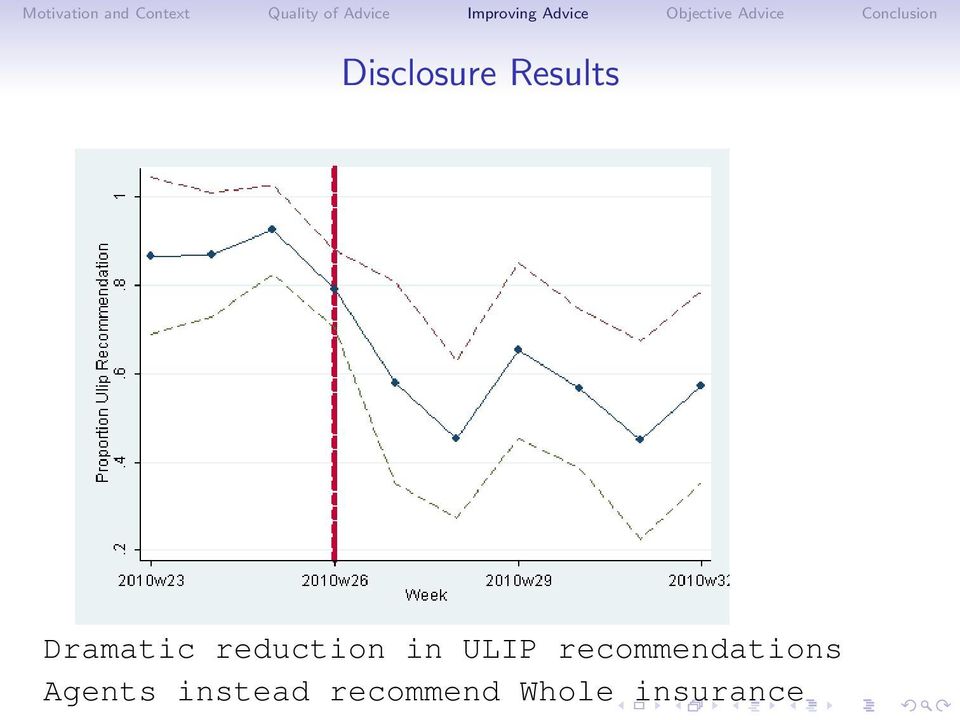

17 Improving Advice: Natural Experiment on Effect of Disclosure Natural experiment on ULIP disclosures Prior to July 1, 2010, agents required to inform buyers about total ULIP costs/charges As of July 1, 2010, agents are required to provide separate breakdown of commission costs Allows us to isolate disclosure of agency problems Measure agent reaction

18 Field Experiment Overlaid on Natural Experiment Overlay with field experiment Agent expresses knowledge of agency problems Can you give me more information about the commission charges I ll be paying? Agent does not express knowledge of agency problems [No statement]

19 Results Table: 8-Effect of Disclosure on Product Recommendations Dep Var = Ulip Recommended (1) (2) Post Disclosure Regulation -0.22*** -0.21*** [0.05] [0.08] Disclosure Knowledge [0.05] [0.07] Agent Home [0.11] [0.11] Auditor Home [0.17] [0.17] Agent Office [0.10] [0.10] Auditor Office [0.20] [0.20] LIC -0.44*** -0.44*** [0.05] [0.05] Post Disclosure Regulation * Disclosure Knowledge [0.10] Observations R-squared

![11] Auditor Home -0.13-0.13 [0.17] [0.17] Agent Office -0.05-0.05 [0.10] [0.10] Auditor Office -0.04-0.04 [0.20] [0.](/docs-images/54/10338382/images/page_19.jpg "20] LIC -0.44*** -0.44*** [0.05] [0.05] Post Disclosure Regulation * Disclosure Knowledge -0.02 [0.")

20 Disclosure Results

21 Improving Advice: Competition? Competition and bad advice: does the threat of losing a sale to another agent make an agent more likely to match needs of customer? Vary level of competition by varying source of beliefs: I have heard from a friend that whole (life)... I have heard from another agent from whom I am considering purchasing... Does agent try to win business by correcting another agent?

22 Does Competition Matter for Type of Advice? Agents de-bias when advice comes from another agent Statistically significant at 5 percent level Note that this de-biasing is mainly through recommending term in addition to whole

23 Improving Advice: Sophisticated vs. Un-Sophisticated Customers High level of sophistication: In the past, I have spent time shopping for the policies, and am perhaps surprisingly somewhat familiar with the different types of policies: ULIPs, term, whole life insurance. However, I am less familiar with the specific policies that your firm offers, so I was hoping you can walk me through them and recommend a policy specific for my situation. Low level of sophistication: I am aware that Life Insurance products are complex, and I don t understand them very much. However I am interested in learning, what type of policy may be right for me? Delivered in introduction of auditor to agent Remainder of script unchanged In particular, stated income held constant

24 Sophistication Results: Product Recommendation (1) (2) (3) (4) Dependent Variable: Any Term Only Term Ln(Coverage) Ln(Premium) Sophisticated 0.10* 0.10 * 0.21* [0.06] [0.06] [0.12] [0.10] Government Underwriter [0.07] [0.06] [0.16] [0.10] Auditor FE YES YES YES YES Audit Location FE YES YES YES YES Observations Sophisticated agents 10 percentage points less likely to receive recommendation of any term Sophisticated agents also recommend to buy more coverage, but not to pay more premiums - consistent with catering to premium amount story

25 Conclusion Quality of Advice Agents mainly recommend whole despite fact that term + savings seems to dominate Even to customers who mainly want risk coverage Agents will cater to incorrect beliefs When agents do recommend term, they prefer to do it as a package (whole + term) Improving Advice When agents forced to disclose information changes advice Some evidence that agents will compete by providing different advice When consumer signals sophistication gets weakly better advice

Understanding the Incentives of Commissions Motivated Agents: Theory and Evidence from the Indian Life Insurance Market

Understanding the Incentives of Commissions Motivated Agents: Theory and Evidence from the Indian Life Insurance Market Santosh Anagol Shawn Cole Shayak Sarkar Working Paper 12-055 January 2, 2012 Copyright

Understanding the Incentives of Commissions Motivated Agents: Theory and Evidence from the Indian Life Insurance Market Santosh Anagol Shawn Cole Shayak Sarkar Working Paper 12-055 January 2, 2012 Copyright

Bad Advice: Explaining the Persistence of Whole Life Insurance

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School June 5, 2011 Shayak Sarkar Harvard University Abstract We conduct a series of field

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School June 5, 2011 Shayak Sarkar Harvard University Abstract We conduct a series of field

Bad Advice: Explaining the Persistence of Whole Life Insurance

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School April 12, 2011 Shayak Sarkar Harvard University Abstract We conduct a series of

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School April 12, 2011 Shayak Sarkar Harvard University Abstract We conduct a series of

Bad Advice: Explaining the Persistence of Whole Life Insurance

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School July 2010 Shayak Sarkar Harvard University Abstract We conduct a series of field

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School July 2010 Shayak Sarkar Harvard University Abstract We conduct a series of field

Bad Advice: Explaining the Persistence of Whole Life Insurance

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School October 29, 2010 Shayak Sarkar Harvard University Abstract We conduct a series of

Bad Advice: Explaining the Persistence of Whole Life Insurance Santosh Anagol Wharton Shawn Cole Harvard Business School October 29, 2010 Shayak Sarkar Harvard University Abstract We conduct a series of

Understanding the Advice of Commissions-Motivated Agents: Evidence from the Indian Life Insurance Market

Understanding the Advice of Commissions-Motivated Agents: Evidence from the Indian Life Insurance Market Santosh Anagol Shawn Cole Shayak Sarkar Working Paper 12-055 March 7, 2013 Copyright 2012, 2013

Understanding the Advice of Commissions-Motivated Agents: Evidence from the Indian Life Insurance Market Santosh Anagol Shawn Cole Shayak Sarkar Working Paper 12-055 March 7, 2013 Copyright 2012, 2013

Unit-Linked Insurance Policies in the Indian Market- A Consumer Perspective

Unit-Linked Insurance Policies in the Indian Market- A Consumer Perspective R. Rajagopalan 1 Dean (Academic Affairs) T.A. Pai Management Institute Manipal-576 104 Email: raja@mail.tapmi.org 1 The author

Unit-Linked Insurance Policies in the Indian Market- A Consumer Perspective R. Rajagopalan 1 Dean (Academic Affairs) T.A. Pai Management Institute Manipal-576 104 Email: raja@mail.tapmi.org 1 The author

Term Life vs. Permanent Life Insurance

Term Life vs. Permanent Life Insurance Should I Buy Term or Permanent? A widow doesn t ask What kind of insurance was it - Whole Life, Universal Life or Term? She asks How much do I have to raise my family?

Term Life vs. Permanent Life Insurance Should I Buy Term or Permanent? A widow doesn t ask What kind of insurance was it - Whole Life, Universal Life or Term? She asks How much do I have to raise my family?

Understanding the Advice of Commissions-Motivated Agents: Evidence from the Indian Life Insurance Market

Understanding the Advice of Commissions-Motivated Agents: Evidence from the Indian Life Insurance Market Santosh Anagol Wharton Shawn Cole Harvard Business School January 16, 2013 Shayak Sarkar Harvard

Understanding the Advice of Commissions-Motivated Agents: Evidence from the Indian Life Insurance Market Santosh Anagol Wharton Shawn Cole Harvard Business School January 16, 2013 Shayak Sarkar Harvard

Life Insurance, Really?

YNAB PRESENTS Life Insurance, Really? A primer on why you need it, what you need (and what you don t). YouNeedABudget.com The idea of life insurance is pretty disturbing. Honestly, I d rather be talking

YNAB PRESENTS Life Insurance, Really? A primer on why you need it, what you need (and what you don t). YouNeedABudget.com The idea of life insurance is pretty disturbing. Honestly, I d rather be talking

Your Guide to Living Benefits

Easy to read, understandable, and timely... Charlie Denholm Your Guide to Living Benefits THE BEST KEPT SECRET IN AMERICA By Richard Drazien, CLU, SRM Chapter 6 OK, You Have My Attention. Show Me The Money!

Easy to read, understandable, and timely... Charlie Denholm Your Guide to Living Benefits THE BEST KEPT SECRET IN AMERICA By Richard Drazien, CLU, SRM Chapter 6 OK, You Have My Attention. Show Me The Money!

Society of Actuaries Middle Market Life Insurance Segmentation Program (Phase 1: Young Families)

") Society of Actuaries Middle Market Life Insurance Segmentation Program (Phase 1: Young Families) September 2012 Sponsored By: SOA Marketing and Distribution Section SOA Product Development Section SOA

Society of Actuaries Middle Market Life Insurance Segmentation Program (Phase 1: Young Families) September 2012 Sponsored By: SOA Marketing and Distribution Section SOA Product Development Section SOA

Life Insurance Modelling: Notes for teachers. Overview

Life Insurance Modelling: Notes for teachers In this mathematics activity, students model the following situation: An investment fund is set up Investors pay a set amount at the beginning of 20 years.

Life Insurance Modelling: Notes for teachers In this mathematics activity, students model the following situation: An investment fund is set up Investors pay a set amount at the beginning of 20 years.

Why do I need protection?

Why do I need protection? What s inside 3 Life cover 4 Critical illness cover 7 Income protection 8 Who else would you rely on? 10 It might cost less than you think 12 A word from your adviser... Introduction

Why do I need protection? What s inside 3 Life cover 4 Critical illness cover 7 Income protection 8 Who else would you rely on? 10 It might cost less than you think 12 A word from your adviser... Introduction

China s Middle Market for Life Insurance

China s Middle Market for Life Insurance May 2014 Sponsored by: SOA International Section SOA Marketing & Distribution Section SOA Research Expanding Boundaries Pool The opinions expressed and conclusions

China s Middle Market for Life Insurance May 2014 Sponsored by: SOA International Section SOA Marketing & Distribution Section SOA Research Expanding Boundaries Pool The opinions expressed and conclusions

2) You must then determine how much of the risk you are willing to assume.

You must then determine how much of the risk you are willing to assume.") CHAPTER 4 Life Insurance Structure, Concepts, and Planning Strategies Where can you make a Simpler living as a needs financial planner? 1) Wealthy clients have a much higher profit margin. The challenge

CHAPTER 4 Life Insurance Structure, Concepts, and Planning Strategies Where can you make a Simpler living as a needs financial planner? 1) Wealthy clients have a much higher profit margin. The challenge

The Hidden costs of Permanent Insurance Policies revealed by an Actuary By Rajiv Rebello, Principal, Colva Insurance Services

The Hidden costs of Permanent Insurance Policies revealed by an Actuary By Rajiv Rebello, Principal, Colva Insurance Services For first time buyers of life insurance, the plethora of choices available

The Hidden costs of Permanent Insurance Policies revealed by an Actuary By Rajiv Rebello, Principal, Colva Insurance Services For first time buyers of life insurance, the plethora of choices available

Santosh Anagol Shawn Cole Laura Litvine. R E S E A R C H P A P E R N o. 3 9 M A R C H 2 0 1 4

CAN DEBIASING PROVIDED OVER THE INTERNET IMPROVE CONSUMER FINANCIAL DECISIONS? EVIDENCE FROM EXPERIMENTS ON LIFE INSURANCE DECISIONS FROM INDIA AND THE U.S. Santosh Anagol Shawn Cole Laura Litvine R E

CAN DEBIASING PROVIDED OVER THE INTERNET IMPROVE CONSUMER FINANCIAL DECISIONS? EVIDENCE FROM EXPERIMENTS ON LIFE INSURANCE DECISIONS FROM INDIA AND THE U.S. Santosh Anagol Shawn Cole Laura Litvine R E

EXECUTIVE SUMMARY OF MINOR RESEARCH PROJECT (UGC) _ Mr Ishwara Gowda

_ Mr Ishwara Gowda") EXECUTIVE SUMMARY OF MINOR RESEARCH PROJECT (UGC) _ Mr Ishwara Gowda TITLE: AWARENESS OF RURAL INSURANCE SCHEMES:-A SPECIAL STUDY OF RURAL INSURANCE AND LIC WITH REFERENCE TO BELTHANGADY TALUK. It is a

EXECUTIVE SUMMARY OF MINOR RESEARCH PROJECT (UGC) _ Mr Ishwara Gowda TITLE: AWARENESS OF RURAL INSURANCE SCHEMES:-A SPECIAL STUDY OF RURAL INSURANCE AND LIC WITH REFERENCE TO BELTHANGADY TALUK. It is a

Before you agree to buy a house, make sure

SPECIAL ALERT Office of the Attorney General, Consumer Protection Division Home Buyers: Beware of Flipping Scams Bought by "flipper" $24,000 February Before you agree to buy a house, make sure you re not

SPECIAL ALERT Office of the Attorney General, Consumer Protection Division Home Buyers: Beware of Flipping Scams Bought by "flipper" $24,000 February Before you agree to buy a house, make sure you re not

WEEKWISE SYLLABUS 2015-16 CLASS : XI (VOCATIONAL) SUBJECT : LIFE INSURANCE (786) TIME : 3 HRS. M.M. : 100 THEORY 60 PRACTICAL

SUBJECT : LIFE INSURANCE (786) TIME : 3 HRS. M.M. : 100 THEORY 60 PRACTICAL") WEEKWISE SYLLABUS 2015-16 CLASS : XI (VOCATIONAL) SUBJECT : LIFE INSURANCE (786) TIME : 3 HRS. M.M. : 100 THEORY 60 PRACTICAL 40 THEORY PRACTICAL Unit-1 : Introduction to Insurance and Practice of Insurance

WEEKWISE SYLLABUS 2015-16 CLASS : XI (VOCATIONAL) SUBJECT : LIFE INSURANCE (786) TIME : 3 HRS. M.M. : 100 THEORY 60 PRACTICAL 40 THEORY PRACTICAL Unit-1 : Introduction to Insurance and Practice of Insurance

Complete Guide to Reverse Mortgages

Complete Guide to Reverse Mortgages Contents I. What Is a Reverse Mortgage? 2 Reasons for taking out a reverse mortgage 2 Differences between reverse and traditional mortgages 2 II. Where to Get Reverse

Complete Guide to Reverse Mortgages Contents I. What Is a Reverse Mortgage? 2 Reasons for taking out a reverse mortgage 2 Differences between reverse and traditional mortgages 2 II. Where to Get Reverse

Understanding the Basics of Term Life Insurance LIFE. Your future. Made easier.

Understanding the Basics of Term Life Insurance LIFE Your future. Made easier. I already have group insurance with my company. Why should I purchase more insurance? Since many companies offer group insurance

Understanding the Basics of Term Life Insurance LIFE Your future. Made easier. I already have group insurance with my company. Why should I purchase more insurance? Since many companies offer group insurance

Protection is Precious. Life Insurance

Protection is Precious Life Insurance Not FDIC/NCUA Insured Not Insured By Any Federal Government Entity Not a Deposit May Lose Value No Bank/Credit Union Guarantee Subject to Underwriter Approval What

Protection is Precious Life Insurance Not FDIC/NCUA Insured Not Insured By Any Federal Government Entity Not a Deposit May Lose Value No Bank/Credit Union Guarantee Subject to Underwriter Approval What

Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01

UIN: 104N076V01") IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICYHOLDER LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT About Max Life Max Life Insurance, ne of the leading non-bank

IN THIS POLICY, THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS BORNE BY THE POLICYHOLDER LIFE INSURANCE COVERAGE IS AVAILABLE IN THIS PRODUCT About Max Life Max Life Insurance, ne of the leading non-bank

Life insurance quote. Who the policy covers. Your total monthly payment will be: 14.60. This quote is only valid for 30 days

Life insurance quote This quote has been prepared for Mr Rick Jones by LifeQuotes4U on 30th April 2013. You should read the details of your quote in conjunction with the Key Features in order to make your

Life insurance quote This quote has been prepared for Mr Rick Jones by LifeQuotes4U on 30th April 2013. You should read the details of your quote in conjunction with the Key Features in order to make your

Life Insurance Buyer s Guide

Page 1 of 5 Life Insurance Buyer s Guide Illinois This guide can show you how to save money when you shop for life insurance. It helps you to: Decide how much life insurance you should buy, Decide what

Page 1 of 5 Life Insurance Buyer s Guide Illinois This guide can show you how to save money when you shop for life insurance. It helps you to: Decide how much life insurance you should buy, Decide what

Life Insurance Capacity Calculator. Producer Guide. For agent use only. Not for public distribution.

Life Insurance Capacity Calculator Producer Guide What is a Life Insurance Capacity Calculator? The Voya TM Life Companies Life Insurance Capacity (LIC) Calculator is a life insurance sales tool which

Life Insurance Capacity Calculator Producer Guide What is a Life Insurance Capacity Calculator? The Voya TM Life Companies Life Insurance Capacity (LIC) Calculator is a life insurance sales tool which

Trendsetter. LB Series. Product Overview

Trendsetter LB Series Product Overview Trendsetter LB Series Life happens. Are you prepared? Sometimes we are surprised by what happens in life. One of the most important assets we have is our health

Trendsetter LB Series Product Overview Trendsetter LB Series Life happens. Are you prepared? Sometimes we are surprised by what happens in life. One of the most important assets we have is our health

How to Trade Almost Any Asset in the World from a Single Account Using CFDs

How to Trade Almost Any Asset in the World from a Single Account Using CFDs How to Trade Almost Any Asset in the World from a Single Account Using CFDs Shae Russell, Editor INTRODUCTION TO TRADING CFDS

How to Trade Almost Any Asset in the World from a Single Account Using CFDs How to Trade Almost Any Asset in the World from a Single Account Using CFDs Shae Russell, Editor INTRODUCTION TO TRADING CFDS

Investment-linked Insurance plans (ILPs)

") Produced by > your guide to Investment-linked Insurance plans (ILPs) An initiative of This Guide is an initiative of the MoneySENSE national financial education programme. The MoneySENSE programme brings

Produced by > your guide to Investment-linked Insurance plans (ILPs) An initiative of This Guide is an initiative of the MoneySENSE national financial education programme. The MoneySENSE programme brings

Life Insurance Buyer's Guide

United of Omaha Life Insurance Company Life Insurance Buyer s Guide Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

United of Omaha Life Insurance Company Life Insurance Buyer s Guide Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

UNIT 7 1 Applying for a Home Mortgage

UNIT 7 1 Applying for a Home Mortgage Regardless of where you get your mortgage, the issuer is not likely to keep the mortgage for the duration of the loan. So, if you get your mortgage at a local bank,

UNIT 7 1 Applying for a Home Mortgage Regardless of where you get your mortgage, the issuer is not likely to keep the mortgage for the duration of the loan. So, if you get your mortgage at a local bank,

A Guide to Investing in Property Using a Self Managed Super Fund

A Guide to Investing in Property Using a Self Managed Super Fund Why would I consider a SMSF? I already have a super fund. Self Managed Superannuation Funds (SMSF s) are the fastest growing sector of the

A Guide to Investing in Property Using a Self Managed Super Fund Why would I consider a SMSF? I already have a super fund. Self Managed Superannuation Funds (SMSF s) are the fastest growing sector of the

India Life Insurance Survey May 2011

India Life Insurance Survey May 2011 In May 2011, Milliman carried out a survey of the C-level life insurance executives (covering CEOs / CFOs / Appointed Actuaries / Chief Actuaries) to gauge their views

India Life Insurance Survey May 2011 In May 2011, Milliman carried out a survey of the C-level life insurance executives (covering CEOs / CFOs / Appointed Actuaries / Chief Actuaries) to gauge their views

A Guide To Life Insurance and Protection

A Guide To Life Insurance and Protection Independent Financial Advisers Independent Mortgage Advisers P N DALES LTD, are an Independent Financial Advisers, experts in protection & life insurance. We help

A Guide To Life Insurance and Protection Independent Financial Advisers Independent Mortgage Advisers P N DALES LTD, are an Independent Financial Advisers, experts in protection & life insurance. We help

Life Insurance Buyer s Guide

Life Insurance Buyer s Guide This guide can show you how to save money when you shop for life insurance. It helps you to: - Decide how much life insurance you should buy, - Decide what kind of life insurance

Life Insurance Buyer s Guide This guide can show you how to save money when you shop for life insurance. It helps you to: - Decide how much life insurance you should buy, - Decide what kind of life insurance

Life insurance policy reviews

Allianz Life Insurance Company of North America P For financial professional use only. Not for use with the public. Life insurance policy reviews Help your clients, build your business M-3962 Page 1 of

Allianz Life Insurance Company of North America P For financial professional use only. Not for use with the public. Life insurance policy reviews Help your clients, build your business M-3962 Page 1 of

-17-5. Life Insurance: What to Look For

-17-5. Life Insurance: What to Look For Have you ever thought about buying life insurance? Have you ever puzzled about whether you needed it and if you did, how much to buy? Or what kind? Or how to compare

-17-5. Life Insurance: What to Look For Have you ever thought about buying life insurance? Have you ever puzzled about whether you needed it and if you did, how much to buy? Or what kind? Or how to compare

CREATE TAX ADVANTAGED RETIREMENT INCOME YOU CAN T OUTLIVE. create tax advantaged retirement income you can t outlive

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

How to Avoid The Five Biggest First-time Homebuyer Mistakes. Mistake #1

How to Avoid The Five Biggest First-time Homebuyer Mistakes Mistake #1 Failure To Examine And Repair Any Credit Problems Prior To Applying For Your Loan Many potential new home buyers have no idea what

How to Avoid The Five Biggest First-time Homebuyer Mistakes Mistake #1 Failure To Examine And Repair Any Credit Problems Prior To Applying For Your Loan Many potential new home buyers have no idea what

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Money Math for Teens. Dividend-Paying Stocks

Money Math for Teens Dividend-Paying Stocks This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Money Math for Teens Dividend-Paying Stocks This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features

Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features") RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Start counting on yourself

Start counting on yourself Start with life insurance on your terms ING ROP Endowment Term and ING ROP Endowment Term NY Term Life Insurance issued by ReliaStar Life Insurance Company and ReliaStar Life

Start counting on yourself Start with life insurance on your terms ING ROP Endowment Term and ING ROP Endowment Term NY Term Life Insurance issued by ReliaStar Life Insurance Company and ReliaStar Life

Investment by foreign direct investors in to Insurance company is restricted to 12% 25% 40% 26%

In life insurance business if a person is working in calculating premium rates of insurance products, then he is mostly likely a member of Institutes of actuaries of India Insurance institute of India

In life insurance business if a person is working in calculating premium rates of insurance products, then he is mostly likely a member of Institutes of actuaries of India Insurance institute of India

Retiring from the Family Business Last update: October 27, 2011

Summary Retiring from the Family Business Last update: October 27, 2011 If you are the owner or a major partner in a small business, your retirement concerns are more complex than most people s. It is

Summary Retiring from the Family Business Last update: October 27, 2011 If you are the owner or a major partner in a small business, your retirement concerns are more complex than most people s. It is

Get life insurance with guaranteed returns on your investment.*

P RODUCT B ROCHURE Protection. Protection with guaranteed returns. Get life insurance with guaranteed returns on your investment.* Invest ` 1 lakh and get ` 1.801 lakhs after 10, plus life cover. (For

P RODUCT B ROCHURE Protection. Protection with guaranteed returns. Get life insurance with guaranteed returns on your investment.* Invest ` 1 lakh and get ` 1.801 lakhs after 10, plus life cover. (For

Benefits of Insurance and Tips on Buying Insurance

Lets. 1 Benefits of Insurance and Tips on Buying Insurance 2 Benefits of Insurance 3 4 What is insurance? Insurance is a form of management used to offer a financial payment when unplanned or unexpected

Lets. 1 Benefits of Insurance and Tips on Buying Insurance 2 Benefits of Insurance 3 4 What is insurance? Insurance is a form of management used to offer a financial payment when unplanned or unexpected

Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01

UIN: 104N076V01") About Max Life Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01 Max Life Insurance, one of the leading non-bank

About Max Life Max Life Guaranteed Lifetime Income Plan Pension (A Traditional Non Linked Non Participating Immediate Annuity Pension Plan) UIN: 104N076V01 Max Life Insurance, one of the leading non-bank

FRS Pension Payout Options

FRS Pension Payout Options The income distribution option that a Pension Plan participant chooses is easily one of the most important financial decisions they will make in their life and, potentially,

FRS Pension Payout Options The income distribution option that a Pension Plan participant chooses is easily one of the most important financial decisions they will make in their life and, potentially,

Life insurance policy reviews

Allianz Life Insurance Company of North America P For financial professional use only. Not for use with the public. Life insurance policy reviews Help your clients, build your business M-3962 Page 1 of

Allianz Life Insurance Company of North America P For financial professional use only. Not for use with the public. Life insurance policy reviews Help your clients, build your business M-3962 Page 1 of

Reverse Mortgage Nightmares Should Never Happen Top 10 Misconceptions About Reverse Mortgages 14

Reverse Mortgage Nightmares Should Never Happen Top 10 Misconceptions About Reverse Mortgages 14 Searching online for information about reverse mortgages, I came across article after article about how

Reverse Mortgage Nightmares Should Never Happen Top 10 Misconceptions About Reverse Mortgages 14 Searching online for information about reverse mortgages, I came across article after article about how

The Basics of Life Settlements

The Basics of Life Settlements AN EDUCATIONAL GUIDE FOR CONSUMERS THE VOICE OF THE INDUSTRY THE BASICS OF LIFE SETTLEMENTS The Basics of Life Settlements 1 The Concept of Life Settlements 4 Free Market

The Basics of Life Settlements AN EDUCATIONAL GUIDE FOR CONSUMERS THE VOICE OF THE INDUSTRY THE BASICS OF LIFE SETTLEMENTS The Basics of Life Settlements 1 The Concept of Life Settlements 4 Free Market

Registered Investment Advisor Firm

Registered Investment Advisor Firm Issue VI, Vol. III Bud Heng Registered Adviser (925) 360-6819 June 2014 Congratulation Graduates! For the graduating class of 2014, let me be among the first to say congratulations!

Registered Investment Advisor Firm Issue VI, Vol. III Bud Heng Registered Adviser (925) 360-6819 June 2014 Congratulation Graduates! For the graduating class of 2014, let me be among the first to say congratulations!

Case Study 2 Protection Planner

Case Study 2 Protection Planner Objectives Anthony and Alan are keen to implement some form of succession planning for their business because neither of them have children nor any obvious management successors.

Case Study 2 Protection Planner Objectives Anthony and Alan are keen to implement some form of succession planning for their business because neither of them have children nor any obvious management successors.

ING Return of Premium Term Term life insurance issued by ReliaStar Life Insurance Company

Start counting on yourself. Start with life insurance on your terms. ING Return of Premium Term Term life insurance issued by ReliaStar Life Insurance Company Take a moment to listen to Ida, an old friend

Start counting on yourself. Start with life insurance on your terms. ING Return of Premium Term Term life insurance issued by ReliaStar Life Insurance Company Take a moment to listen to Ida, an old friend

Protecting Your Loved Ones Every Step of the Way

Protecting Your Loved Ones Every Step of the Way Gerber Life Insurance Company Gerber Life Insurance Company, White Plains, NY 10605 5/10/2011 Gerber Life Insurance Company is a financially separate affiliate

Protecting Your Loved Ones Every Step of the Way Gerber Life Insurance Company Gerber Life Insurance Company, White Plains, NY 10605 5/10/2011 Gerber Life Insurance Company is a financially separate affiliate

Securities and Advisory Services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser.

FACTORS IN THE DECISION TO REPLACE OR EXCHANGE A LIFE INSURANCE POLICY You own a life insurance policy, having purchased it some time ago after you researched all the issues involved and evaluated the

FACTORS IN THE DECISION TO REPLACE OR EXCHANGE A LIFE INSURANCE POLICY You own a life insurance policy, having purchased it some time ago after you researched all the issues involved and evaluated the

Money and the Single Parent. Apprisen. 800.355.2227 www.apprisen.com

Money and the Single Parent Apprisen 800.355.2227 www.apprisen.com Money and the Single Parent Being a single parent is not easy. As a matter of fact, it is really hard. Single parents are stretched in

Money and the Single Parent Apprisen 800.355.2227 www.apprisen.com Money and the Single Parent Being a single parent is not easy. As a matter of fact, it is really hard. Single parents are stretched in

RULES OF THE DEPARTMENT OF INSURANCE DIVISION OF INSURANCE CHAPTER 0780-1-40 RELATING TO LIFE INSURANCE SOLICITATION TABLE OF CONTENTS

RULES OF THE DEPARTMENT OF INSURANCE DIVISION OF INSURANCE CHAPTER 0780-1-40 RELATING TO LIFE INSURANCE SOLICITATION TABLE OF CONTENTS 0780-1-40-.01 Purpose 0780-1-40-.05 General Rules 0780-1-40-.02 Scope

RULES OF THE DEPARTMENT OF INSURANCE DIVISION OF INSURANCE CHAPTER 0780-1-40 RELATING TO LIFE INSURANCE SOLICITATION TABLE OF CONTENTS 0780-1-40-.01 Purpose 0780-1-40-.05 General Rules 0780-1-40-.02 Scope

Life Insurance Capacity Calculator

Life Insurance Capacity Calculator LIFE For agent INSURANCE use only. Not for public distribution. Your future. Made easier. Life Insurance Capacity Calculator What is it? The ING life companies Life Insurance

Life Insurance Capacity Calculator LIFE For agent INSURANCE use only. Not for public distribution. Your future. Made easier. Life Insurance Capacity Calculator What is it? The ING life companies Life Insurance

Understanding the Basics of Term Life Insurance LIFE INSURANCE. Your future. Made easier.

Understanding the Basics of Term Life Insurance LIFE INSURANCE Your future. Made easier. I already have group insurance with my company. Why should I purchase more insurance? Since many companies offer

Understanding the Basics of Term Life Insurance LIFE INSURANCE Your future. Made easier. I already have group insurance with my company. Why should I purchase more insurance? Since many companies offer

Start small. Save big.

Start small. Save big. PRODUCT BROCHURE A long term savings plan with bonuses, guaranteed additions and insurance protection* *Terms and Conditions apply. Your life is full of responsibilities. As a responsible

Start small. Save big. PRODUCT BROCHURE A long term savings plan with bonuses, guaranteed additions and insurance protection* *Terms and Conditions apply. Your life is full of responsibilities. As a responsible

Learning Journey. Max Vijay

Learning Journey Max Vijay Reducing costs by leveraging technology and educating the customers, to bring life insurance benefits to the low-income people Contents Project Basics... 1 About the project...

Learning Journey Max Vijay Reducing costs by leveraging technology and educating the customers, to bring life insurance benefits to the low-income people Contents Project Basics... 1 About the project...

Suggested Standards for Product Designers, Managers and Distributors. June 2013. Edition 3.0

Suggested Standards for Product Designers, Managers and Distributors June 2013 Edition 3.0 FOREWORD Edition 1.0 of the European Life Settlement Association (ELSA) Code of Practice (the Code) was introduced

Suggested Standards for Product Designers, Managers and Distributors June 2013 Edition 3.0 FOREWORD Edition 1.0 of the European Life Settlement Association (ELSA) Code of Practice (the Code) was introduced

Copyright Notice & Legal Notice 2012 LifeNet Insurance Solutions 11505 Eastridge Drive NE Suite 420 Redmond, WA 98053-5758

Copyright Notice & Legal Notice 2012 LifeNet Insurance Solutions 11505 Eastridge Drive NE Suite 420 Redmond, WA 98053-5758 Feel free to share this ebook (FOR FREE) with anyone you want to. All rights reserved.

Copyright Notice & Legal Notice 2012 LifeNet Insurance Solutions 11505 Eastridge Drive NE Suite 420 Redmond, WA 98053-5758 Feel free to share this ebook (FOR FREE) with anyone you want to. All rights reserved.

life INSURANcE The Boring Money guide to Yes. You over there trying to avoid the subject. Listen up!

life The Boring Money guide to INSURANcE Yes. You over there trying to avoid the subject. Listen up! Oh puh-lease, do I have to!? Come on, let s be honest. From the second you know you re pregnant, you

life The Boring Money guide to INSURANcE Yes. You over there trying to avoid the subject. Listen up! Oh puh-lease, do I have to!? Come on, let s be honest. From the second you know you re pregnant, you

What is a Short Sale?

What is a Short Sale? A Short Sale is used to describe the sale of a home in which the homeowner owes the bank more than the home is worth. The bank agrees to allow the home to be sold for less than what

What is a Short Sale? A Short Sale is used to describe the sale of a home in which the homeowner owes the bank more than the home is worth. The bank agrees to allow the home to be sold for less than what

Life Settlements Product Overview

Life Settlements Product Overview Leveraging Life Settlements in Writing New Business Contents What is a Life Settlement? Case study Options for unwanted policies Who buys these policies? How does it work?

Life Settlements Product Overview Leveraging Life Settlements in Writing New Business Contents What is a Life Settlement? Case study Options for unwanted policies Who buys these policies? How does it work?

What You Should Know About Buying. Life Insurance

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

BUSINESS CASE STUDIES

BUSINESS CASE STUDIES Below you will find 2 Case Studies of 2 very different organisations. An small Advertising Firm; & a well established Construction Equipment Hire Business. Most business owners have

BUSINESS CASE STUDIES Below you will find 2 Case Studies of 2 very different organisations. An small Advertising Firm; & a well established Construction Equipment Hire Business. Most business owners have

White Paper No. 59: The Last, Best Tax Shelter Ever?

White Paper No. 59: The Last, Best Tax Shelter Ever? A s tax rates declined from the stratospheric levels that prevailed in the middle of the Twentieth Century, the need for tax shelters diminished. And

White Paper No. 59: The Last, Best Tax Shelter Ever? A s tax rates declined from the stratospheric levels that prevailed in the middle of the Twentieth Century, the need for tax shelters diminished. And

Value what your family values the most, you. Protect yourself now in 3 easy steps.

Value what your family values the most, you. Protect yourself now in 3 easy steps. Birla Sun Life Insurance Protect@Ease A traditional online term insurance plan INTRODUCING BSLI Protect@Ease You are successful

Value what your family values the most, you. Protect yourself now in 3 easy steps. Birla Sun Life Insurance Protect@Ease A traditional online term insurance plan INTRODUCING BSLI Protect@Ease You are successful

APPENDIX 1 QUESTIONNAIRE TO BENEFICIARIES PLEASE ANSWER FOR THE FOLLOWING QUESTIONS, YOUR IDENTITY IS GUARDED. PLEASE FEEL FREE TO GIVE YOUR COMMENTS.

396 APPENDIX 1 QUESTIONNAIRE TO BENEFICIARIES PLEASE ANSWER FOR THE FOLLOWING QUESTIONS, YOUR IDENTITY IS GUARDED. PLEASE FEEL FREE TO GIVE YOUR COMMENTS. GENERAL INFORMATION : 1. Policy number (optional)

396 APPENDIX 1 QUESTIONNAIRE TO BENEFICIARIES PLEASE ANSWER FOR THE FOLLOWING QUESTIONS, YOUR IDENTITY IS GUARDED. PLEASE FEEL FREE TO GIVE YOUR COMMENTS. GENERAL INFORMATION : 1. Policy number (optional)

Private annuity/trust

Deferring Capital Gains Taxes With A Private annuity/trust TM The National Association of Financial and Estate Planning NAFEP, 1999 and 2001 Revision 2 DEFERRAL OF CAPITAL GAINS AND DEPRECIATION RECAPTURE

Deferring Capital Gains Taxes With A Private annuity/trust TM The National Association of Financial and Estate Planning NAFEP, 1999 and 2001 Revision 2 DEFERRAL OF CAPITAL GAINS AND DEPRECIATION RECAPTURE

Safeguard your family's future against life's uncertainties

Safeguard your family's future against life's uncertainties Birla Sun Life Insurance Easy Protect Plan A traditional term insurance plan INTRODUCING BSLI Easy Protect Plan You are successful in your career

Safeguard your family's future against life's uncertainties Birla Sun Life Insurance Easy Protect Plan A traditional term insurance plan INTRODUCING BSLI Easy Protect Plan You are successful in your career

Destiny. a guide for clients

Destiny a guide for clients 1 For those who prefer choice over chance Destiny is universal life insurance that provides a broad spectrum of choices to protect your life, your investments, and your business.

Destiny a guide for clients 1 For those who prefer choice over chance Destiny is universal life insurance that provides a broad spectrum of choices to protect your life, your investments, and your business.

A New Course for Health Insurance Agents? (An easy way to convert health insurance clients into financial products clients!)

") A New Course for Health Insurance Agents? (An easy way to convert health insurance clients into financial products clients!) Written by Bill O Quin, CLU, ChFC, RFC and adapted from The Virtual Assistant

A New Course for Health Insurance Agents? (An easy way to convert health insurance clients into financial products clients!) Written by Bill O Quin, CLU, ChFC, RFC and adapted from The Virtual Assistant

MICHAEL HODGES AND BRETT COOPER

WHY COPY TRADE FOREX MICHAEL HODGES AND BRETT COOPER WHAT IS FOREX COPY TRADING Forex copy trading is a relatively new way of trading currency. It takes a lot of the risk and hassle out of trading and

WHY COPY TRADE FOREX MICHAEL HODGES AND BRETT COOPER WHAT IS FOREX COPY TRADING Forex copy trading is a relatively new way of trading currency. It takes a lot of the risk and hassle out of trading and

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality

First Regional Europa Re Conference Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality 12-14 October 2011 Ohrid, FYR of Macedonia Exploring alternative product

First Regional Europa Re Conference Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality 12-14 October 2011 Ohrid, FYR of Macedonia Exploring alternative product

RNIS COLLEGE OF INSURANCE

RNIS COLLEGE OF INSURANCE NEW IC 33 MODEL TEST 3 1. What fee is payable by the aggrieved person to the District Consumer Forum while filing his complaint? a. Rs.250 b. Rs.100 c. 10% of the relief sought

RNIS COLLEGE OF INSURANCE NEW IC 33 MODEL TEST 3 1. What fee is payable by the aggrieved person to the District Consumer Forum while filing his complaint? a. Rs.250 b. Rs.100 c. 10% of the relief sought

Society of Actuaries Research

Society of Actuaries Research R. Dale Hall, FSA, MAAA, CERA, CFA Managing Director of Research Society of Actuaries dhall@soa.org @RDaleHall Society of Actuaries Overview 24,000 worldwide members Based

Society of Actuaries Research R. Dale Hall, FSA, MAAA, CERA, CFA Managing Director of Research Society of Actuaries dhall@soa.org @RDaleHall Society of Actuaries Overview 24,000 worldwide members Based

afe Money Concepts James Schultz From Badger Insurance

afe Money Concepts James Schultz From Badger Insurance 220 Grant Street, Fort Atkinson, WI 53538 Phone: (920) 563-2478 Email: jimschultz@badgerbank.com INTRODUCTION It s hard to say where and when most

afe Money Concepts James Schultz From Badger Insurance 220 Grant Street, Fort Atkinson, WI 53538 Phone: (920) 563-2478 Email: jimschultz@badgerbank.com INTRODUCTION It s hard to say where and when most

1/26/96 (Effective 11/3/95) 211 CMR - 143

211 CMR - 143") 211 CMR 31.00: LIFE INSURANCE SOLICITATION Section 31.01: : Authority 31.02: : Purpose 31.03: : Scope 31.04: : Definitions 31.05: Disclosure RequirementsDuties of Insurers 31.06: Pre-Need Funeral Contracts

211 CMR 31.00: LIFE INSURANCE SOLICITATION Section 31.01: : Authority 31.02: : Purpose 31.03: : Scope 31.04: : Definitions 31.05: Disclosure RequirementsDuties of Insurers 31.06: Pre-Need Funeral Contracts

How to Write a Marketing Plan: Identifying Your Market

How to Write a Marketing Plan: Identifying Your Market (Part 1 of 5) Any good marketing student will tell you that marketing consists of the four functions used to create a sale: The right product to the

How to Write a Marketing Plan: Identifying Your Market (Part 1 of 5) Any good marketing student will tell you that marketing consists of the four functions used to create a sale: The right product to the

What You Should Know About Buying. Life Insurance

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

What You Should Know About Buying Life Insurance Life insurance is the foundation of financial security for you and your family. It protects your financial resources against the uncertainties of life so

WHAT YOU SHOULD KNOW. About Buying Life Insurance. Life insurance is financial protection. It provides the

Life insurance is financial protection. It provides the resources your family may need to pay immediate and continuing expenses after you die. WHAT YOU SHOULD KNOW About Buying Life Insurance There are

Life insurance is financial protection. It provides the resources your family may need to pay immediate and continuing expenses after you die. WHAT YOU SHOULD KNOW About Buying Life Insurance There are

7 Secrets To Websites That Sell. By Alex Nelson

7 Secrets To Websites That Sell By Alex Nelson Website Secret #1 Create a Direct Response Website Did you know there are two different types of websites? It s true. There are branding websites and there

7 Secrets To Websites That Sell By Alex Nelson Website Secret #1 Create a Direct Response Website Did you know there are two different types of websites? It s true. There are branding websites and there

KEY GUIDE. Financial protection for you and your family

KEY GUIDE Financial protection for you and your family Protecting what matters most Life and health insurance protection underpins most good financial planning. These types of insurance can ensure that

KEY GUIDE Financial protection for you and your family Protecting what matters most Life and health insurance protection underpins most good financial planning. These types of insurance can ensure that

Gains on foreign life insurance policies

Helpsheet 321 Tax year 6 April 2013 to 5 April 2014 Gains on foreign life insurance policies A Contacts Introduction Page 2 Part 1 Types of policy Page 3 What sort of policy do you have? Page 3 When will

Helpsheet 321 Tax year 6 April 2013 to 5 April 2014 Gains on foreign life insurance policies A Contacts Introduction Page 2 Part 1 Types of policy Page 3 What sort of policy do you have? Page 3 When will

Income Protection. The Income Protection Market - Opportunity? Karen Gallagher Business Development Manager

Karen Gallagher Business Development Manager The Market - Opportunity? Only 12% to 15% of the working population have cover Majority of people in Ireland are still in employment Current consumer sentiment

Karen Gallagher Business Development Manager The Market - Opportunity? Only 12% to 15% of the working population have cover Majority of people in Ireland are still in employment Current consumer sentiment

Welcome to Pre Licensing!

Welcome to Pre Licensing! Your Primerica pre licensing experience is about to begin, and we encourage you to keep this guide handy as you go through the process. Thousands of people just like you have

Welcome to Pre Licensing! Your Primerica pre licensing experience is about to begin, and we encourage you to keep this guide handy as you go through the process. Thousands of people just like you have

Get to know your options for protecting yourself and your family

Get to know your options for protecting yourself and your family LifeProtect Guide Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of

Get to know your options for protecting yourself and your family LifeProtect Guide Allow us to introduce ourselves. We are Zurich. We are part of a global insurance group with Swiss roots. We are one of

Actuarial Funding Tushar Falodia & Surajit Basu

Actuarial Funding Tushar Falodia & Surajit Basu Ibexi Solutions Page 1 Table of Contents Executive Summary...3 About the Authors...3 Introduction...4 Insurance Concepts...5 Traditional products...5 Unit-linked

Actuarial Funding Tushar Falodia & Surajit Basu Ibexi Solutions Page 1 Table of Contents Executive Summary...3 About the Authors...3 Introduction...4 Insurance Concepts...5 Traditional products...5 Unit-linked

he Ultimate Baby Boomers Guide to Life Insurance

The Ultimate Baby Boomers Guide to Life Insurance he Ultimate Baby Boomers Guide to Life Insurance Contents Life Insurance Quotes for Baby Boomers- 3 Our Best Advice How the New Living Benefits Riders

The Ultimate Baby Boomers Guide to Life Insurance he Ultimate Baby Boomers Guide to Life Insurance Contents Life Insurance Quotes for Baby Boomers- 3 Our Best Advice How the New Living Benefits Riders

Life Insurance. Nationwide and the Nationwide Frame are federally registered service marks of Nationwide Mutual Insurance Company.

Life Insurance Nationwide and the Nationwide Frame are federally registered service marks of Nationwide Mutual Insurance Company. Facilitator s Guide Life Insurance Overview: If you ask people to name

Life Insurance Nationwide and the Nationwide Frame are federally registered service marks of Nationwide Mutual Insurance Company. Facilitator s Guide Life Insurance Overview: If you ask people to name

Types of life insurance Buying life insurance How cancer can affect buying life insurance Getting money early from life insurance

This information is an extract from the booklet Insurance, which is part of the financial guidance series. You may find the full booklet helpful. We can send you a free copy see page 6. Contents Types

This information is an extract from the booklet Insurance, which is part of the financial guidance series. You may find the full booklet helpful. We can send you a free copy see page 6. Contents Types

A CONSUMER GUIDE TO LIFE SETTLEMENTS

A CONSUMER GUIDE TO LIFE SETTLEMENTS Open Life Settlements 866.877.4054 Maximizing the Value of Your Life Policy Your unwanted life insurance policy can be an incredible asset. Open Life Settlements can

A CONSUMER GUIDE TO LIFE SETTLEMENTS Open Life Settlements 866.877.4054 Maximizing the Value of Your Life Policy Your unwanted life insurance policy can be an incredible asset. Open Life Settlements can