Building Assets. of Foster Care. The Opportunity Passport : Findings from the Jim Casey Youth Opportunities Initiative June 2009

|

|

|

- Curtis Perkins

- 8 years ago

- Views:

Transcription

1 The Opportunity Passport : Building Assets for Youth Y Aging Out of Foster Care Findings from the Jim Casey Youth Opportunities Initiative June 2009 Opportunity Passport TM participants at the Youth Leadership Institute

2 The Jim Casey Youth Opportunities Initiative would like to thank our co-investment and grantee partners for all of their efforts. This brief will hopefully assist organizations in helping young people build assets and savings that support them in successfully transitioning to adulthood. In addition, the Initiative would like to give special thanks to Lynn Tiede, Jim Casey Youth Opportunities Initiative, and Fran Schorr, Metis Associates, who gave both heart and skill to the preparation of this brief. Cover photo by Lance Omar Thurman Photography Graphic Design by Tina Koenen Graphic Design, Inc.

3 Y outh aging out of foster care face many challenges. Often lacking the support of a permanent family, they must navigate this critical time in their lives with little guidance. It is not surprising that these young people, when compared to their peers from intact families, are less likely to have a high school diploma, are less likely to complete post-secondary education, and are more likely to become parents at a young age i. The Jim Casey Youth Opportunities Initiative (Initiative) focuses on improving the well-being of youth transitioning from foster care. The Initiative works with communities nationwide ii to help youth and young adults leaving foster care become successful, productive adults by helping reform the systems that support them. Initiative sites implement a broad set of strategies that include engaging young people, bringing together public and private partners, using data to drive decisions and galvanizing public support in order to improve policy and practice. Within this broader context of systems improvement, sites also implement a very focused strategy that offers young people the Opportunity Passport, the primary component of which is an Individual Development Account (IDA), or a matched savings account. The rationale for this matched savings account is that young people aging out of foster care do not often have the typical developmental experience of learning how to manage money, and leave care without even the basic financial and asset development skills that enable people to achieve economic success. A matched savings account can help participants learn financial management, obtain experience with the mainstream banking system, and save money for assets. Looking to apply best practices from the IDA field to this distinct population, the Initiative designed the Opportunity Passport for youth between the ages of 14 and 24 that have been in foster care on or after their 14th birthday. With the IDA, approved assets education expenses, vehicle, housing, investments, microenterprise and health care can be matched dollar for dollar, up to $1,000 per year based on the participant s savings. Saving for a vehicle purchase leads to dramatic changes in a young mother s life At 20 years old, Danielle Brunetta was out of foster care in San Diego, California. She was pregnant with her second child and struggling to maintain a part-time job. Danielle had owned a car, but it was totaled in an accident and she didn t have the means to replace it. I would try to get rides to and from work and child care. Every day was a struggle trying to figure it all out. Danielle became an Opportunity Passport participant and youth board member through Access, Inc., the Initiative s lead organization in San Diego. Very motivated to use the matched savings account to replace her car, Danielle saved and took the required asset-specific training. The training taught me how to shop around for cars, and avoid the lemons by getting a mechanic to look at the car first. I also learned about getting a loan with a good interest rate. The training was solid I really felt like I knew what I was doing when buying a car. After purchasing a vehicle with matched savings, Danielle was able to work full-time and decided to go to school in the evenings. With the help of the Opportunity Passport, I was able to purchase a car. I can now use my time more effectively, and tackle more tasks throughout the day. I ve maintained full-time employment, continued a college education, and I can still be home in time to read bedtime stories to my sons. That matters to me. When the Initiative began its work, we were not certain that young people aging out of foster care would and could take advantage of an IDA. We have now seen that they can and will. 2

4 Young people transitioning from foster care are saving and buying assets Over the past three years, we have seen consistent trends in these data The Initiative collects IDA-related data through a web-based system and outcome-related data from the Opportunity Passport Participant Survey completed by participants at the time they enroll (baseline) and then twice a year thereafter. Over the past three years, we have seen consistent trends in these data demonstrating that IDAs are an important resource utilized by young people transitioning from foster care. Data from Opportunity Passport participants show that those that have taken at least a baseline survey through October 2008 (baseline group, N=3052), are saving and purchasing assets at a similar rate as participants in the American Dream Demonstration (ADD). Opportunity Passport TM Participants Match Well Against the American Dream Demonstration (ADD) The Initiative 5.5 years iii ADD 5 years iv % with Matched Withdrawal 35% 32% Total $ Deposited $3,108,407 $2,530,538 Average Deposit per Participant $1,018 $1,070 Sample Size 3,052 participants in 10 sites 2,364 participants in 14 programs Indeed, the Opportunity Passport participants are achieving this despite being an average age of 18, compared to the average age of 36 for ADD participants. A developmentally appropriate IDA is key to success The emphasis on supporting youth in a developmentally appropriate way has grown in recent years, fueled by research on issues such as adolescent brain development and the typical trajectory that youth take toward adulthood. Research supports that older teenagers and young adults are truly in a transition period no longer a child, but not fully an adult. The bright line of becoming an adult at 18 or 19 years of age is fading, with growing consensus that the brain reaches maturity around age 25. 3

, are saving and purchasing assets at a similar")

5 The Opportunity Passport was developed specifically to meet these young people where they are and support them on their path toward adulthood. At this age, the assets that young people transitioning from an intact family accumulate are primarily their education, their early work experience, and their ability to live independently. The support that youth and young adults from intact families often receive is help with post-secondary education expenses, help purchasing a car which facilitates their ability to attend school and go to work and help with a deposit on their first apartment. Typically, these types of assets are not readily available to young people transitioning from foster care. Unlike other asset-building programs, the Opportunity Passport is unique in that participants can use their match dollars to purchase a vehicle, pay a deposit on an apartment, cover medical expenses, and procure investments, in addition to the more traditional IDA-approved assets of education expenses, purchase of a house, or microenterprise. Given these options, Opportunity Passport participants in the baseline group have most often purchased a car, followed by housing and education assets. Most housing purchases are for rent deposits, with a small number of young people purchasing homes, typically as they reach age 24. Housing: 24% (490) Based on 2,023 asset purchases by 1,077 youth Opportunity Passport TM Asset Purchases Education/Training: 21% (421) Investments: 9% (188) Medical/Dental: 3% (61) Microenterprise: 2% (35) Vehicle: 41% (828) Furthermore, almost one-half (46%) of asset purchasers have gone on to purchase another asset. In these cases, the assets purchased are most often some combination of a vehicle, housing, and education expenses. An IDA can meet the immediate needs of young people, while broader systems reforms occur Rob Hilla was 20 years old and out of Michigan's foster care system. He tried to get Medicaid coverage, but the Medicaid worker told him he wasn't eligible. I got denied services, said Hill, now 22 and a member of the Michigan Youth Opportunities Initiative youth board and Opportunity Passport participant. So instead, he used his matched savings account for braces a very typical need of youth and young adults and for other medical expenses. The experiences of Hilla and other young people aging out of foster care led Michigan to enact reforms to make sure that those leaving foster care have health insurance. It took two years, but Michigan extended Medicaid to youth until age 21. And in 2008, the state instituted another reform aimed at making it even easier for young people to get Medicaid coverage. They established a procedure to automatically enroll them, ensuring no gap in coverage through age 21. I m glad I was able to use my IDA for something that I really needed. The Opportunity Passport gave me something to fall back on, at a time when I didn t have any other options. 4

6 Despite this challenge, there are promising ways to support young people at all ages and stages of development to build their financial knowledge and experience. These data suggest that the matched savings account, while clearly no replacement for a family, is being utilized by participants in a developmentally appropriate way that facilitates a natural path toward economic success. The assets match the young people s interests and needs. We believe that these unique assets are motivating young people to take advantage of the IDA, and in the process they are connected to mainstream banking and acquiring real world experience with savings. Another developmentally appropriate way that we see youth using their IDAs is in the type of account activity. Not surprisingly, participants that purchase assets make more deposits than those that have not purchased an asset. However, asset purchasers also make more unmatched withdrawals (i.e., withdrawals for other reasons), while still managing to amass savings in order to reach their goal v. This indicates that they are practicing and developing new savings and money management behaviors. They are learning to save by struggling to save, which is not only typical behavior for young people, but for the population at large. In fact, for the past several years the personal savings rate in America has been negligible or negative. Youth and young adults must guide their involvement in asset development One of the core principles of the Initiative is the importance of the voice of youth and young adults in guiding the work. In practice, this occurs primarily through youth leadership boards and community boards that work in full partnership to create opportunities for, and advocate on behalf of, youth leaving foster care. However, the role of young people in guiding their own future has been further reinforced in sites experience implementing the Opportunity Passport. Not all young people are at the proper developmental stage to manage bank accounts or to save for long-term goals immediately following financial literacy training. Despite this challenge, there are promising ways to support young people at all ages and stages of development to build their financial knowledge and experience. Sites found that the financial literacy training provided a good foundation for young people, and introduced them to the potential of a matched savings account. But the training was not the only prerequisite to being ready to participate. Youth and young adults need to be motivated to have an IDA; they need a clear goal and plan for saving. Young people that do not feel ready should be engaged in other ways, such as being supported in planning for the future and goal setting, and being provided with real opportunities for earning income. But ultimately, it is the young person that should determine when he or she is ready to begin saving, a readiness that is not necessarily tied to age. 5

7 Even the most challenged young people are able to save and purchase assets All youth in and leaving foster care face serious challenges. However, we identified an interesting trend when examining findings from our longitudinal group (i.e., Opportunity Passport participants that took at least two surveys [N=1,936], a subset of the baseline group referred to earlier). We found that young people who report facing additional challenges, such as being a young parent, experiencing homelessness, or having no adult in their lives to turn to for support actually utilize the IDA proportionately more than others. % Young people who purchased at least one asset Even the Most Challenged Young People Can Save and Buy Assets No Permanent Adult Connection (N=165) Have been Homeless (N=563) All Participants (N=1,936) 0% 10% 20% 30% 40% 50% 60% 70% Based on young people who took at least two surveys We suspect that a higher level of need even survival is leading to the higher rate of utilization. That is, these young people need help to get a car, an apartment, help with school costs, etc., even more. And they are able to take advantage of the IDA to meet some of those needs, lacking the supports families typically provide. 49% (275) Parents (N=435) 46% (881) 58% (95) 57% (246) Early trends show that Opportunity Passport participants who report having a permanent adult in their lives are more likely to do better across outcome areas. An IDA is an important support but no replacement for a family The IDA is a resource that the Initiative believes has great potential for supporting this population, and the data indicate that young people transitioning from foster care can save and purchase assets when given access to matched savings accounts that meet their needs. That is promising. 6

8 An apartment, a car, a job, and a new lease on life Gina's old life was rocky and difficult. As one of six children of teen parents, Gina often was absent from school because she was the primary caregiver for her younger siblings. Her dad was in prison. "We didn't know where my mom was half the time," she says. Four of her six siblings were placed in foster care. Gina, 15 1/2 at the time, had dreams of going to law school and becoming a lawyer. Her first pregnancy shelved those plans. Still, she was determined not to follow the same path as her parents. Gina got involved with Bridging the Gap, a partnership between the Initiative and the Mile High United Way in Denver, and isn't sure how she would have made it without this support. Gina saved for assets and with matches through her Opportunity Passport, she was able to put a $300 deposit on an apartment and buy a new Hyundai. A door opener a person or organization in the community who offers opportunities for youth in or formerly in foster care to work toward self-sufficiency gave her discounted rent on the three-bedroom apartment for her and her three children, and even hired Gina as a leasing agent. "My whole life has changed as a result of this," says Gina, "I wouldn't have this apartment. Through my job, I have life insurance, health insurance and a 401K. This is the first job in which I'm not on any assistance. This is a dream come true. I never thought I would have a job where I would be able to support myself." But in the end, we are interested in improving the overall well-being of youth transitioning from care. An area for continued study is how the utilization of an IDA can improve a young person s life trajectory. For the Initiative, it is still too early in implementation to see changes in life outcomes. Across our sites, implementation of the Opportunity Passport was staggered over the past five years. Therefore, the young people in our longitudinal group have an average length of participation of only about two years. However, we have begun to see some differences in outcomes for asset purchasers as compared to those that have not yet purchased an asset. In particular, asset purchasers are more likely to self-report being employed and having safe, stable and affordable housing, and they experience greater rates of improvement over time vi. These are very early trends, and we will see if they hold as the longitudinal data become more robust. But the trends are also not surprising. The opportunity for an IDA promotes regular employment. Does it matter whether the IDA motivates a young person to obtain employment in order to save for an asset, or that the young person is able to save for an asset because they were previously employed? Either way, steady employment and savings behavior are rewarded. Furthermore, there are logical reasons why the most-utilized assets would impact housing and employment. The purchase of a car, the most common asset purchased, has potential to impact both employment and housing opportunities very quickly. Young people with a car immediately have a broader geographic area within which they can find appropriate employment or housing, while also providing reliable transportation to and from their job. And clearly a match for an apartment deposit can directly impact having safe, stable and affordable housing. The connection between asset purchases and youth outcomes needs more time and research to substantiate. However, what the data are also beginning to suggest and what the participants have told us and common sense dictates is that what young people need more than anything is a family. Early trends show that those participants who report having a permanent adult in their life are more likely to do better across outcome areas, in particular related to housing, health insurance coverage, and personal and community engagement vii. This overarching need for a family must never be overlooked as targeted supports for young people leaving foster care are considered. 7

9 Recommendations for policy and practice The IDA is one important resource that can be utilized by young people transitioning from care. Based on our experience and data, we recommend that during the upcoming reauthorization of the Assets for Independence Act, policymakers should make asset-building programs available for young people ages transitioning from foster care that: include vehicles as allowable assets for IDAs for this population; expand the home ownership asset to allow for apartment deposits; and ensure that the financial literacy training provided is developmentally appropriate. We further recommend systemic changes in the practice of child welfare and asset development practitioners that would support youth until age 21 in: making permanent connections to family that better ensure sustainable support; guiding their participation in asset-building programs; attending and completing post-secondary education or training; and attaining and retaining employment, housing, and health care. i Kids are Waiting and the Jim Casey Youth Opportunities Initiative (2007) Time for Reform: Aging Out and On their Own Philadelphia, PA: Pew Charitable Trusts. ii Jim Casey Youth Opportunities Initiative has ten demonstration sites: Atlanta, Connecticut, Denver/Front Range, Des Moines, Maine, Michigan, Nashville, Rhode Island, San Diego, and Tampa; and two co-investment sites in Nebraska and Indiana. iii Data collected from ten demonstration sites through December 31, iv Schreiner, M., Clancy, M., & Sherraden, M. (2002). Final Report. Saving Performance in the American Dream Demonstration: A National Demonstration of Individual Development Accounts. St. Louis, MO: Washington University, Center for Social Development. v Unpublished data, Jim Casey Youth Opportunities Initiative, June The average number of deposits for asset purchasers is 14.6; for non-asset purchasers the average number of deposits is 6.5. The average number of unmatched withdrawals for assets purchasers is 8; for non-asset purchasers the average number of unmatched withdrawals is 6.5. vi Cross-Site Report: Youth Indicator Findings on Opportunity Passport Participants, Jim Casey Youth Opportunities Initiative, November vii Cross-Site Report: Youth Indicator Findings on Opportunity Passport Participants, Jim Casey Youth Opportunities Initiative, November

10

11

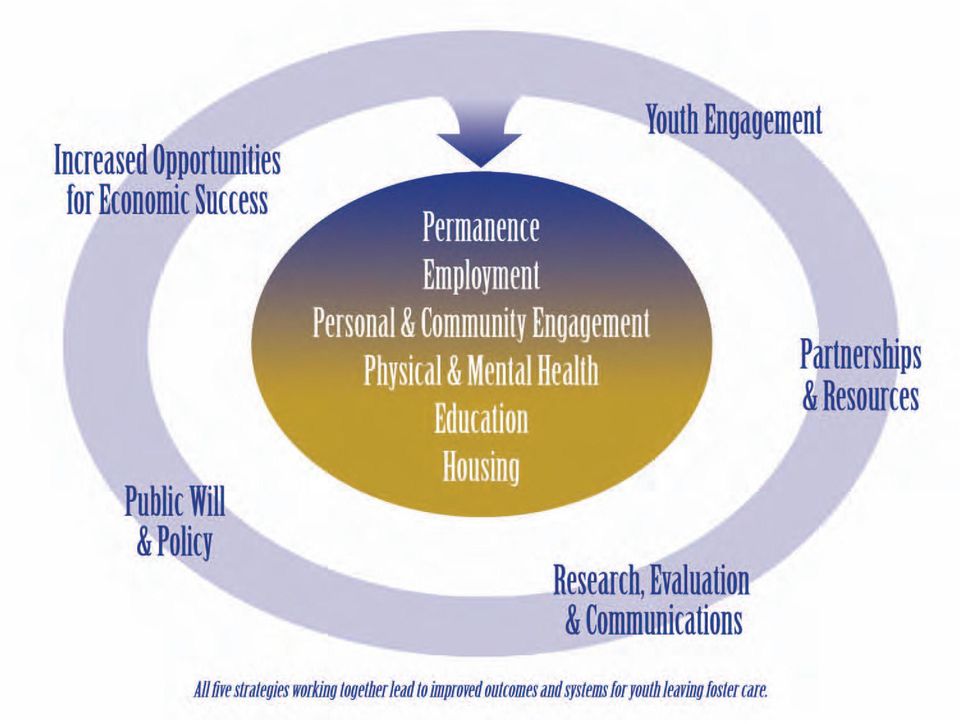

12 The Jim Casey Youth Opportunities Initiative is a national foundation that brings together the people, resources and systems necessary to assist youth leaving foster care make successful transitions to adulthood. The Initiative achieves its mission through making grants, providing technical assistance, and advocating for improved policy and practice. The Initiative is working in sites nationwide that implement five broad strategies: Youth Engagement; Partnerships and Resources; Research, Evaluation and Communications; Public Will and Policy; and Increased Opportunities. As part of the Increased Opportunities strategy, the Opportunity Passport is a package of resources that is used to create opportunities for young people leaving foster care. The Opportunity Passport has three distinct components: a personal bank account for short-term expenses and instant cash; a matched savings account (or IDA) for asset-building; and door openers, which are opportunities developed on a local basis (e.g., expedited access to job training or adult education courses). More information can be found on our website at: Metis Associates, an independent research and evaluation consulting organization, provides ongoing evaluation and technical assistance to the Jim Casey Youth Opportunities Initiative on the collection, maintenance, analysis, interpretation and presentation of data. Metis has been working collaboratively with the Initiative and its ten demonstration sites to examine and assess progress on implementation and outcomes. Improvement is tracked through the self-evaluation efforts of each site, using the data collection tools and assistance provided by the Initiative. Metis supports the self-evaluation work at each site and aggregates and evaluates the data across sites. Information about Metis Associates can be found at: South Central, Suite 305, Saint Louis, Missouri

The Challenge of Retaining College Students Who Grew up in Foster Care

Who Grew up in Foster Care By Yvonne A. Unrau, Ph.D., Founding Director Ronicka Hamilton, M.A., Seita Campus Coach Kristin Putney, M.S.W., Seita Campus Coach Seita Scholars Program, Western Michigan University

Who Grew up in Foster Care By Yvonne A. Unrau, Ph.D., Founding Director Ronicka Hamilton, M.A., Seita Campus Coach Kristin Putney, M.S.W., Seita Campus Coach Seita Scholars Program, Western Michigan University

Federal Chafee Funds and State Matched Savings Programs for Foster Youth. Policy and Practice Working Paper. April 2007 Volume 1 Issue 3

Policy and Practice Working Paper April 2007 Volume 1 Issue 3 Federal Chafee Funds and State Matched Savings Programs for Foster Youth Written by James Nguyen Introduction This paper provides policy and

Policy and Practice Working Paper April 2007 Volume 1 Issue 3 Federal Chafee Funds and State Matched Savings Programs for Foster Youth Written by James Nguyen Introduction This paper provides policy and

ASSET-DEVELOPMENT OPPORTUNITIES FOR DOMESTIC VIOLENCE AND SEXUAL ASSAULT SURVIVORS

ASSET-DEVELOPMENT OPPORTUNITIES FOR DOMESTIC VIOLENCE AND SEXUAL ASSAULT SURVIVORS KEY FACTS > More than one in three women have experienced domestic violence in their lifetime. 71 > Nearly one in five

ASSET-DEVELOPMENT OPPORTUNITIES FOR DOMESTIC VIOLENCE AND SEXUAL ASSAULT SURVIVORS KEY FACTS > More than one in three women have experienced domestic violence in their lifetime. 71 > Nearly one in five

Debt and Assets Among Low-Income Families

Identifying and promoting strategies that prevent child poverty in the U.S. and that improve the lives of low-income children and families. Debt and Assets Among Low-Income Families Robert Wagmiller October

Identifying and promoting strategies that prevent child poverty in the U.S. and that improve the lives of low-income children and families. Debt and Assets Among Low-Income Families Robert Wagmiller October

Serving Teens Transitioning Into Adulthood. The Condensed Version

Serving Teens Transitioning Into Adulthood The Condensed Version The Basics... CONTRACTUAL AGREEMENT FOR RESIDENTIAL SUPPORT (CARS) NC LINKS EDUCATION EMPLOYMENT HOUSING HEALTH CARE IMMIGRATION OPTIONS

Serving Teens Transitioning Into Adulthood The Condensed Version The Basics... CONTRACTUAL AGREEMENT FOR RESIDENTIAL SUPPORT (CARS) NC LINKS EDUCATION EMPLOYMENT HOUSING HEALTH CARE IMMIGRATION OPTIONS

Many states have passed laws to improve education outcomes for children in foster care. Innovative approaches include:

The federal Fostering Connections to Success and Increasing Adoptions Act of 2008 (Fostering Connections) promotes education stability for all children in foster care. A May 2014 joint letter from the

The federal Fostering Connections to Success and Increasing Adoptions Act of 2008 (Fostering Connections) promotes education stability for all children in foster care. A May 2014 joint letter from the

CRS Report for Congress

Order Code RS22501 September 6, 2006 CRS Report for Congress Received through the CRS Web Summary Child Welfare: The Chafee Foster Care Independence Program (CFCIP) Adrienne L. Fernandes Analyst in Social

Order Code RS22501 September 6, 2006 CRS Report for Congress Received through the CRS Web Summary Child Welfare: The Chafee Foster Care Independence Program (CFCIP) Adrienne L. Fernandes Analyst in Social

LEAN ON ME. He took me to this gas station in Colorado Springs and dropped me off with all my stuff. I called my mom and she came and got me.

You survived the streets for days or maybe months. Then a street outreach worker tells you about a safe place to go for food, clothes, and a hot shower. Tired and alone, you decide to check the place out.

You survived the streets for days or maybe months. Then a street outreach worker tells you about a safe place to go for food, clothes, and a hot shower. Tired and alone, you decide to check the place out.

The Jim Casey Youth Opportunities Initiative

CHAFEE PLUS TEN: A VISION FOR THE NEXT DECADE The Jim Casey Youth Opportunities Initiative Ensuring that each youth in foster care has both permanent family connections and the life skills to make a successful

CHAFEE PLUS TEN: A VISION FOR THE NEXT DECADE The Jim Casey Youth Opportunities Initiative Ensuring that each youth in foster care has both permanent family connections and the life skills to make a successful

Discover What s Possible

Discover What s Possible Guaranteed Term 10-15-20 Guaranteed Term 10 15 20 Life is filled with possibilities As your life unfolds, you will have many dreams and goals. Your financial needs will continue

Discover What s Possible Guaranteed Term 10-15-20 Guaranteed Term 10 15 20 Life is filled with possibilities As your life unfolds, you will have many dreams and goals. Your financial needs will continue

Quotes for car insurance

Quotes for car insurance When I was a small child, as was the case with most parents, my parents gave me an allowance. It started with 25 cents per week. Now at age 5 that was impressive to me. I remember

Quotes for car insurance When I was a small child, as was the case with most parents, my parents gave me an allowance. It started with 25 cents per week. Now at age 5 that was impressive to me. I remember

September 29, 2015. The Honorable Jim McDermott 1035 Longworth HOB U.S. House of Representatives Washington, D.C. 20515

September 29, 2015 The Honorable Karen Bass 408 Cannon HOB U.S. House of Representatives Washington, D.C. 20515 The Honorable Jim McDermott 1035 Longworth HOB U.S. House of Representatives Washington,

September 29, 2015 The Honorable Karen Bass 408 Cannon HOB U.S. House of Representatives Washington, D.C. 20515 The Honorable Jim McDermott 1035 Longworth HOB U.S. House of Representatives Washington,

Head Start Annual Report

Head Start Annual Report Children s Friend Early Head Start and Head Start provides a comprehensive child and family development program for low-income children birth to age five and their families, as

Head Start Annual Report Children s Friend Early Head Start and Head Start provides a comprehensive child and family development program for low-income children birth to age five and their families, as

My name is Ana Maria Alvarez

I had come to the United States dreaming of finding my mother but I ended up discovering so much more about myself. My name is Ana Maria Alvarez and I am 20 years old. I am from Guatemala I came to Mary

I had come to the United States dreaming of finding my mother but I ended up discovering so much more about myself. My name is Ana Maria Alvarez and I am 20 years old. I am from Guatemala I came to Mary

Supplemental Health Insurance Products Inventory Report. May 2014

Supplemental Health Insurance Products Inventory Report May 2014 1 Health Insurance Options for the Uninsured In May of 2014, Gallup estimated that 13.4% of Americans were uninsured, which means approximately

Supplemental Health Insurance Products Inventory Report May 2014 1 Health Insurance Options for the Uninsured In May of 2014, Gallup estimated that 13.4% of Americans were uninsured, which means approximately

Testimony of Robert Geremia Teacher, Washington Teachers Union and American Federation of Teachers

Testimony of Robert Geremia Teacher, Washington Teachers Union and American Federation of Teachers Senate Committee of Banking, Housing, and Urban Affairs Financial Institutions and Consumer Protection

Testimony of Robert Geremia Teacher, Washington Teachers Union and American Federation of Teachers Senate Committee of Banking, Housing, and Urban Affairs Financial Institutions and Consumer Protection

CECW. Programs for youths transitioning from foster care to independence 1. Introduction

Programs for youths transitioning from foster care to independence 1 2009 2006 #70E #42E CECW Della Knoke This information sheet describes some of the challenges faced by youths growing up in foster care

Programs for youths transitioning from foster care to independence 1 2009 2006 #70E #42E CECW Della Knoke This information sheet describes some of the challenges faced by youths growing up in foster care

Adolescent Services Strategic Plan:

Adolescent Services Strategic Plan: Striving for Success in Transitions to Adulthood 2011 2014 Prepared by Kerrie Ocasio, MSW, Ph.D. Candidate Institute for Families at the Rutgers School of Social Work

Adolescent Services Strategic Plan: Striving for Success in Transitions to Adulthood 2011 2014 Prepared by Kerrie Ocasio, MSW, Ph.D. Candidate Institute for Families at the Rutgers School of Social Work

How Health Reform Will Help Children with Mental Health Needs

How Health Reform Will Help Children with Mental Health Needs The new health care reform law, called the Affordable Care Act (or ACA), will give children who have mental health needs better access to the

How Health Reform Will Help Children with Mental Health Needs The new health care reform law, called the Affordable Care Act (or ACA), will give children who have mental health needs better access to the

Welcome! AFI Program Overview & Grant Application Process. AFI Resource Center 1-866-778-6037 info@idaresources.org

Welcome! AFI Program Overview & Grant Application Process AFI Resource Center 1-866-778-6037 info@idaresources.org Assets for Independence Special federally funded 5-year grants to organizations that enable

Welcome! AFI Program Overview & Grant Application Process AFI Resource Center 1-866-778-6037 info@idaresources.org Assets for Independence Special federally funded 5-year grants to organizations that enable

Payday Loans Poverty in America A Money Mystery Career Corner

Payday Loans Poverty in America A Money Mystery Career Corner We talk a lot about the high cost of credit card debt with interest rates running from 18-25% a year. But compared to the interest rates being

Payday Loans Poverty in America A Money Mystery Career Corner We talk a lot about the high cost of credit card debt with interest rates running from 18-25% a year. But compared to the interest rates being

KEY TAKE-AWAYS In our work, we, on the Teen Advisory Board, have identified several priority concerns and proposed solutions.

KEY TAKE-AWAYS In our work, we, on the Teen Advisory Board, have identified several priority concerns and proposed solutions. These include: Documentation Youth in foster care must have access to key personal

KEY TAKE-AWAYS In our work, we, on the Teen Advisory Board, have identified several priority concerns and proposed solutions. These include: Documentation Youth in foster care must have access to key personal

1. INTRODUCTION Page 9. 2. GENERAL QUESTIONS ABOUT FOSTERING CONNECTIONS Page 12. 3. PERMANENCY Page 16

ABOUT THE NATIONAL FOSTER CARE COALITION Page 7 1. INTRODUCTION Page 9 2. GENERAL QUESTIONS ABOUT FOSTERING CONNECTIONS Page 12 a. What is the Fostering Connections to Success and Increasing Adoptions

ABOUT THE NATIONAL FOSTER CARE COALITION Page 7 1. INTRODUCTION Page 9 2. GENERAL QUESTIONS ABOUT FOSTERING CONNECTIONS Page 12 a. What is the Fostering Connections to Success and Increasing Adoptions

Raising Expectations for States, Education Providers and Adult Learners

The Adult Education and Economic Growth Act (AEEGA) was introduced in the House of Representatives in June 2011 by Rep. Ruben Hinojosa (TX-15). 1 The bill (H.R. 2226) would amend the Workforce Investment

The Adult Education and Economic Growth Act (AEEGA) was introduced in the House of Representatives in June 2011 by Rep. Ruben Hinojosa (TX-15). 1 The bill (H.R. 2226) would amend the Workforce Investment

Raising Expectations for States, Education Providers and Adult Learners

The Adult Education and Economic Growth Act (AEEGA) was introduced in the House of Representatives in June 2011 by Rep. Ruben Hinojosa (TX-15) 1 and in February 2012 in the Senate by Sen. Jim Webb (VA).

The Adult Education and Economic Growth Act (AEEGA) was introduced in the House of Representatives in June 2011 by Rep. Ruben Hinojosa (TX-15) 1 and in February 2012 in the Senate by Sen. Jim Webb (VA).

The Family Self-Sufficiency Program: A Promising, Low-Cost Vehicle to Promote Savings and Asset Building for Recipients of Federal Housing Assistance

Issue Brief #9 March 2005 The Family Self-Sufficiency Program: A Promising, Low-Cost Vehicle to Promote Savings and Asset Building for Recipients of Federal Housing Assistance Reid Cramer and Jeff Lubell

Issue Brief #9 March 2005 The Family Self-Sufficiency Program: A Promising, Low-Cost Vehicle to Promote Savings and Asset Building for Recipients of Federal Housing Assistance Reid Cramer and Jeff Lubell

A HAND UP How State Earned Income Tax Credits Help Working Families Escape Poverty in 2004. Summary. By Joseph Llobrera and Bob Zahradnik

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org May 14, 2004 A HAND UP How State Earned Income Tax Credits Help Working Families Escape

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org May 14, 2004 A HAND UP How State Earned Income Tax Credits Help Working Families Escape

For decades, the Pine Ridge Indian Reservation of South Dakota

THE LAKOTA FUNDS STORY How Indian Country is Building Financial Capability Elsie M. Meeks Lakota Funds For decades, the Pine Ridge Indian Reservation of South Dakota has been among the poorest, if not

THE LAKOTA FUNDS STORY How Indian Country is Building Financial Capability Elsie M. Meeks Lakota Funds For decades, the Pine Ridge Indian Reservation of South Dakota has been among the poorest, if not

Participant Guide Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum

Loan to Own Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum Table of Contents Page Lending Terms 1 Consumer Installment Loan Versus Rent-to-Own 2 Federal Trade Commission

Loan to Own Building: Knowledge, Security, Confidence FDIC Financial Education Curriculum Table of Contents Page Lending Terms 1 Consumer Installment Loan Versus Rent-to-Own 2 Federal Trade Commission

By Hart Research Associates

One Year Out Findings From A National Survey Among Members Of The High School Graduating Class Of 2010 Submitted To: The College Board By Hart Research Associates August 18, 2011 Hart Research Associates

One Year Out Findings From A National Survey Among Members Of The High School Graduating Class Of 2010 Submitted To: The College Board By Hart Research Associates August 18, 2011 Hart Research Associates

Higher Education: A Pathway to Opportunity Making Higher Education Affordable and Effective for All Rhode Islanders

A Note from Gina Dear friend, Higher Education: A Pathway to Opportunity Making Higher Education Affordable and Effective for All Rhode Islanders Like so many other Rhode Islanders, my family s American

A Note from Gina Dear friend, Higher Education: A Pathway to Opportunity Making Higher Education Affordable and Effective for All Rhode Islanders Like so many other Rhode Islanders, my family s American

Assisting Members in Attaining Education Goals

Assisting Members in Attaining Education Goals Importance of Education and Employment o Education is often the key to financial security through employment. o Consistent with treating members like anybody

Assisting Members in Attaining Education Goals Importance of Education and Employment o Education is often the key to financial security through employment. o Consistent with treating members like anybody

What you know about life insurance

What you need to know about life insurance This piece has been reproduced with the permission of Life Happens, a nonprofit organization dedicated to helping consumers make smart insurance decisions to

What you need to know about life insurance This piece has been reproduced with the permission of Life Happens, a nonprofit organization dedicated to helping consumers make smart insurance decisions to

Access and Barriers to Post-Secondary Education Under Michigan's Welfare to Work Policies

Access and Barriers to Post-Secondary Education Under Michigan's Welfare to Work Policies Policy Background and Recipients' Experiences Coalition for Independence Through Education (CFITE) February 2002

Access and Barriers to Post-Secondary Education Under Michigan's Welfare to Work Policies Policy Background and Recipients' Experiences Coalition for Independence Through Education (CFITE) February 2002

GOING BEYOND FOSTER CARE

GOING BEYOND FOSTER CARE Sharon W. Cooper, MD Developmental & Forensic Pediatrics, P.A. University of North Carolina Chapel Hill School of Medicine Sharon_Cooper@med.unc.edu OBJECTIVES Adverse childhood

GOING BEYOND FOSTER CARE Sharon W. Cooper, MD Developmental & Forensic Pediatrics, P.A. University of North Carolina Chapel Hill School of Medicine Sharon_Cooper@med.unc.edu OBJECTIVES Adverse childhood

(photo representative of client)

") (photo representative of client) Susan F., a single mother of three small children, ages seven, three and one applied for a job driving a bus. This job would work perfectly with her children s schedules

(photo representative of client) Susan F., a single mother of three small children, ages seven, three and one applied for a job driving a bus. This job would work perfectly with her children s schedules

Progressive Economic Narrative: Health Care

Progressive Economic Narrative: Health Care 1. What s Wrong with the Economy? Today the middle class is getting crushed and closed off. Working and middle-class families are struggling, while the super-rich

Progressive Economic Narrative: Health Care 1. What s Wrong with the Economy? Today the middle class is getting crushed and closed off. Working and middle-class families are struggling, while the super-rich

Compass Working Capital Financial Stability and Savings (FSS) Program Growth Plan: 2013-2015

Program Growth Plan: 2013-2015") Compass Working Capital Financial Stability and Savings (FSS) Program Growth Plan: 2013-2015 Compass Working Capital Mission Founded in 2005, Compass Working Capital ( Compass ) is a Boston-based nonprofit

Compass Working Capital Financial Stability and Savings (FSS) Program Growth Plan: 2013-2015 Compass Working Capital Mission Founded in 2005, Compass Working Capital ( Compass ) is a Boston-based nonprofit

POSTSECONDARY SUCCESS OF YOUNG ADULTS: SYSTEM IMPACT OPPORTUNITIES IN ADULT EDUCATION. Executive Summary

POSTSECONDARY SUCCESS OF YOUNG ADULTS: SYSTEM IMPACT OPPORTUNITIES IN ADULT EDUCATION Executive Summary Young adults who come through adult education are among the most under represented students in postsecondary

POSTSECONDARY SUCCESS OF YOUNG ADULTS: SYSTEM IMPACT OPPORTUNITIES IN ADULT EDUCATION Executive Summary Young adults who come through adult education are among the most under represented students in postsecondary

Westcoast Children s Clinic

Westcoast Children s Clinic The future promise of any nation can be directly mesured by the present prospects of its youth. President John F. Kennedy, February 14, 1963 Dear Friend: November 2008 By the

Westcoast Children s Clinic The future promise of any nation can be directly mesured by the present prospects of its youth. President John F. Kennedy, February 14, 1963 Dear Friend: November 2008 By the

How To Get A Job At A Community College

28 Preview Now More Than Ever: Community Colleges Daniel Wister When Miranda left for school at a faraway university, she thought that all her dreams were on their way to coming true. Then, once disappointment

28 Preview Now More Than Ever: Community Colleges Daniel Wister When Miranda left for school at a faraway university, she thought that all her dreams were on their way to coming true. Then, once disappointment

Discover What s Possible

Discover What s Possible Guaranteed Term 10-15-20 Guaranteed Term 10 15 20 Life is filled with possibilities As your life unfolds, you will have many dreams and goals. Your financial needs will continue

Discover What s Possible Guaranteed Term 10-15-20 Guaranteed Term 10 15 20 Life is filled with possibilities As your life unfolds, you will have many dreams and goals. Your financial needs will continue

WHAT S IN THE PROPOSED FY 2016 BUDGET FOR HEALTH CARE?

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 408-1073 www.dcfpi.org April 16, 2015 WHAT S IN THE PROPOSED FY 2016

An Affiliate of the Center on Budget and Policy Priorities 820 First Street NE, Suite 460 Washington, DC 20002 (202) 408-1080 Fax (202) 408-1073 www.dcfpi.org April 16, 2015 WHAT S IN THE PROPOSED FY 2016

Life insurance is a simple answer to a very difficult question:

Chances are, you need life insurance Life insurance is a simple answer to a very difficult question: How will my family manage financially when I die? It s a subject no one really wants to think about.

Chances are, you need life insurance Life insurance is a simple answer to a very difficult question: How will my family manage financially when I die? It s a subject no one really wants to think about.

3-2: Open a Savings Account

MODULE 3: SAVINGS/SPENDING PLAN 3-2: Open a Savings Account Cast List Darryl Terri Millie Dunn, consumer financial expert with Lifetime Savings and Loan; 60-65, motherly Caucasian woman Synopsis Terri

MODULE 3: SAVINGS/SPENDING PLAN 3-2: Open a Savings Account Cast List Darryl Terri Millie Dunn, consumer financial expert with Lifetime Savings and Loan; 60-65, motherly Caucasian woman Synopsis Terri

Wealth Inequity, Debt and Savings

Wealth Inequity, Debt and Savings Implications for Policy and Financial Services Sandra Venner FDIC Alliance for Economic Inclusion May 21, 2008 Today, government wealth building policy is primarily in

Wealth Inequity, Debt and Savings Implications for Policy and Financial Services Sandra Venner FDIC Alliance for Economic Inclusion May 21, 2008 Today, government wealth building policy is primarily in

Growing Knowledge from

Growing Knowledge from SEED November 2006 Lessons learned from the Saving for Education, Entrepreneurship, and Downpayment Initiative Learning to save: Lessons on financial education By Carl Rist and Sarah

Growing Knowledge from SEED November 2006 Lessons learned from the Saving for Education, Entrepreneurship, and Downpayment Initiative Learning to save: Lessons on financial education By Carl Rist and Sarah

Protecting Your Loved Ones Every Step of the Way

Protecting Your Loved Ones Every Step of the Way Gerber Life Insurance Company Gerber Life Insurance Company, White Plains, NY 10605 5/10/2011 Gerber Life Insurance Company is a financially separate affiliate

Protecting Your Loved Ones Every Step of the Way Gerber Life Insurance Company Gerber Life Insurance Company, White Plains, NY 10605 5/10/2011 Gerber Life Insurance Company is a financially separate affiliate

California College Pathways Educational Guide: A Guide to Career Development Opportunities in California s High Schools: Career Goal Worksheet

A Caregivers Guide To Helping Youth Develop Independent Living Skills Traditionally services to prepare foster youth for adulthood have been relegated to Independent Living Programs. These programs, whether

A Caregivers Guide To Helping Youth Develop Independent Living Skills Traditionally services to prepare foster youth for adulthood have been relegated to Independent Living Programs. These programs, whether

An outline of National Standards for Out of home Care

Department of Families, Housing, Community Services and Indigenous Affairs together with the National Framework Implementation Working Group An outline of National Standards for Out of home Care A Priority

Department of Families, Housing, Community Services and Indigenous Affairs together with the National Framework Implementation Working Group An outline of National Standards for Out of home Care A Priority

My name is Emma Kallaway. I graduated from the University of Oregon in 2010 with $25,000 in student

Testimony for the OSA Good Afternoon Members of the Committee, My name is Emma Kallaway. I graduated from the University of Oregon in 2010 with $25,000 in student loan debt. I am the Executive Director

Testimony for the OSA Good Afternoon Members of the Committee, My name is Emma Kallaway. I graduated from the University of Oregon in 2010 with $25,000 in student loan debt. I am the Executive Director

Colony Term. I Life Insurance. The Traditional Term Solution. Consumer Guide ColonySM Term

I Consumer Guide ColonySM Term I Life Insurance Colony Term The Traditional Term Solution Life insurance products underwritten by: Genworth Life and Annuity Insurance Company, Genworth Life Insurance Company,

I Consumer Guide ColonySM Term I Life Insurance Colony Term The Traditional Term Solution Life insurance products underwritten by: Genworth Life and Annuity Insurance Company, Genworth Life Insurance Company,

Latino Community Credit Union (LCCU , North Carolina

U.S. Department of the Treasury Office of Financial Education Community Financial Access Pilot: Elements of an Effective Banking the Unbanked Strategy Bank and credit union accounts serve three basic functions:

U.S. Department of the Treasury Office of Financial Education Community Financial Access Pilot: Elements of an Effective Banking the Unbanked Strategy Bank and credit union accounts serve three basic functions:

Rhode Island KIDS COUNT Presents: Newport Data in Your Backyard ~~~

For Immediate Release Contact: Raymonde Charles Day: (401) 351-9400, Ext. 22 rcharles@rikidscount.org Rhode Island KIDS COUNT Presents: Newport Data in Your Backyard The percentage of Newport eighth graders

For Immediate Release Contact: Raymonde Charles Day: (401) 351-9400, Ext. 22 rcharles@rikidscount.org Rhode Island KIDS COUNT Presents: Newport Data in Your Backyard The percentage of Newport eighth graders

NATIONAL BABY FACTS. Infants, Toddlers, and Their Families in the United States THE BASICS ABOUT INFANTS AND TODDLERS

NATIONAL BABY FACTS Infants, Toddlers, and Their Families in the United States T he facts about infants and toddlers in the United States tell us an important story of what it s like to be a very young

NATIONAL BABY FACTS Infants, Toddlers, and Their Families in the United States T he facts about infants and toddlers in the United States tell us an important story of what it s like to be a very young

Ready to Compete? - Pennsylvania s Community Colleges: A Three-Part Series Part I: Affordability

Ready to Compete? - Pennsylvania s Community Colleges: A Three-Part Series Part I: Affordability Even in the best of economic times, Pennsylvanians found themselves searching for good jobs that were always

Ready to Compete? - Pennsylvania s Community Colleges: A Three-Part Series Part I: Affordability Even in the best of economic times, Pennsylvanians found themselves searching for good jobs that were always

Before the House Ways and Means Committee Subcommittee on Oversight. June 24, 2015 10:00 AM

Testimony of Washington State Insurance Commissioner, Mike Kreidler Before the House Ways and Means Committee Subcommittee on Oversight June 24, 2015 10:00 AM Good morning Chairman Roskam, Ranking Member

Testimony of Washington State Insurance Commissioner, Mike Kreidler Before the House Ways and Means Committee Subcommittee on Oversight June 24, 2015 10:00 AM Good morning Chairman Roskam, Ranking Member

State Policies to Help Youth Transition Out of Foster Care

Contact: Sarah Oldmixon Policy Analyst Social, Economic, and Workforce Programs 202/624-7822 January 2007 State Policies to Help Youth Transition Out of Foster Care Executive Summary Most youth who leave

Contact: Sarah Oldmixon Policy Analyst Social, Economic, and Workforce Programs 202/624-7822 January 2007 State Policies to Help Youth Transition Out of Foster Care Executive Summary Most youth who leave

Simplifying Life Insurance

Simplifying Life Insurance Think Differently About Life A sound financial plan is essential to ensure a smooth path through all stages of life and help you reach future goals. A plan centered on life insurance

Simplifying Life Insurance Think Differently About Life A sound financial plan is essential to ensure a smooth path through all stages of life and help you reach future goals. A plan centered on life insurance

Prepared For: Prepared By: James Bell Associates, Inc. Arlington, Virginia. August 2015

Summary of the Title IV-E Child Welfare Waiver Demonstrations Prepared For: Children s Bureau Administration on Children, Youth, and Families Administration for Children and Families U.S. Department of

Summary of the Title IV-E Child Welfare Waiver Demonstrations Prepared For: Children s Bureau Administration on Children, Youth, and Families Administration for Children and Families U.S. Department of

KEY FINDINGS AND IMPLICATIONS

May 2015 Publication #2015-20 The Developing Brain: IMPLICATIONS FOR YOUTH PROGRAMS OVERVIEW The brain, with more than 100 billion neurons, is our body s most complex organ. There is increasing global

May 2015 Publication #2015-20 The Developing Brain: IMPLICATIONS FOR YOUTH PROGRAMS OVERVIEW The brain, with more than 100 billion neurons, is our body s most complex organ. There is increasing global

National Definitions of PATH Eligibility and PATH Enrollment

National Definitions of PATH Eligibility and PATH Enrollment Webcast 10/29/09 Mattie Curry Cheek, PhD, Director, PATH Program, SPC, Washington Monica Bellamy, SPC, Michigan Laura Gillis, PATH Technical

National Definitions of PATH Eligibility and PATH Enrollment Webcast 10/29/09 Mattie Curry Cheek, PhD, Director, PATH Program, SPC, Washington Monica Bellamy, SPC, Michigan Laura Gillis, PATH Technical

My Money Personality. Money Beliefs. Your Values. Should I Be Listening? What does money mean to you? Independence? Power? Fame? Stuff?

TEEN GUIDE moneytalks4teens.org Should I Be Listening? My Money Personality What does money mean to you? Independence? Power? Fame? Stuff? Discover your Money Personality inside. Publication 8272 Surprise

TEEN GUIDE moneytalks4teens.org Should I Be Listening? My Money Personality What does money mean to you? Independence? Power? Fame? Stuff? Discover your Money Personality inside. Publication 8272 Surprise

AB12 The California Fostering Connections to Success Act

AB12 The California Fostering Connections to Success Act April 7, 2011 C I T Y & C O U N T Y O F S A N F R A N C I S C O Human Services Agency H U M A N S E R V I C E S A G E N C Y Assembly Bill 12: Extended

AB12 The California Fostering Connections to Success Act April 7, 2011 C I T Y & C O U N T Y O F S A N F R A N C I S C O Human Services Agency H U M A N S E R V I C E S A G E N C Y Assembly Bill 12: Extended

Tax Help Colorado Client Stories 2015 Tax Season

Tax Help Colorado Client Stories 2015 Tax Season Alejandro Denver, Colorado Alejandro lives in West Denver with his family of four and works as a roofer to support them. As he waits to get his taxes prepared

Tax Help Colorado Client Stories 2015 Tax Season Alejandro Denver, Colorado Alejandro lives in West Denver with his family of four and works as a roofer to support them. As he waits to get his taxes prepared

ACVL Web Site LEASING VS. BUYING QUIZ

ACVL Web Site LEASING VS. BUYING QUIZ There are many factors to consider when deciding whether to lease or finance your next vehicle. To help consumers weigh their circumstances and understand whether

ACVL Web Site LEASING VS. BUYING QUIZ There are many factors to consider when deciding whether to lease or finance your next vehicle. To help consumers weigh their circumstances and understand whether

story: I have no problem lending money to family & friends as long as I can afford it.

name: Emily state: Texas story: My husband has borrowed money from his parents many different times without my knowing. I think that if you expect repayment, a written loan agreement or share secured loan

name: Emily state: Texas story: My husband has borrowed money from his parents many different times without my knowing. I think that if you expect repayment, a written loan agreement or share secured loan

The Aspen Institute Initiative on Financial Security (Aspen IFS) proposes. incentives available to low- and middleincome

proposes. incentives available to low- and middleincome") BACK TO BASICS: A SAVINGS APPROACH TO HOMEOWNERSHIP Homeownership is a core American value. It epitomizes the American Dream and the be a springboard to the acquisition of other important assets like a

BACK TO BASICS: A SAVINGS APPROACH TO HOMEOWNERSHIP Homeownership is a core American value. It epitomizes the American Dream and the be a springboard to the acquisition of other important assets like a

I have always been good at school. I enjoyed it, and did very well. I think that is why I never got a diagnosis of Asperger s Syndrome until

Jennica s Speech for Family Weekend Brunch ASAT student Jennica Harris was a featured speaker at Chapel Haven s April 27, 2014 Family Weekend Brunch. Her remarks are shared with her permission. Hello!

Jennica s Speech for Family Weekend Brunch ASAT student Jennica Harris was a featured speaker at Chapel Haven s April 27, 2014 Family Weekend Brunch. Her remarks are shared with her permission. Hello!

Our Mission To ensure the success of children in jeopardy by empowering families. Our Vision A community where all children and families flourish

Our Mission To ensure the success of children in jeopardy by empowering families Our Vision A community where all children and families flourish Who We Are Georgia s largest nonprofit, family-service agency

Our Mission To ensure the success of children in jeopardy by empowering families Our Vision A community where all children and families flourish Who We Are Georgia s largest nonprofit, family-service agency

Wealth. Build. VivoCash. Why is it good for me? your. Financial returns till age 100. Living the moment, protecting the future.

Build your Wealth VivoCash Financial returns till age 100. Living the moment, protecting the future. A dream home. A comfortable lifestyle. And the freedom to travel wherever you want. In recent years,

Build your Wealth VivoCash Financial returns till age 100. Living the moment, protecting the future. A dream home. A comfortable lifestyle. And the freedom to travel wherever you want. In recent years,

Bank of America/USA TODAY Better Money Habits Millennial Report

Letter from Andrew Plepler, Global Corporate Social Responsibility Executive We are pleased to share the results from the second Bank of America/ USA TODAY Better Money Habits Millennial Report, which

Letter from Andrew Plepler, Global Corporate Social Responsibility Executive We are pleased to share the results from the second Bank of America/ USA TODAY Better Money Habits Millennial Report, which

HUSKY Program Coverage for Infants: Maintaining Coverage When Babies Turn One

HUSKY Program Coverage for Infants: Maintaining Coverage When Babies Turn One May 2011 Key Findings In Connecticut, babies who are enrolled in HUSKY A (Medicaid) are at risk of losing coverage when they

HUSKY Program Coverage for Infants: Maintaining Coverage When Babies Turn One May 2011 Key Findings In Connecticut, babies who are enrolled in HUSKY A (Medicaid) are at risk of losing coverage when they

LIFE INSURANCE SUMMARY

LIFE INSURANCE SUMMARY Your family can count on your paycheck to meet day-to-day expenses while you are actively at work, but it is important to plan for their financial security in the event of your death.

LIFE INSURANCE SUMMARY Your family can count on your paycheck to meet day-to-day expenses while you are actively at work, but it is important to plan for their financial security in the event of your death.

Transitional Kindergarten Parent Engagement Toolkit

Transitional Kindergarten Parent Engagement Toolkit A Parent Outreach and Communications Resource for School Districts and Local Education Agencies Implementing Transitional Kindergarten The Kindergarten

Transitional Kindergarten Parent Engagement Toolkit A Parent Outreach and Communications Resource for School Districts and Local Education Agencies Implementing Transitional Kindergarten The Kindergarten

Improving Outcomes for Homeless Youth

GUIDE TO GIVING Improving Outcomes for Homeless Youth HOW TO USE THIS GUIDE Are you interested in helping homeless youth? This guide will help you assess the effectiveness of the programs you are considering

GUIDE TO GIVING Improving Outcomes for Homeless Youth HOW TO USE THIS GUIDE Are you interested in helping homeless youth? This guide will help you assess the effectiveness of the programs you are considering

Life insurance. Shedding light on A PRACTICAL GUIDE TO HELPING YOU ACHIEVE A LIFETIME OF FINANCIAL SECURITY. Life s brighter under the sun

Shedding light on Life insurance A PRACTICAL GUIDE TO HELPING YOU ACHIEVE A LIFETIME OF FINANCIAL SECURITY LEARN MORE ABOUT: Safeguarding your loved ones Protecting your future Ensuring your dreams live

Shedding light on Life insurance A PRACTICAL GUIDE TO HELPING YOU ACHIEVE A LIFETIME OF FINANCIAL SECURITY LEARN MORE ABOUT: Safeguarding your loved ones Protecting your future Ensuring your dreams live

Financial Literacy and Young Teens

Report No. 1 April 2013 Financial literacy for kids and young teens is essential for their future prosperity. So what do our banks offer this specialised group of potential future customers? TEACHING THEM

Report No. 1 April 2013 Financial literacy for kids and young teens is essential for their future prosperity. So what do our banks offer this specialised group of potential future customers? TEACHING THEM

Information Packet. Expanding Health Insurance for Youth Aging Out of Foster. Care. By Natalie Mendes

Information Packet Expanding Health Insurance for Youth Aging Out of Foster Care By Natalie Mendes May 2015 Overview Research shows that young people in foster care are far more likely to endure homelessness,

Information Packet Expanding Health Insurance for Youth Aging Out of Foster Care By Natalie Mendes May 2015 Overview Research shows that young people in foster care are far more likely to endure homelessness,

Building Pathways, Creating Roadblocks: State Child Care Assistance Policies for Parents in School. May 2015

CHILD CARE Building Pathways, Creating Roadblocks: State Child Care Assistance Policies for Parents in School May 2015 Education and training opportunities help parents trying to gain more stable employment

CHILD CARE Building Pathways, Creating Roadblocks: State Child Care Assistance Policies for Parents in School May 2015 Education and training opportunities help parents trying to gain more stable employment

Big Data in Early Childhood: Using Integrated Data to Guide Impact

Big Data in Early Childhood: Using Integrated Data to Guide Impact Rob Fischer, Ph.D. & Beth Anthony, Ph.D. Center on Urban Poverty & Community Development Rebekah Dorman, Ph.D. Cuyahoga County Office

Big Data in Early Childhood: Using Integrated Data to Guide Impact Rob Fischer, Ph.D. & Beth Anthony, Ph.D. Center on Urban Poverty & Community Development Rebekah Dorman, Ph.D. Cuyahoga County Office

Understanding the Affordable Care Act

Understanding the Affordable Care Act The Affordable Care Act (officially called the Patient Protection and Affordable Care Act) is the law that mandates that everyone in the United States maintain health

Understanding the Affordable Care Act The Affordable Care Act (officially called the Patient Protection and Affordable Care Act) is the law that mandates that everyone in the United States maintain health

Business Example Car Wash Business Plan Soapy Rides Car Wash

Business Example Car Wash Business Plan Soapy Rides Car Wash http://www.bplans.com/car_wash_business_plan/company_summary_fc.php#.uciee6dwplu Read more: http://www.bplans.com/car_wash_business_plan/executive_summary_fc.php#ixzz22wl39guk

Business Example Car Wash Business Plan Soapy Rides Car Wash http://www.bplans.com/car_wash_business_plan/company_summary_fc.php#.uciee6dwplu Read more: http://www.bplans.com/car_wash_business_plan/executive_summary_fc.php#ixzz22wl39guk

Selected Publications Related to the American Dream Demonstration

Selected Publications Related to the American Dream Demonstration Beverly, S., & Clancy, M. (2001). Financial education in a children and youth savings account policy demonstration: issues and options

Selected Publications Related to the American Dream Demonstration Beverly, S., & Clancy, M. (2001). Financial education in a children and youth savings account policy demonstration: issues and options

Our Nation s Children at Risk: A State by State Report on Early Intervention

Our Nation s Children at Risk: A State by State Report on Early Intervention Message to Readers: Easter Seals is pleased to present Our Nation s Children at Risk: A State by State Report on Early Intervention.

Our Nation s Children at Risk: A State by State Report on Early Intervention Message to Readers: Easter Seals is pleased to present Our Nation s Children at Risk: A State by State Report on Early Intervention.

Aligning Resources and Results: How Communities and Policymakers Collaborated to Create a National Program

Aligning Resources and Results: How Communities and Policymakers Collaborated to Create a National Program The recent release of President Obama s fiscal year (FY) 2013 budget proposal provides an important

Aligning Resources and Results: How Communities and Policymakers Collaborated to Create a National Program The recent release of President Obama s fiscal year (FY) 2013 budget proposal provides an important

Asset-Building and Financial Education Programs

CONNECTED BY 25: FINANCING Asset-Building and Financial Education Programs FOR YOUTH TRANSITIONING OUT OF FOSTER CARE CONNECTED BY 25: FINANCING Asset-Building and Financial Education Programs FOR YOUTH

CONNECTED BY 25: FINANCING Asset-Building and Financial Education Programs FOR YOUTH TRANSITIONING OUT OF FOSTER CARE CONNECTED BY 25: FINANCING Asset-Building and Financial Education Programs FOR YOUTH

Colony SM Term. The Traditional Term Life Insurance Solution. Consumer Guide I Colony SM Term I Life Insurance

Consumer Guide I Colony SM Term I Life Insurance Colony SM Term The Traditional Term Life Insurance Solution Life insurance products underwritten by: Genworth Life and Annuity Insurance Company, Genworth

Consumer Guide I Colony SM Term I Life Insurance Colony SM Term The Traditional Term Life Insurance Solution Life insurance products underwritten by: Genworth Life and Annuity Insurance Company, Genworth

Michael Makes a Plan

Cast Michael Mom Dad Mr. Henson Receptionist James Moore Narrator Michael Makes a Plan ACT I Narrator Michael Marino is sitting in his living room with his parents discussing his job possibilities after

Cast Michael Mom Dad Mr. Henson Receptionist James Moore Narrator Michael Makes a Plan ACT I Narrator Michael Marino is sitting in his living room with his parents discussing his job possibilities after

Statement by. Lynnae Ruttledge. Commissioner, Rehabilitation Services Administration

Statement by Lynnae Ruttledge Commissioner, Rehabilitation Services Administration On RSA s Leadership in Improving Employment Outcomes for Students with Intellectual Disabilities Transitioning to Careers

Statement by Lynnae Ruttledge Commissioner, Rehabilitation Services Administration On RSA s Leadership in Improving Employment Outcomes for Students with Intellectual Disabilities Transitioning to Careers

AEDC User Guide: Schools

Our Children Our Communities Our Future AEDC User Guide: Schools This AEDC user guide leads schools through the steps they might take when thinking about how to respond to AEDC data for their community.

Our Children Our Communities Our Future AEDC User Guide: Schools This AEDC user guide leads schools through the steps they might take when thinking about how to respond to AEDC data for their community.

Maria lived in a dozen foster homes and several

BY JOHN EMERSON Maria lived in a dozen foster homes and several group homes during her seven years in foster care. She attended eight high schools, placed in programs ranging from special education to

BY JOHN EMERSON Maria lived in a dozen foster homes and several group homes during her seven years in foster care. She attended eight high schools, placed in programs ranging from special education to

Franchising USA HEALTHY FRANCHISING WOMEN IN FRANCHISING: HOW MUCH MONEY WILL YOUR FRANCHISE MAKE? WEIGHT LOSS & WELLNESS: FROM MARKETING TO MILLIONS

THE MAGAZINE FOR FRANCHISEES VOL 02, ISSUE 05, MAR 2014 $5.95 www.franchisingusamagazine.com WEIGHT LOSS & WELLNESS: HEALTHY FRANCHISING HOW MUCH MONEY WILL YOUR FRANCHISE MAKE? WOMEN IN FRANCHISING: FROM

THE MAGAZINE FOR FRANCHISEES VOL 02, ISSUE 05, MAR 2014 $5.95 www.franchisingusamagazine.com WEIGHT LOSS & WELLNESS: HEALTHY FRANCHISING HOW MUCH MONEY WILL YOUR FRANCHISE MAKE? WOMEN IN FRANCHISING: FROM

SECTION I: Current Michigan Policies on Postsecondary Education for Low-income Parents Receiving Public Assistance

SECTION I: Current Michigan Policies on Postsecondary Education for Low-income Parents Receiving Public Assistance 10 Current Michigan Policies The survey and this report focus on the policies and practices

SECTION I: Current Michigan Policies on Postsecondary Education for Low-income Parents Receiving Public Assistance 10 Current Michigan Policies The survey and this report focus on the policies and practices

Educational Rights. Source of Rights for Children in the Child Welfare System. Florida Constitution

Florida Constitution Right to High Quality Education Article IX (a). Adequate provision shall be made by law for a uniform, efficient, safe, secure, and high quality system of free public schools that

Florida Constitution Right to High Quality Education Article IX (a). Adequate provision shall be made by law for a uniform, efficient, safe, secure, and high quality system of free public schools that

Life Insurance. Nationwide and the Nationwide Frame are federally registered service marks of Nationwide Mutual Insurance Company.

Life Insurance Nationwide and the Nationwide Frame are federally registered service marks of Nationwide Mutual Insurance Company. Facilitator s Guide Life Insurance Overview: If you ask people to name

Life Insurance Nationwide and the Nationwide Frame are federally registered service marks of Nationwide Mutual Insurance Company. Facilitator s Guide Life Insurance Overview: If you ask people to name

Highlights from State Reports to the National Youth in Transition Database, Federal Fiscal Year 2011

Data Brief #1 Highlights from State Reports to the National Youth in Transition Database, Federal Fiscal Year 2011 September 2012 Background In 1999, Public Law 106-169 established the John H. Chafee Foster

Data Brief #1 Highlights from State Reports to the National Youth in Transition Database, Federal Fiscal Year 2011 September 2012 Background In 1999, Public Law 106-169 established the John H. Chafee Foster

CHOP Karabots Early Head Start (HS/EHS) Case Study

Case Study") CHOP Karabots Early Head Start (HS/EHS) Case Study Background For the past thirteen years, The Children s Hospital of Philadelphia Early Head Start (CHOP Karabots EHS) has provided high-quality child development

CHOP Karabots Early Head Start (HS/EHS) Case Study Background For the past thirteen years, The Children s Hospital of Philadelphia Early Head Start (CHOP Karabots EHS) has provided high-quality child development

Affordable Care Act: What The Health Care Law Means for Small Businesses

Affordable Care Act: What The Health Care Law Means for Small Businesses August 2013 Indian Country Business Summit These materials are provided for informational purposes only and are not intended as

Affordable Care Act: What The Health Care Law Means for Small Businesses August 2013 Indian Country Business Summit These materials are provided for informational purposes only and are not intended as

PUBLISHER OF CONSUMER REPORTS The Affordable Care Act: The First Year DISCOVER WHAT THE NEW LAW MEANS FOR YOU AND YOUR FAMILY

PUBLISHER OF CONSUMER REPORTS The Affordable Care Act: The First Year DISCOVER WHAT THE NEW LAW MEANS FOR YOU AND YOUR FAMILY A Note About Using This Guide: What s a Grandfathered Plan? You ll see references

PUBLISHER OF CONSUMER REPORTS The Affordable Care Act: The First Year DISCOVER WHAT THE NEW LAW MEANS FOR YOU AND YOUR FAMILY A Note About Using This Guide: What s a Grandfathered Plan? You ll see references