Uncertainty and Insurance

|

|

|

- Donna Burke

- 10 years ago

- Views:

Transcription

1 Uncertainty and Insurance A risk averse consumer is willing to pay for insurance. If consumption levels are 100, 200 and 400, with probabilities 1/6, 1/2, 1/3, respectively, then expected value of cons. = (100/6)+(200/2)+(400/3) = 250. Actuarially fair insurance: Insurer's expected net payout = 0. Offered actuarially fair insurance, risk averse consumer insures fully (completely removes uncertainty) replaces uncertain consumption in example by sure 250. Certainty equivalent of the risky consumption is the sure consumption that the consumer considers just as good. For risk averse consumer certainty equivalent < expected consumption since certainty equivalent is just as good as risky consumption, but getting the expected consumption for sure is better.

replaces uncertain consumption in example by sure 250.")

2 Uncertainty and Insurance Insurer offering actuarially fair insurance gets expected payout equal to sure premium received, so expected net revenue =0. Private insurers charge higher premium to cover costs + profit. With premium higher than actuarially fair, rational risk averse consumers buy less than full insurance, accept some risk (insurance with deductible). Private vs public insurance. Benefits of private: flexibility; match product to preferences; competition tends to lower costs. Benefits of public: fixed costs spread over bigger population. Potential inefficiencies from asymmetric information. Insurance buyers know more about their risks than insurers. Riskier people more likely to buy, so buyers are more risky than ave. Insurers raise premium, more low risk people drop out making customer pool riskier: Death spiral (CA health ins)

3 Adverse Selection and Moral Hazard Insurance buyers know more about their risks than insurers do. Adverse selection from hidden info about trader's characteristics Inefficiency from externality: riskier buyer imposes costs on insurers and other buyers. Lose mutually beneficial trades. Second kind of asymmetric info: Moral hazard Economists' definition: hidden action affecting insurer's costs. Example: with unemployment insurance, don't look hard for job. Insurers' definition: buyer's actions (hidden or not) affecting insurer's costs. Example: people with health insurance getting more treatment. With low transaction costs, only hidden action moral hazard causes inefficiency. (First welfare theorem: distinguish goods by the situation in which they are produced or consumed.)

affecting insurer's costs. Example: people with health insurance getting more treatment.")

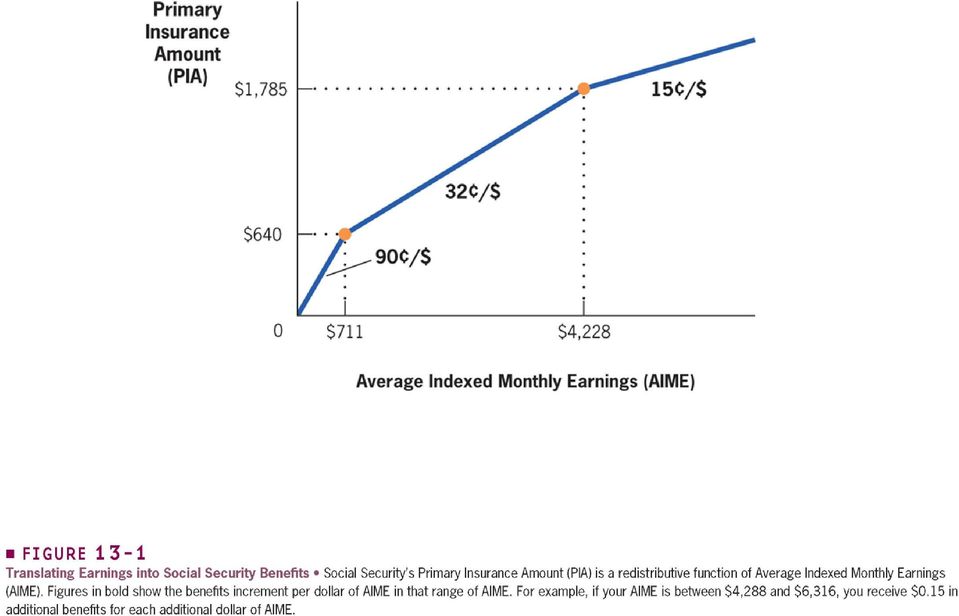

4 Social Security (SS) Pension System SS is Old Age, Survivors and Disability Insurance, OASDI. Annuity: buyer pays initially, gets periodic payment until death. After death, SS pays spouse and children up to age 18. US SS since 1935; first benefit 1940; after 1939 pay-as-you-go PAYGO current workers' payroll tax pays for benefits to retirees. Since 1983, partially funded: part of tax goes to SS Trust. Payroll tax 12.4% of earnings up to $106,800 cap in 2011, half paid by worker, half by employer ($'s inflation adjusted) Can start benefit at age 62 if paid tax in 40 quarters. Benefit depends on retirement age and 35 yr average indexed monthly earnings (AIME). Retire at 65, get (90% of first $744 of AIME) + (32% of AIME btw $744 and $4483) + (15% of rest of AIME). Get highest expected value retiring at age 67.

Can start benefit at age 62 if paid tax in 40 quarters.")

5

6 Social Security (SS) Pension System Retirees who stopped working long ago earned low wages since they worked long ago. SS formula for AIME adjusts for that. Example: A worker earned $10000 in 1974 and retired in The average wage was $8000 in 1974 and $37000 in 2005 so the worker's adjusted 1974 wage is $10000 x (37000/8000) $ AIME is the average of the worker's adjusted wages over the 35 yrs of highest adjusted wages. AIME raises early wages by more than an adjustment for inflation since wages grew faster than inflation.

7 Social Security (SS) Pension System Distribution of net benefits: See Gruber table SS favors early generations, low earners, women (longer lives), single-earner couples. Ave 1994 retiree gets 2% annual return SS less progressive than benefit formula: rich live longer. Later cohorts' lower return repays legacy debt of early cohorts. Private alternatives: personal saving (no ins); employer pension (bankruptcy risk); annuity (cost > 2.3 actuarially fair rate). Employer pension pools employee risks (less adverse selection); contributions tax free. Most pensions defined contribution: benefits based on market returns on specified contributions. SS is defined benefit: benefit according to formula. SS Trust Fund projected to run out by 2040 (probably sooner). This yr Trust Fund will shrink. PAYGO after it runs out.

; contributions tax free. Most pensions defined contribution: benefits based on market returns on specified contributions.")

8 Social Security (SS) Effects Labor Supply: Many retire at earliest age for SS benefits; many more retire at full benefit age, maximizing expected benefits. Some workers delay retiring to get bigger benefit; probably more retire earlier than if there was no SS; so labor supply falls, maybe not much: without SS few fulltime workers past age 70. Personal Saving. Effect of SS depends on reasons for saving. 1. Saving for retirement: If SS pays same "rate of return" (benefits as return on tax payments) as private market, then consumer chooses same consumption as without SS, so personal saving is reduced by the amount of the payroll tax (100% crowd-out of saving). Personal saving averages around 8% of income. Payroll tax is 12.4% of taxed earnings (about 65% of total income), so the tax is around 7% of total income; Model estimate: SS cuts saving by 45% (from 15% to 8%).

as private market, then consumer chooses same consumption as without SS, so personal saving is reduced by")

9 Social Security (SS) Effects 2. Precautionary saving (saving for unexpected expenses): This motive remains with SS. Payroll tax reduces disposable income, so precautionary saving falls, but not by $1 for each $1 of payroll tax. Saving falls less than in case Altruism: Higher SS benefit and tax transfers wealth from younger to older generation. A saver who cares about heirs' welfare and wants to give them gifts or bequest, continues to save in order to undo the effect of the wealth transfer. Probably the first two motives are more common, so SS probably reduces personal saving and capital accumulation. Because of motives 2 and 3, the amount of saving reduction is probably less than 45%. Quasiexperimental studies in US and Italy suggest saving reduction in the range from 15% to 40%.

10 Social Security (SS) Sustainability In PAYGO after 2040, benefit/ave wage falls or tax rises, or both. N=# workers, R= # retirees, t= tax rate, B= benefit, W= ave wage tnw = BR, tn/r = B/W = ave replacement rate 40% now. N/R 3.3 now, expected to fall to 2.1 in More retirees per worker: longer lifetimes, baby boom retirees. If B/W constant, t rises to 19%; if t constant, B/W falls to 26%. Proposals: 1. Remove payroll tax income cap; raise Full Benefits Age (with highest expected SS benefit) to 69; raise payroll tax rate 2.5% points. 2. Use consumer price index instead of wage index to adjust lifetime wages in AIME formula (lowers long run B/W to 23%). 3. Allow more immigration by young adults; plus other reforms.

to 69; raise payroll tax rate 2.")

11 Social Security (SS) Reform Proposal 4. (Feldstein, Samwick) Privatization: Raise payroll tax to 17%, part goes in private retirement account (PRA) managed by worker, rest pays benefits of current retirees. Return from PRA finances younger workers' retirement. Need historical ave annual stock return, 7%. But stocks are risky. Workers with low returns get low retirement income. Proposal could reduce stock returns: stock prices rise as baby boom generations buy stock; stock prices lower than otherwise as baby boomers sell stock to finance retirement. Interest rates likely higher than otherwise to attract buyers of gov bonds previously held by SS Trust fund. Private annuities market adverse selection problem remains. Workers can buy annuities to insure against low income when very old, but premium is much higher than actuarially fair.

12 Social Security (SS): Efficiency Issues Advantages of gov pension: 1. Dynamic efficiency? Growing population funds same consumption with less saving. 2. Adverse selection limits private market for annuities. 3. Administrative + decision-making economies from big standardized program. (Admin cost 0.2% of assets) 4. Some people don't plan well. In experiments, pension choice depends on framing of alternatives. (Paternalism) Bernheim, et. al. American Economic Review 2001, Disadvantages of gov system: 1. Lower saving can reduce capital accumulation and growth. 2. Less flexibility, poorer matching to preferences. 3. Funded saving can earn higher (riskier) expected return; unlikely to be as high as predicted by Feldstein, Samwick.

Notes - Gruber, Public Finance Chapter 13 - Social Security Social Security started in 1935 in Great Depression. Asset values had fallen drastically,

Notes - Gruber, Public Finance Chapter 13 - Social Security Social Security started in 1935 in Great Depression. Asset values had fallen drastically, many elderly lost their lifetime savings. Workers pay

Notes - Gruber, Public Finance Chapter 13 - Social Security Social Security started in 1935 in Great Depression. Asset values had fallen drastically, many elderly lost their lifetime savings. Workers pay

Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care?

averaged 7%, lower than 15% OECD average. Why? Why do we care?") Taxation and Personal Saving, G 22 Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care? Efficiency issues 1. Negative consumption

Taxation and Personal Saving, G 22 Since 1960's, U.S. personal savings rate (fraction of income saved) averaged 7%, lower than 15% OECD average. Why? Why do we care? Efficiency issues 1. Negative consumption

Social Insurance (Chapter-12) Part-1

Part-1") (Chapter-12) Part-1 Background Dramatic change in the composition of government spending in the U.S. over time Background Social insurance programs: Government interventions in the provision of insurance

(Chapter-12) Part-1 Background Dramatic change in the composition of government spending in the U.S. over time Background Social insurance programs: Government interventions in the provision of insurance

1%(5:25.,1*3$3(56(5,(6 $//2&$7,1*3$<52//7$;5(9(18(72 3(5621$/5(7,5(0(17$&&28176720$,17$,1 62&,$/6(&85,7<%(1(),76$1'7+(3$<52//7$;5$7(

,76$1'7+(3$<52//7$;5$7(") 1%(5:25.,1*3$3(56(5,(6 $//2&$7,1*3$

1%(5:25.,1*3$3(56(5,(6 $//2&$7,1*3$

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

Life Guide Retirement and Social Security

Life Guide Retirement and Social Security The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check

Life Guide Retirement and Social Security The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check

Retirement Payouts and Risks Involved

Retirement Payouts and Risks Involved IOPS OECD Global Forum, Beijing, 14-15 November 2007 Financial Affairs Division, OECD 1 Structure Different types of payout options Lump-sum (pros and cons) Programmed

Retirement Payouts and Risks Involved IOPS OECD Global Forum, Beijing, 14-15 November 2007 Financial Affairs Division, OECD 1 Structure Different types of payout options Lump-sum (pros and cons) Programmed

Notes - Gruber, Public Finance Chapter 20.3 A calculation that finds the optimal income tax in a simple model: Gruber and Saez (2002).

.") Notes - Gruber, Public Finance Chapter 20.3 A calculation that finds the optimal income tax in a simple model: Gruber and Saez (2002). Description of the model. This is a special case of a Mirrlees model.

Notes - Gruber, Public Finance Chapter 20.3 A calculation that finds the optimal income tax in a simple model: Gruber and Saez (2002). Description of the model. This is a special case of a Mirrlees model.

Aon Consulting s 2008 Replacement Ratio Study. A Measurement Tool For Retirement Planning

Aon Consulting s 2008 Replacement Ratio Study A Measurement Tool For Retirement Planning A Measurement Tool for Retirement Planning For twenty years, Aon Consulting and Georgia State University have published

Aon Consulting s 2008 Replacement Ratio Study A Measurement Tool For Retirement Planning A Measurement Tool for Retirement Planning For twenty years, Aon Consulting and Georgia State University have published

CREATE TAX ADVANTAGED RETIREMENT INCOME YOU CAN T OUTLIVE. create tax advantaged retirement income you can t outlive

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

Moral Hazard and Adverse Selection. Topic 6

Moral Hazard and Adverse Selection Topic 6 Outline 1. Government as a Provider of Insurance. 2. Adverse Selection and the Supply of Insurance. 3. Moral Hazard. 4. Moral Hazard and Incentives in Organizations.

Moral Hazard and Adverse Selection Topic 6 Outline 1. Government as a Provider of Insurance. 2. Adverse Selection and the Supply of Insurance. 3. Moral Hazard. 4. Moral Hazard and Incentives in Organizations.

TRENDS AND ISSUES A PAYCHECK FOR LIFE: THE ROLE OF ANNUITIES IN YOUR RETIREMENT PORTFOLIO JUNE 2008

TRENDS AND ISSUES JUNE 2008 A PAYCHECK FOR LIFE: THE ROLE OF ANNUITIES IN YOUR RETIREMENT PORTFOLIO Jeffrey R. Brown William G. Karnes Professor of Finance, College of Business University of Illinois at

TRENDS AND ISSUES JUNE 2008 A PAYCHECK FOR LIFE: THE ROLE OF ANNUITIES IN YOUR RETIREMENT PORTFOLIO Jeffrey R. Brown William G. Karnes Professor of Finance, College of Business University of Illinois at

Maximizing Your Pension with Life Insurance

Maximizing Your Pension with Life Insurance Introduction If you participate in a traditional pension plan (known as a defined benefit plan) with your employer, you may receive monthly benefits from the

Maximizing Your Pension with Life Insurance Introduction If you participate in a traditional pension plan (known as a defined benefit plan) with your employer, you may receive monthly benefits from the

Annuity Principles and Concepts Session Five Lesson Two. Annuity (Benefit) Payment Options

Payment Options") Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

Annuities: Good, Not so Good, or Bad? Are They For You?

9-14 41 BRK-A Annuities: Good, Not so Good, or Bad? Are They For You? More often than not, it s clear that variable annuities always benefit the seller, and only infrequently benefit the buyer. -- Forbes

9-14 41 BRK-A Annuities: Good, Not so Good, or Bad? Are They For You? More often than not, it s clear that variable annuities always benefit the seller, and only infrequently benefit the buyer. -- Forbes

Notes - Gruber, Public Finance Section 12.1 Social Insurance What is insurance? Individuals pay money to an insurer (private firm or gov).

.") Notes - Gruber, Public Finance Section 12.1 Social Insurance What is insurance? Individuals pay money to an insurer (private firm or gov). These payments are called premiums. Insurer promises to make a

Notes - Gruber, Public Finance Section 12.1 Social Insurance What is insurance? Individuals pay money to an insurer (private firm or gov). These payments are called premiums. Insurer promises to make a

Contents: What is an Annuity?

Contents: What is an Annuity? When might I need an annuity policy? Types of annuities Pension annuities Annuity income options Enhanced and Lifestyle annuities Impaired Life annuities Annuity rates FAQs

Contents: What is an Annuity? When might I need an annuity policy? Types of annuities Pension annuities Annuity income options Enhanced and Lifestyle annuities Impaired Life annuities Annuity rates FAQs

Annuities: Good, Not so Good, or Bad? (Another Free InvestEd Webinar)

") Annuities: Good, Not so Good, or Bad? (Another Free InvestEd Webinar) Bob Adams 2013 B. Adams 4 Annuities: Good, Not so Good, or Bad? Are They For You? More often than not, it s clear that variable annuities

Annuities: Good, Not so Good, or Bad? (Another Free InvestEd Webinar) Bob Adams 2013 B. Adams 4 Annuities: Good, Not so Good, or Bad? Are They For You? More often than not, it s clear that variable annuities

China's Social Security Pension System and its Reform

China's Pension Reform China's Social Security Pension System and its Reform Kaiji Chen University of Oslo March 27, 2007 1 China's Pension Reform Why should we care about China's social security system

China's Pension Reform China's Social Security Pension System and its Reform Kaiji Chen University of Oslo March 27, 2007 1 China's Pension Reform Why should we care about China's social security system

How to Secure Your Family and Help Vulnerable Children! A BRIEF E-BOOK FROM FH LEGACY

How to Secure Your Family and Help Vulnerable Children! A BRIEF E-BOOK FROM FH LEGACY 01 Does This Describe You? My high productivity, best-earning years are winding down. I forsee an increasing need to

How to Secure Your Family and Help Vulnerable Children! A BRIEF E-BOOK FROM FH LEGACY 01 Does This Describe You? My high productivity, best-earning years are winding down. I forsee an increasing need to

Understanding Annuities: A Lesson in Annuities

Understanding Annuities: A Lesson in Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that you

Understanding Annuities: A Lesson in Annuities Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to guarantee a retirement income that you

Social Security Retirement Parman R. Green, MU Extension Ag Business Mgmt. Specialist

Social Security Retirement Parman R. Green, MU Extension Ag Business Mgmt. Specialist Farmers and many other self-employed business owners who report income on the cash-basis have a tremendous amount of

Social Security Retirement Parman R. Green, MU Extension Ag Business Mgmt. Specialist Farmers and many other self-employed business owners who report income on the cash-basis have a tremendous amount of

Efficient Retirement Design Combining Private Assets and Social Security to Maximize Retirement Resources. March 2013

Efficient Retirement Design Combining Private Assets and Social Security to Maximize Retirement Resources John B. Shoven Stanford University Sita N. Slavov American Enterprise Institute March 2013 Executive

Efficient Retirement Design Combining Private Assets and Social Security to Maximize Retirement Resources John B. Shoven Stanford University Sita N. Slavov American Enterprise Institute March 2013 Executive

Cash value accumulation life insurance

Protection, wealth accumulation, and tax benefits all in one policy Cash value accumulation life insurance Allianz Life Insurance Company of North America M-5249 Page 1 of 12 Uncertainty in life is the

Protection, wealth accumulation, and tax benefits all in one policy Cash value accumulation life insurance Allianz Life Insurance Company of North America M-5249 Page 1 of 12 Uncertainty in life is the

SIEPR policy brief. Efficient Retirement Design. By John B. Shoven. About The Author. Stanford University March 2013

Stanford University March 2013 Stanford Institute for Economic Policy Research on the web: http://siepr.stanford.edu Efficient Retirement Design By John B. Shoven The pension system in the U.S. has changed

Stanford University March 2013 Stanford Institute for Economic Policy Research on the web: http://siepr.stanford.edu Efficient Retirement Design By John B. Shoven The pension system in the U.S. has changed

Pacific. Income Provider. A Single-Premium, Immediate Fixed Annuity for a Confident Retirement. Client Guide 9/15 80002-15A

Pacific Income Provider A Single-Premium, Immediate Fixed Annuity for a Confident Retirement 9/15 80002-15A Client Guide Why Pacific Life Pacific Life has more than 145 years of experience, and we remain

Pacific Income Provider A Single-Premium, Immediate Fixed Annuity for a Confident Retirement 9/15 80002-15A Client Guide Why Pacific Life Pacific Life has more than 145 years of experience, and we remain

Macroeconomic and Distributional Effects of Social Security

Macroeconomic and Distributional Effects of Social Security Luisa Fuster 1 Universitat Pompeu Fabra and University of Toronto First draft: September 2002. This version: December 2002 1. Introduction Social

Macroeconomic and Distributional Effects of Social Security Luisa Fuster 1 Universitat Pompeu Fabra and University of Toronto First draft: September 2002. This version: December 2002 1. Introduction Social

for INCOME IN USING YOUR HOUSE RETIREMENT A retirement PLANNING GUIDE

A retirement PLANNING GUIDE USING YOUR HOUSE for INCOME IN RETIREMENT It s something Americans increasingly need to consider. And increasingly need to do. A retirement PLANNING GUIDE By Steven Sass, Alicia

A retirement PLANNING GUIDE USING YOUR HOUSE for INCOME IN RETIREMENT It s something Americans increasingly need to consider. And increasingly need to do. A retirement PLANNING GUIDE By Steven Sass, Alicia

Standard 6: The student will explain and evaluate the importance of planning for retirement.

TEACHER GUIDE 6.1 RETIREMENT PLANNING PAGE 1 Standard 6: The student will explain and evaluate the importance of planning for retirement. Planning for Your Retirement Priority Academic Student Skills Personal

TEACHER GUIDE 6.1 RETIREMENT PLANNING PAGE 1 Standard 6: The student will explain and evaluate the importance of planning for retirement. Planning for Your Retirement Priority Academic Student Skills Personal

The Individual Annuity

The Individual Annuity a re s o u rc e i n yo u r r e t i r e m e n t an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live

The Individual Annuity a re s o u rc e i n yo u r r e t i r e m e n t an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live

Composition of Farm Household Income and Wealth

Composition of Farm Household Income and Wealth Today it is rare for any household to receive all of its from a single source. Even when only one household member is employed, it is possible to earn from

Composition of Farm Household Income and Wealth Today it is rare for any household to receive all of its from a single source. Even when only one household member is employed, it is possible to earn from

Understanding Your Life Insurance Options

Understanding Your Life Insurance Options Designed for: Marathonbenefits.com Designed by: Marathon Benefit Corp. Ph: 403-238-7343 [email protected] September 17, 2010 U N D E R S T A N D I N G

Understanding Your Life Insurance Options Designed for: Marathonbenefits.com Designed by: Marathon Benefit Corp. Ph: 403-238-7343 [email protected] September 17, 2010 U N D E R S T A N D I N G

A Guide to Planning for Retirement INVESTMENT BASICS SERIES

A Guide to Planning for Retirement INVESTMENT BASICS SERIES It s Never Too Early to Start What You Need to Know About Saving for Retirement Most of us don t realize how much time we may spend in retirement.

A Guide to Planning for Retirement INVESTMENT BASICS SERIES It s Never Too Early to Start What You Need to Know About Saving for Retirement Most of us don t realize how much time we may spend in retirement.

Retirement Income Investment Strategy by Andrew J. Krosnowski

Retirement Income Investment Strategy by Andrew J. Krosnowski Step 1- Income Needs-When formulating a successful strategy to generate income during retirement we feel that it is important to start by identifying

Retirement Income Investment Strategy by Andrew J. Krosnowski Step 1- Income Needs-When formulating a successful strategy to generate income during retirement we feel that it is important to start by identifying

Understanding annuities

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

CASE District IV Conference Fort Worth, Texas. March 25, 2013. What true assets does your family possess?

HOW TO INITIATE GIFT PLANNING DISCUSSIONS WITH DONORS The Charitable Planning Process CASE District IV Conference Fort Worth, Texas March 25, 2013 Laura Hansen Dean, J.D. Attorney at Law (Texas, Indiana)

HOW TO INITIATE GIFT PLANNING DISCUSSIONS WITH DONORS The Charitable Planning Process CASE District IV Conference Fort Worth, Texas March 25, 2013 Laura Hansen Dean, J.D. Attorney at Law (Texas, Indiana)

Planning for Your Retirement

STUDENT MODULE 6.1 RETIREMENT PLANNING PAGE 1 Standard 6: The student will explain and evaluate the importance of planning for retirement. Planning for Your Retirement Lindzi and Lezli will attend retirement

STUDENT MODULE 6.1 RETIREMENT PLANNING PAGE 1 Standard 6: The student will explain and evaluate the importance of planning for retirement. Planning for Your Retirement Lindzi and Lezli will attend retirement

Life Insurance and Annuity Buyer s Guide

Life Insurance and Annuity Buyer s Guide Published by the Kentucky Office of Insurance Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as

Life Insurance and Annuity Buyer s Guide Published by the Kentucky Office of Insurance Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as

The Individual Annuity

The Individual Annuity a resource in your retirement an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live 20 to 30 years

The Individual Annuity a resource in your retirement an age of Decision Retirement today requires more planning than for previous generations. Americans are living longer many will live 20 to 30 years

Understanding annuities

Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Helping to protect your retirement income security from life s uncertainties. The retirement

Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Helping to protect your retirement income security from life s uncertainties. The retirement

Understanding Annuities: A Lesson in Fixed Interest and Indexed Annuities Prepared for: Your Clients

Understanding Annuities: A Lesson in Fixed Interest and Indexed Annuities Prepared for: Your Clients Presented by: Arvin D. Pfefer Arvin D. Pfefer & Associates 7301 Mission Road, Suite 241 Prairie Village,

Understanding Annuities: A Lesson in Fixed Interest and Indexed Annuities Prepared for: Your Clients Presented by: Arvin D. Pfefer Arvin D. Pfefer & Associates 7301 Mission Road, Suite 241 Prairie Village,

Understanding fixed index universal life insurance

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation potential, and tax advantages in one policy M-3959 Understanding fixed

Allianz Life Insurance Company of North America Understanding fixed index universal life insurance Protection, wealth accumulation potential, and tax advantages in one policy M-3959 Understanding fixed

Excerpts from IRI Annuity Fact Book Variable Annuity 101 An annuity is often viewed as life insurance in reverse. Whereas life insurance protects an individual against premature death, an annuity protects

Excerpts from IRI Annuity Fact Book Variable Annuity 101 An annuity is often viewed as life insurance in reverse. Whereas life insurance protects an individual against premature death, an annuity protects

Issued by Fidelity & Guaranty Life Insurance Company, Baltimore, MD Distributed by Legacy Marketing Group

Issued by Fidelity & Guaranty Life Insurance Company, Baltimore, MD Distributed by Legacy Marketing Group Choices To Plan for the Long Term The financial challenges you face evolve with economic and life

Issued by Fidelity & Guaranty Life Insurance Company, Baltimore, MD Distributed by Legacy Marketing Group Choices To Plan for the Long Term The financial challenges you face evolve with economic and life

Designing a Monthly Paycheck for Retirement MANAGING RETIREMENT DECISIONS SERIES

Designing a Monthly Paycheck for Retirement MANAGING RETIREMENT DECISIONS SERIES WHERE S MY PAYCHECK? That is a common question for new retirees and near-retirees when they start mapping out the retirement

Designing a Monthly Paycheck for Retirement MANAGING RETIREMENT DECISIONS SERIES WHERE S MY PAYCHECK? That is a common question for new retirees and near-retirees when they start mapping out the retirement

Part VII Individual Retirement Accounts

Part VII are a retirement planning tool that virtually everyone should consider. The new IRA options also have made selecting an IRA a bit more complicated. IRA Basics The Traditional IRA is an Individual

Part VII are a retirement planning tool that virtually everyone should consider. The new IRA options also have made selecting an IRA a bit more complicated. IRA Basics The Traditional IRA is an Individual

An Adviser s Guide to Pensions

An Adviser s Guide to Pensions 1 An Adviser s Guide to Pensions Contents: Section 1: Personal Pensions 1.1 Eligibility 1.2 Maximum Benefits 1.3 Contributions & Tax Relief 1.4 Death Benefits 1.5 Retirement

An Adviser s Guide to Pensions 1 An Adviser s Guide to Pensions Contents: Section 1: Personal Pensions 1.1 Eligibility 1.2 Maximum Benefits 1.3 Contributions & Tax Relief 1.4 Death Benefits 1.5 Retirement

The Effective Use of Reverse Mortgages in Retirement

Page 1 of 8 Copyright 2009, Society of Financial Service Professionals All rights reserved. Journal of Financial Service Professionals July 2009 The Effective Use of Reverse Mortgages in Retirement by

Page 1 of 8 Copyright 2009, Society of Financial Service Professionals All rights reserved. Journal of Financial Service Professionals July 2009 The Effective Use of Reverse Mortgages in Retirement by

When to Claim Social Security Retirement Benefits

When to Claim Social Security Retirement Benefits David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management January 10, 2013 Morningstar Investment Management Abstract Social

When to Claim Social Security Retirement Benefits David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management January 10, 2013 Morningstar Investment Management Abstract Social

Wealth Strategies. www.rfawealth.com. Saving For Retirement: Tax Deductible vs Roth Contributions. www.rfawealth.com

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU Contents 1 Give and you shall receive 3 Techniques summary 5 Planning for charitable giving NOT FDIC OR NCUA INSURED NOT

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU Contents 1 Give and you shall receive 3 Techniques summary 5 Planning for charitable giving NOT FDIC OR NCUA INSURED NOT

Should I Buy an Income Annuity?

Prepared For: Fred & Wilma FLINT Prepared By: Don Maycock The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off

Prepared For: Fred & Wilma FLINT Prepared By: Don Maycock The purchase of any financial product involves a trade off. For example when saving for retirement, you are often faced with making a trade off

Longevity insurance annuities are deferred annuities that. Longevity Insurance Annuities in 401(k) Plans and IRAs. article Retirement

Plans and IRAs. article Retirement") article Retirement Longevity Insurance Annuities in 401(k) Plans and IRAs What role should longevity insurance annuities play in 401(k) plans? This article addresses the question of whether participants,

article Retirement Longevity Insurance Annuities in 401(k) Plans and IRAs What role should longevity insurance annuities play in 401(k) plans? This article addresses the question of whether participants,

Delayed Income Annuities / Longevity Insurance. Presented By: Scott White, AAPA, ALMI Annuity Marketing Manager

Delayed Income Annuities / Longevity Insurance Presented By: Scott White, AAPA, ALMI Annuity Marketing Manager CPS Overview Founded in 1974 The Largest Independently-Owned Wholesaler of Life, Long Term

Delayed Income Annuities / Longevity Insurance Presented By: Scott White, AAPA, ALMI Annuity Marketing Manager CPS Overview Founded in 1974 The Largest Independently-Owned Wholesaler of Life, Long Term

Your pension benefit options

2 Your pension benefit options Traditional pension plans generally provide the option of a lump-sum payment or a fixed monthly payment for life through an annuity. The fixed monthly payment amount is usually

2 Your pension benefit options Traditional pension plans generally provide the option of a lump-sum payment or a fixed monthly payment for life through an annuity. The fixed monthly payment amount is usually

BUYER'S GUIDE TO EQUITY-INDEXED ANNUITIES WHAT ARE THE DIFFERENT KINDS OF ANNUITY CONTRACTS?

BUYER'S GUIDE TO EQUITY-INDEXED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

BUYER'S GUIDE TO EQUITY-INDEXED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

Fixed Deferred Annuities

Buyer Buyer s Guide to: s Guide to: Fixed Deferred Annuities Prepared by the Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

Buyer Buyer s Guide to: s Guide to: Fixed Deferred Annuities Prepared by the Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association

Zero Estate Tax Strategy

Zero Estate Tax Strategy AN PLANNING STRATEGY USING LIFE INSURANCE, A FOUNDATION, AND WEALTH REPLACEMENT TRUST The Prudential Insurance Company of America 0257697 0257697-00003-00 Ed. 07/2015 Exp. 01/20/2017

Zero Estate Tax Strategy AN PLANNING STRATEGY USING LIFE INSURANCE, A FOUNDATION, AND WEALTH REPLACEMENT TRUST The Prudential Insurance Company of America 0257697 0257697-00003-00 Ed. 07/2015 Exp. 01/20/2017

Social Security Fundamentals

Social Security Fundamentals Guidelines for making well-informed decisions There s Wealth in Our Approach. When it comes to thinking about the part Social Security plays in your retirement plan, most of

Social Security Fundamentals Guidelines for making well-informed decisions There s Wealth in Our Approach. When it comes to thinking about the part Social Security plays in your retirement plan, most of

2 Fundamentals of Employee Benefit Programs

PART ONE OVERVIEW 2 Fundamentals of Employee Benefit Programs CHAPTER 1 EMPLOYEE BENEFITS IN THE UNITED STATES: AN INTRODUCTION Employee benefits are intended to promote economic security by insuring against

PART ONE OVERVIEW 2 Fundamentals of Employee Benefit Programs CHAPTER 1 EMPLOYEE BENEFITS IN THE UNITED STATES: AN INTRODUCTION Employee benefits are intended to promote economic security by insuring against

Retirement and Estate Planning

6P A R T Retirement and Estate Planning Should you invest in a retirement plan? Chapter 19 Retirement Planning Chapter 20 Estate Planning How much should you contribute to your retirement plan? How should

6P A R T Retirement and Estate Planning Should you invest in a retirement plan? Chapter 19 Retirement Planning Chapter 20 Estate Planning How much should you contribute to your retirement plan? How should

2012 HOUSEHOLD FINANCIAL PLANNING SURVEY

2012 HOUSEHOLD FINANCIAL PLANNING SURVEY A Summary of Key Findings July 23, 2012 Prepared for: Certified Financial Planner Board of Standards, Inc. and the Consumer Federation of America Prepared by: Princeton

2012 HOUSEHOLD FINANCIAL PLANNING SURVEY A Summary of Key Findings July 23, 2012 Prepared for: Certified Financial Planner Board of Standards, Inc. and the Consumer Federation of America Prepared by: Princeton

Retirement Income White Paper Insights Presentation

Retirement Income White Paper Insights Presentation Alun Stevens Jack Ding Nathan Bonarius Agenda Background Preliminary projections What are the risks? What are the possible solutions? Purpose of presentation

Retirement Income White Paper Insights Presentation Alun Stevens Jack Ding Nathan Bonarius Agenda Background Preliminary projections What are the risks? What are the possible solutions? Purpose of presentation

> The Role of Insurance in Wealth Planning

> The Role of Insurance in Wealth Planning Executive retirement solutions A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Executive retirement solutions Everyone wants enough retirement

> The Role of Insurance in Wealth Planning Executive retirement solutions A S S A N T E E S T A T E A N D I N S U R A N C E S E R V I C E S I N C. Executive retirement solutions Everyone wants enough retirement

Life Insurance and Annuity Buyer s Guide Introduction

Life Insurance and Annuity Buyer s Guide Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as an aid to assist you in determining your insurance

Life Insurance and Annuity Buyer s Guide Introduction The Kentucky Office of Insurance is pleased to offer this Life Insurance and Annuity Buyer s Guide as an aid to assist you in determining your insurance

BS2551 Money Banking and Finance. Institutional Investors

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

Survivorship Builder. An indexed survivorship life policy AS2000 (04-15)

") Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Survivorship Builder An indexed survivorship life policy AS2000 (04-15) Accordia Life believes in the essence of family. Your family may be a traditional one. It may be a group of people who care for

Experience Life. National Life Insurance Company. Liberty. Green Mountain Annuity Series. MK0813 (0209); LR 10139 (0209); Cat. No.

; LR 10139 (0209); Cat. No.") National Life Insurance Company Liberty Green Mountain Annuity Series MK0813 (0209); LR 10139 (0209); Cat. No. 61188 Experience Life National Life s Green Mountain Liberty Single Premium Tax-Deferred Annuity

National Life Insurance Company Liberty Green Mountain Annuity Series MK0813 (0209); LR 10139 (0209); Cat. No. 61188 Experience Life National Life s Green Mountain Liberty Single Premium Tax-Deferred Annuity

The Truth About Fixed Indexed Annuities

The Truth About Fixed Indexed Annuities Index annuities were first introduced in the United States nearly two decades ago. They were initially created as an alternative to mutual funds and variable annuities,

The Truth About Fixed Indexed Annuities Index annuities were first introduced in the United States nearly two decades ago. They were initially created as an alternative to mutual funds and variable annuities,

Evaluating the Advanced Life Deferred Annuity - An Annuity People Might Actually Buy

Evaluating the Advanced Life Deferred Annuity - An Annuity People Might Actually Buy Guan Gong and Anthony Webb Center for Retirement Research at Boston College Shanghai University of Finance and Economics

Evaluating the Advanced Life Deferred Annuity - An Annuity People Might Actually Buy Guan Gong and Anthony Webb Center for Retirement Research at Boston College Shanghai University of Finance and Economics

Performance Annuity. with Standard Life. Your guide to. Investment Solutions

Investment Solutions Your guide to Performance Annuity with Standard Life For insurance representative use only. This document is not intended for public distribution. title Hello. Performance Annuity:

Investment Solutions Your guide to Performance Annuity with Standard Life For insurance representative use only. This document is not intended for public distribution. title Hello. Performance Annuity:

Life Insurance Tutorial & Calculation Worksheet

Life Insurance Tutorial & Calculation Worksheet Provided By NAVY MUTUAL AID ASSOCIATION Henderson Hall, 29 Carpenter Road, Arlington, VA 22212 Telephone 800-628-6011-703-614-1638 - FAX 703-945-1441 E-mail:

Life Insurance Tutorial & Calculation Worksheet Provided By NAVY MUTUAL AID ASSOCIATION Henderson Hall, 29 Carpenter Road, Arlington, VA 22212 Telephone 800-628-6011-703-614-1638 - FAX 703-945-1441 E-mail:

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES Prepared by the National Association of Insurance Commissioners The National Association of Insurance Commissioners is an association of state insurance regulatory

Private annuity/trust

Deferring Capital Gains Taxes With A Private annuity/trust TM The National Association of Financial and Estate Planning NAFEP, 1999 and 2001 Revision 2 DEFERRAL OF CAPITAL GAINS AND DEPRECIATION RECAPTURE

Deferring Capital Gains Taxes With A Private annuity/trust TM The National Association of Financial and Estate Planning NAFEP, 1999 and 2001 Revision 2 DEFERRAL OF CAPITAL GAINS AND DEPRECIATION RECAPTURE

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES. The face page of the Fixed Deferred Annuity Buyer s Guide shall read as follows:

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES The face page of the Fixed Deferred Annuity Buyer s Guide shall read as follows: Prepared by the National Association of Insurance Commissioners The National Association

BUYER S GUIDE TO FIXED DEFERRED ANNUITIES The face page of the Fixed Deferred Annuity Buyer s Guide shall read as follows: Prepared by the National Association of Insurance Commissioners The National Association

PAYGO systems and their problems

A Global Perspective on Old Age Security Systems by Estelle James forthcoming in Encyclopedia of Global Studies, ed. H. Anheier, V. Faessel, M. Juergensmeyer. New York : Sage Publications, 2012 In pre-industrialized

A Global Perspective on Old Age Security Systems by Estelle James forthcoming in Encyclopedia of Global Studies, ed. H. Anheier, V. Faessel, M. Juergensmeyer. New York : Sage Publications, 2012 In pre-industrialized